Step-by-step guide on using theIn this walkthrough, we will become familiar with the mainGARCH ModelwithStatsforecast.

StatsForecast class and some relevant methods such as

StatsForecast.plot, StatsForecast.forecast and

StatsForecast.cross_validation.

The text in this article is largely taken from: 1. Changquan Huang •

Alla Petukhina. Springer series (2022). Applied Time Series Analysis and

Forecasting with

Python. 2.

Bollerslev, T. (1986). Generalized autoregressive conditional

heteroskedasticity. Journal of econometrics, 31(3),

307-327.

3. Engle, R. F. (1982). Autoregressive conditional heteroscedasticity

with estimates of the variance of United Kingdom inflation.

Econometrica: Journal of the econometric society,

987-1007.. 4.

James D. Hamilton. Time Series Analysis Princeton University Press,

Princeton, New Jersey, 1st Edition,

1994.

Table of Contents

- Introduction

- GARCH Models

- Loading libraries and data

- Explore data with the plot method

- Split the data into training and testing

- Implementation of GARCH with StatsForecast

- Cross-validation

- Model evaluation

- References

Introduction

The Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model is a statistical technique used to model and predict volatility in financial and economic time series. It was developed by Robert Engle in 1982 as an extension of the Autoregressive Conditional Heteroskedasticity (ARCH) model proposed by Andrew Lo and Craig MacKinlay in 1988. The GARCH model allows capturing the presence of conditional heteroscedasticity in time series data, that is, the presence of fluctuations in the variance of a time series as a function of time. This is especially useful in financial data analysis, where volatility can be an important measure of risk. The GARCH model has become a fundamental tool in the analysis of financial time series and has been used in a wide variety of applications, from risk management to forecasting prices of shares and other financial values.Definition of GARCH Models

Definition 1. A model with order is of the form where ,and are constants,, and is independent of . A stochastic process is called a process if it satisfies Eq. (1). In practice, it has been found that for some time series, the model defined by (1) will provide an adequate fit only if the order is large. By allowing past volatilities to affect the present volatility in (1), a more parsimonious model may result. That is why we needGARCH models. Besides, note the condition that the order

. The GARCH model in Definition 1 has the properties as

follows.

Proposition 1. If is a process defined in (1)

and ,then the

following propositions hold.

- follows the model

- is a white noise with

- is the conditional variance of , that is, we have

- Model (1) reflects the fat tails and volatility clustering.

Advantages and disadvantages of the Generalized Autoregressive Conditional Heteroskedasticity (GARCH) Model

The Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model can be applied in several fields

The Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model can be applied in a wide variety of areas where time series volatility is required to be modeled and predicted. Some of the areas in which the GARCH model can be applied are:- Financial markets: the GARCH model is widely used to model the volatility (risk) of returns on financial assets such as stocks, bonds, currencies, etc. It allows you to capture the changing nature of volatility.

- Commodity prices: the prices of raw materials such as oil, gold, grains, etc. they exhibit conditional volatility that can be modeled with GARCH.

- Credit risk: the risk of non-payment of loans and bonds also presents volatility over time that suits GARCH well.

- Economic time series: macroeconomic indicators such as inflation, GDP, unemployment, etc. they have conditional volatility modelable with GARCH.

- Implicit volatility: the GARCH model allows estimating the implicit volatility in financial options.

- Forecasts: GARCH allows conditional volatility forecasts to be made in any time series.

- Risk analysis: GARCH is useful for measuring and managing the risk of investment portfolios and assets.

- Finance: The GARCH model is widely used in finance to model the price volatility of financial assets, such as stocks, bonds, and currencies.

- Economics: The GARCH model is used in economics to model the volatility of the prices of goods and services, inflation, and other economic indicators.

- Environmental sciences: The GARCH model is applied in environmental sciences to model the volatility of variables such as temperature, precipitation, and air quality.

- Social sciences: The GARCH model is used in the social sciences to model the volatility of variables such as crime, migration, and employment.

- Engineering: The GARCH model is applied in engineering to model the volatility of variables such as the demand for electrical energy, industrial production, and vehicular traffic.

- Health sciences: The GARCH model is used in health sciences to model the volatility of variables such as the number of cases of infectious diseases and the prices of medicines.

Loading libraries and data

Tip Statsforecast will be needed. To install, see instructions.Next, we import plotting libraries and configure the plotting style.

Read Data

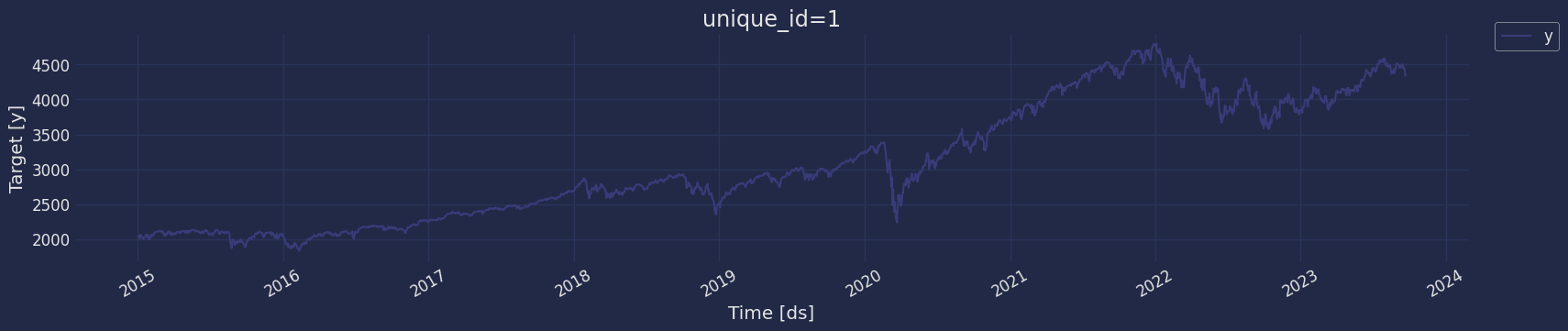

Let’s pull the S&P500 stock data from the Yahoo Finance site.-

The

unique_id(string, int or category) represents an identifier for the series. -

The

ds(datestamp) column should be of a format expected by Pandas, ideally YYYY-MM-DD for a date or YYYY-MM-DD HH:MM:SS for a timestamp. -

The

y(numeric) represents the measurement we wish to forecast.

Explore data with the plot method

Plot a series using the plot method from the StatsForecast class. This method prints a random series from the dataset and is useful for basic EDA.

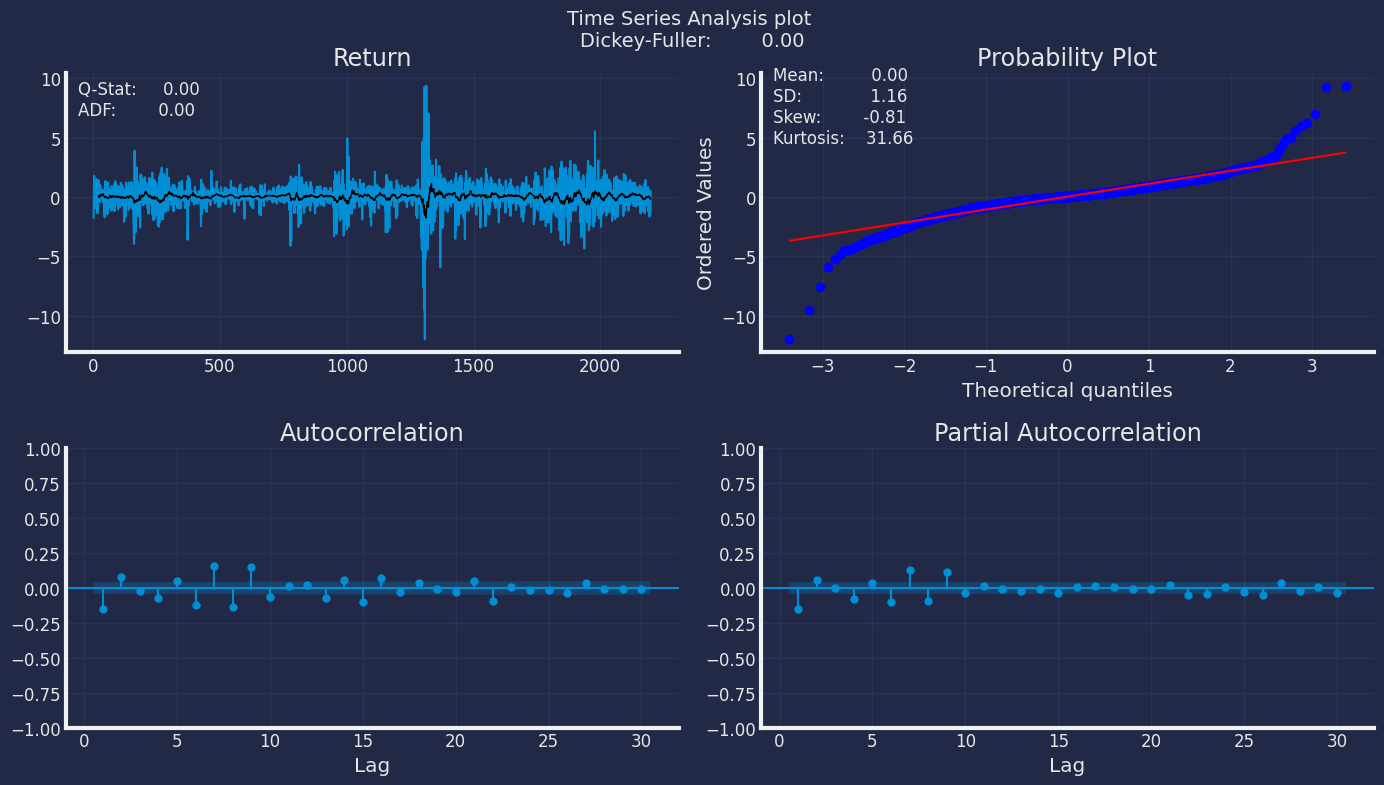

The Augmented Dickey-Fuller Test

An Augmented Dickey-Fuller (ADF) test is a type of statistical test that determines whether a unit root is present in time series data. Unit roots can cause unpredictable results in time series analysis. A null hypothesis is formed in the unit root test to determine how strongly time series data is affected by a trend. By accepting the null hypothesis, we accept the evidence that the time series data is not stationary. By rejecting the null hypothesis or accepting the alternative hypothesis, we accept the evidence that the time series data is generated by a stationary process. This process is also known as stationary trend. The values of the ADF test statistic are negative. Lower ADF values indicate a stronger rejection of the null hypothesis. Augmented Dickey-Fuller Test is a common statistical test used to test whether a given time series is stationary or not. We can achieve this by defining the null and alternate hypothesis. Null Hypothesis: Time Series is non-stationary. It gives a time-dependent trend. Alternate Hypothesis: Time Series is stationary. In another term, the series doesn’t depend on time. ADF or t Statistic < critical values: Reject the null hypothesis, time series is stationary. ADF or t Statistic > critical values: Failed to reject the null hypothesis, time series is non-stationary. Let’s check if our series that we are analyzing is a stationary series. Let’s create a function to check, using theDickey Fuller test

Augmented_Dickey_Fuller

test gives us a p-value of 0.864700, which tells us that the null

hypothesis cannot be rejected, and on the other hand the data of our

series are not stationary.

We need to differentiate our time series, in order to convert the data

to stationary.

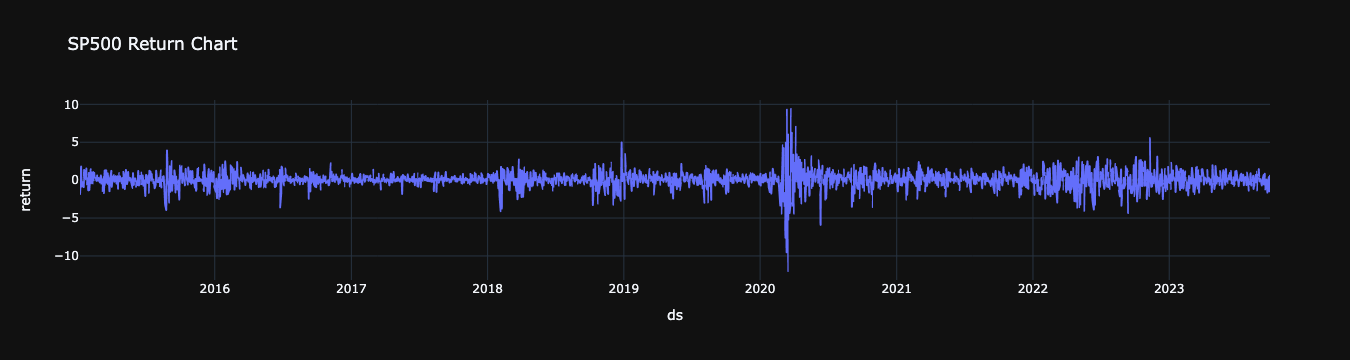

Return Series

Since the 1970s, the financial industry has been very prosperous with advancement of computer and Internet technology. Trade of financial products (including various derivatives) generates a huge amount of data which form financial time series. For finance, the return on a financial product is most interesting, and so our attention focuses on the return series. If is the closing price at time t for a certain financial product, then the return on this product is It is return series that have been much independently studied. And important stylized features which are common across many instruments, markets, and time periods have been summarized. Note that if you purchase the financial product, then it becomes your asset, and its returns become your asset returns. Now let us look at the following examples. We can estimate the series of returns using the pandas,DataFrame.pct_change() function. The pct_change() function has a

periods parameter whose default value is 1. If you want to calculate a

30-day return, you must change the value to 30.

