1. Autoformer

Autoformer

BaseModel

Autoformer

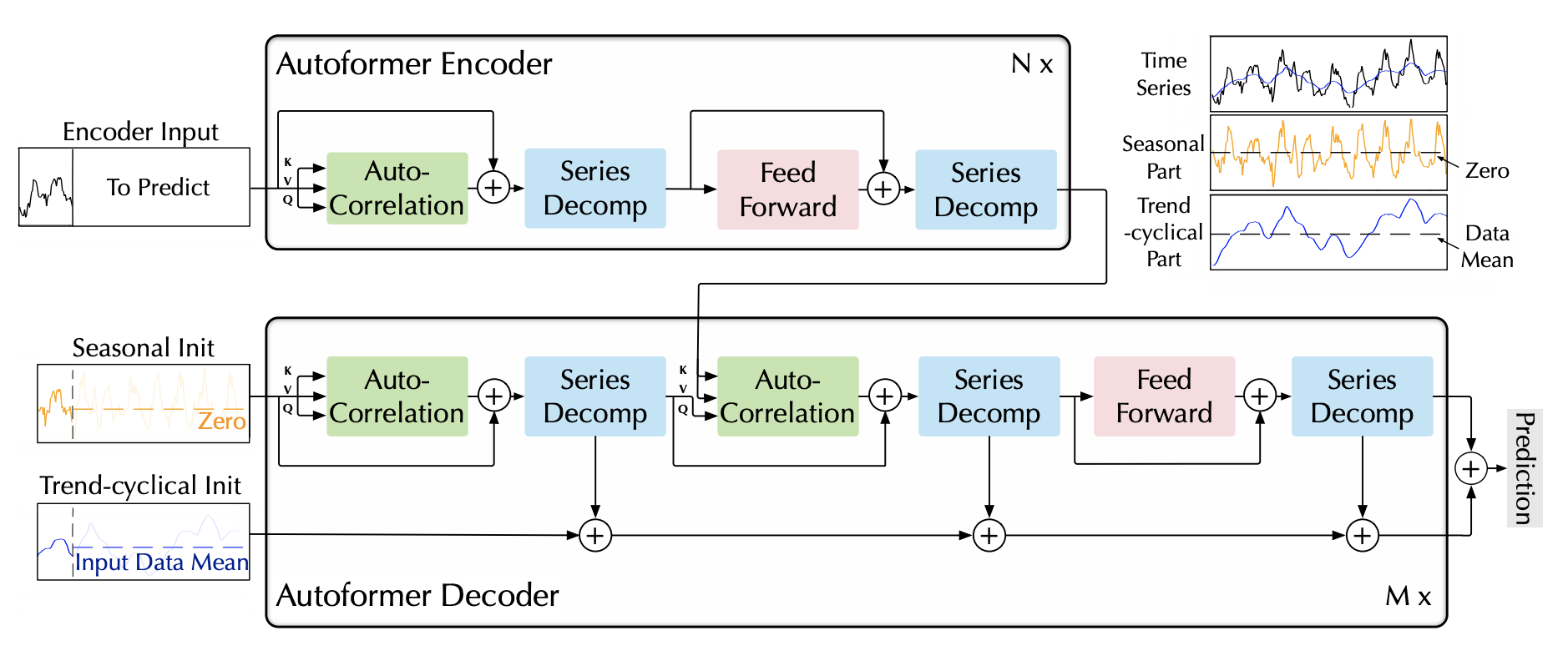

The Autoformer model tackles the challenge of finding reliable dependencies on intricate temporal patterns of long-horizon forecasting.

The architecture has the following distinctive features:

- In-built progressive decomposition in trend and seasonal compontents based on a moving average filter.

- Auto-Correlation mechanism that discovers the period-based dependencies by calculating the autocorrelation and aggregating similar sub-series based on the periodicity.

- Classic encoder-decoder proposed by Vaswani et al. (2017) with a multi-head attention mechanism.

- It employs encoded autoregressive features obtained from a convolution network.

- Absolute positional embeddings obtained from calendar features are utilized.

Autoformer.fit

fit method, optimizes the neural network’s weights using the

initialization parameters (learning_rate, windows_batch_size, …)

and the loss function as defined during the initialization.

Within fit we use a PyTorch Lightning Trainer that

inherits the initialization’s self.trainer_kwargs, to customize

its inputs, see PL’s trainer arguments.

The method is designed to be compatible with SKLearn-like classes

and in particular to be compatible with the StatsForecast library.

By default the model is not saving training checkpoints to protect

disk memory, to get them change enable_checkpointing=True in __init__.

Parameters:

Returns:

Autoformer.predict

Trainer execution of predict_step.

Parameters:

Returns:

Usage Example

2. Auxiliary functions

Decoder

Module

Autoformer decoder

DecoderLayer

Module

Autoformer decoder layer with the progressive decomposition architecture

Encoder

Module

Autoformer encoder

EncoderLayer

Module

Autoformer encoder layer with the progressive decomposition architecture

LayerNorm

Module

Special designed layernorm for the seasonal part

AutoCorrelationLayer

Module

Auto Correlation Layer

AutoCorrelation

Module

AutoCorrelation Mechanism with the following two phases:

(1) period-based dependencies discovery

(2) time delay aggregation

This block can replace the self-attention family mechanism seamlessly.