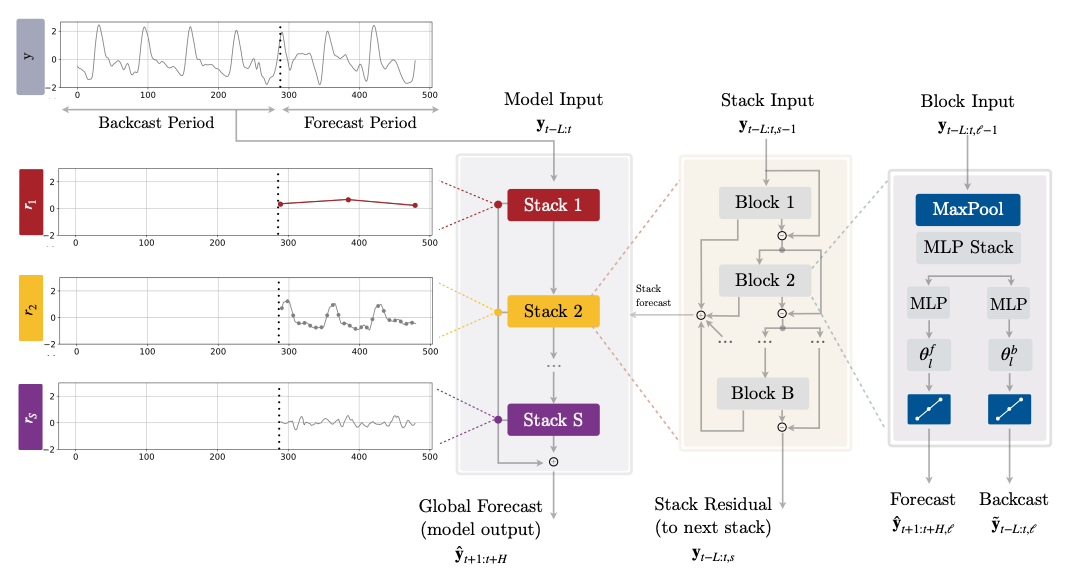

NHITS

builds upon

NBEATS

and specializes its partial outputs in the different frequencies of the

time series through hierarchical interpolation and multi-rate input

processing. On the long-horizon forecasting task

NHITS

improved accuracy by 25% on AAAI’s best paper award the

Informer,

while being 50x faster.

The model is composed of several MLPs with ReLU non-linearities. Blocks

are connected via doubly residual stacking principle with the backcast

and forecast

outputs of the l-th block. Multi-rate

input pooling, hierarchical interpolation and backcast residual

connections together induce the specialization of the additive

predictions in different signal bands, reducing memory footprint and

computational time, thus improving the architecture parsimony and

accuracy.

References

- Boris N. Oreshkin, Dmitri Carpov, Nicolas Chapados, Yoshua Bengio (2019). “N-BEATS: Neural basis expansion analysis for interpretable time series forecasting”.

- Cristian Challu, Kin G. Olivares, Boris N. Oreshkin, Federico Garza, Max Mergenthaler-Canseco, Artur Dubrawski (2023). “NHITS: Neural Hierarchical Interpolation for Time Series Forecasting”. Accepted at the Thirty-Seventh AAAI Conference on Artificial Intelligence.

- Zhou, H.; Zhang, S.; Peng, J.; Zhang, S.; Li, J.; Xiong, H.; and Zhang, W. (2020). “Informer: Beyond Efficient Transformer for Long Sequence Time-Series Forecasting”. Association for the Advancement of Artificial Intelligence Conference 2021 (AAAI 2021).

NHITS

NHITS

BaseModel

NHITS

The Neural Hierarchical Interpolation for Time Series (NHITS), is an MLP-based deep

neural architecture with backward and forward residual links. NHITS tackles volatility and

memory complexity challenges, by locally specializing its sequential predictions into

the signals frequencies with hierarchical interpolation and pooling.

Parameters:

NHITS.fit

fit method, optimizes the neural network’s weights using the

initialization parameters (learning_rate, windows_batch_size, …)

and the loss function as defined during the initialization.

Within fit we use a PyTorch Lightning Trainer that

inherits the initialization’s self.trainer_kwargs, to customize

its inputs, see PL’s trainer arguments.

The method is designed to be compatible with SKLearn-like classes

and in particular to be compatible with the StatsForecast library.

By default the model is not saving training checkpoints to protect

disk memory, to get them change enable_checkpointing=True in __init__.

Parameters:

Returns:

NHITS.predict

Trainer execution of predict_step.

Parameters:

Returns: