- Convergence speed: Neural forecasting models tend to converge faster when the features are on a similar scale.

- Avoiding vanishing or exploding gradients: some architectures, such as recurrent neural networks (RNNs), are sensitive to the scale of input data. If the input values are too large, it could lead to exploding gradients, where the gradients become too large and the model becomes unstable. Conversely, very small input values could lead to vanishing gradients, where weight updates during training are negligible and the training fails to converge.

- Ensuring consistent scale: Neural forecasting models have shared global parameters for the all time series of the task. In cases where time series have different scale, scaling ensures that no particular time series dominates the learning process.

- Improving generalization: time series with consistent scale can lead to smoother loss surfaces. Moreover, scaling helps to homogenize the distribution of the input data, which can also improve generalization by avoiding out-of-range values.

Neuralforecast library integrates two types of temporal scaling:

- Time Series Scaling: scaling each time series using all its data

on the train set before start training the model. This is done by

using the

local_scaler_typeparameter of theNeuralforecastcore class. - Window scaling (TemporalNorm): scaling each input window

separetly for each element of the batch at every training iteration.

This is done by using the

scaler_typeparameter of each model class.

1. Install Neuralforecast

2. Load Data

Thedf dataframe contains the target and exogenous variables past

information to train the model. The unique_id column identifies the

markets, ds contains the datestamps, and y the electricity price.

For future variables, we include a forecast of how much electricity will

be produced (gen_forecast), and day of week (week_day). Both the

electricity system demand and offer impact the price significantly,

including these variables to the model greatly improve performance, as

we demonstrate in Olivares et al. (2022).

The futr_df dataframe includes the information of the future exogenous

variables for the period we want to forecast (in this case, 24 hours

after the end of the train dataset df).

We can see that

y and the exogenous variables are on largely different

scales. Next, we show two methods to scale the data.

3. Time Series Scaling with Neuralforecast class

One of the most widely used approches for scaling time series is to

treat it as a pre-processing step, where each time series and temporal

exogenous variables are scaled based on their entire information in the

train set. Models are then trained on the scaled data.

To simplify pipelines, we added a scaling functionality to the

Neuralforecast class. Each time series will be scaled before training

the model with either fit or cross_validation, and scaling

statistics are stored. The class then uses the stored statistics to

scale the forecasts back to the original scale before returning the

forecasts.

3.a. Instantiate model and Neuralforecast class

In this example we will use the TimesNet model, recently proposed in

Wu, Haixu, et al. (2022). First

instantiate the model with the desired parameters.

NeuralForecast object and using the

fit method. The local_scaler_type parameter is used to specify the

type of scaling to be used. In this case, we will use standard, which

scales the data to have zero mean and unit variance.Other supported

scalers are minmax, robust, robust-iqr, minmax, and boxcox.

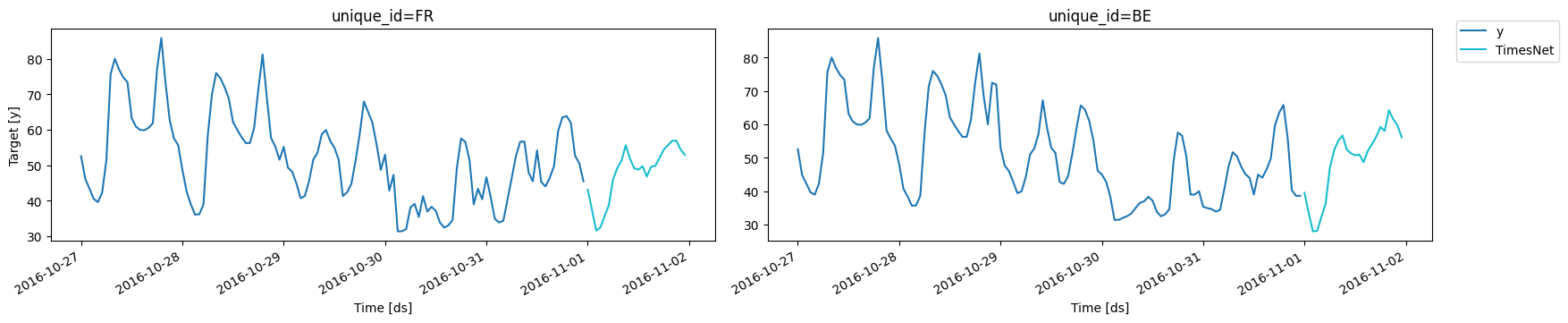

3.b Forecast and plots

Finally, use thepredict method to forecast the day-ahead prices. The

Neuralforecast class handles the inverse normalization, forecasts are

returned in the original scale.

Important The inverse scaling is performed by theNeuralforecastclass before returning the final forecasts. Therefore, the hyperparmater selection withAutomodels and validation loss for early stopping or model selection are performed on the scaled data. Different types of scaling with theNeuralforecastclass can’t be automatically compared withAutomodels.

4. Temporal Window normalization during training

Temporal normalization scales each instance of the batch separately at the window level. It is performed at each training iteration for each window of the batch, for both target variable and temporal exogenous covariates. For more details, see Olivares et al. (2023) and https://nixtlaverse.nixtla.io/neuralforecast/common.scalers.html.4.a. Instantiate model and Neuralforecast class

Temporal normalization is specified by the scaler_type argument.

Currently, it is only supported for Windows-based models (NHITS,

NBEATS, MLP, TimesNet, and all Transformers). In this example, we

use the TimesNet model and robust scaler, recently proposed by Wu,

Haixu, et al. (2022). First instantiate the model with the desired

parameters.

Visit https://nixtlaverse.nixtla.io/neuralforecast/common.scalers.html

for a complete list of supported scalers.

NeuralForecast object and using the

fit method. Note that local_scaler_type has None as default to

avoid scaling the data before training.

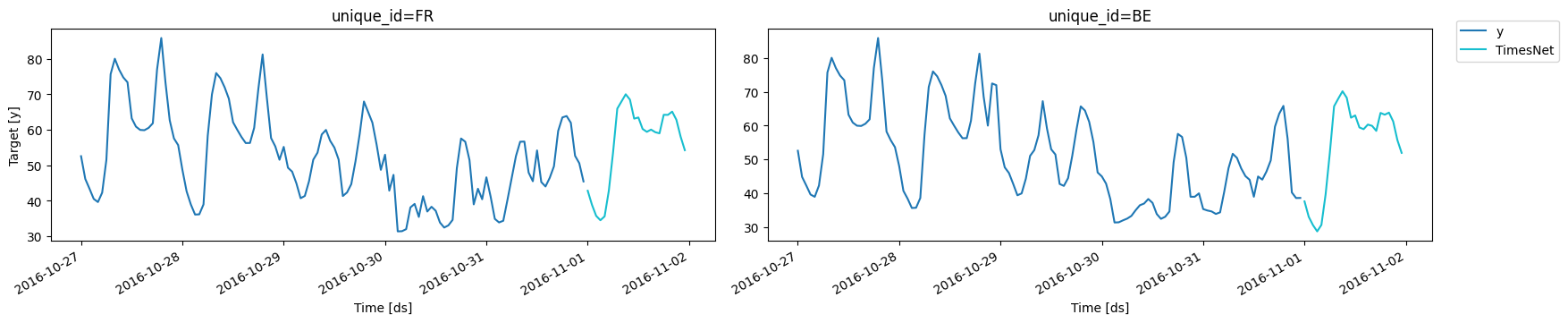

4.b Forecast and plots

Finally, use thepredict method to forecast the day-ahead prices. The

forecasts are returned in the original scale.

Important For most applications, models with temporal normalization (section 4) produced more accurate forecasts than time series scaling (section 3). However, with temporal normalization models lose the information of the relative level between different windows. In some cases this global information within time series is crucial, for instance when an exogenous variables contains the dosage of a medication. In these cases, time series scaling (section 3) is preferred.

References

- Kin G. Olivares, David Luo, Cristian Challu, Stefania La Vattiata, Max Mergenthaler, Artur Dubrawski (2023). “HINT: Hierarchical Mixture Networks For Coherent Probabilistic Forecasting”. International Conference on Machine Learning (ICML). Workshop on Structured Probabilistic Inference & Generative Modeling. Available at https://arxiv.org/abs/2305.07089.

- Wu, Haixu, Tengge Hu, Yong Liu, Hang Zhou, Jianmin Wang, and Mingsheng Long. “Timesnet: Temporal 2d-variation modeling for general time series analysis.”, ICLR 2023