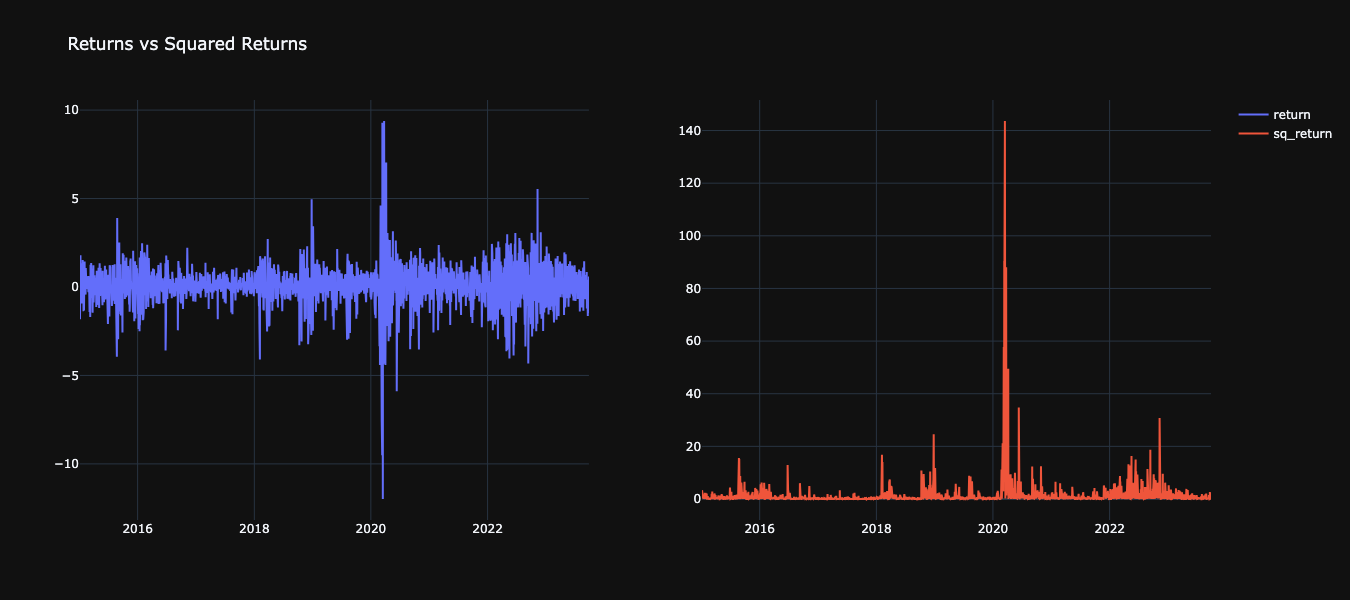

Creating Squared Returns

Returns vs Squared Returns

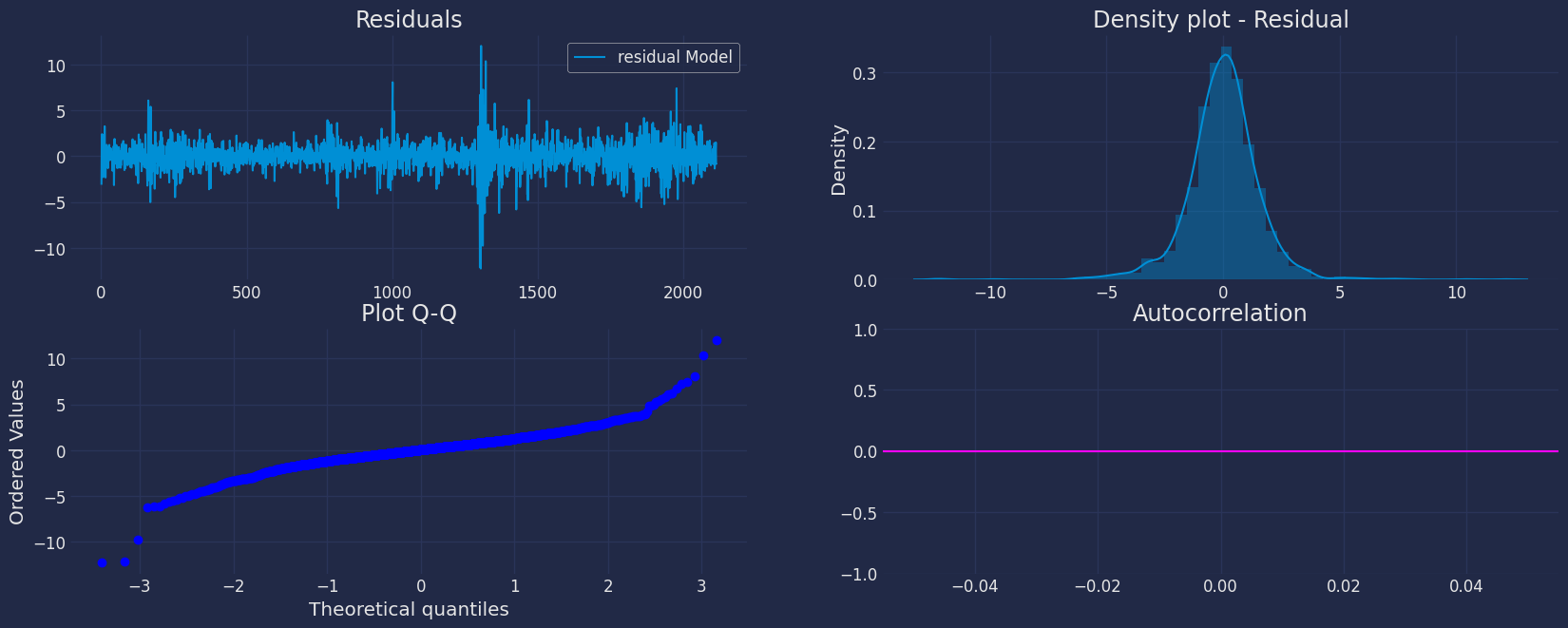

Ljung-Box Test

Ljung-Box is a test for autocorrelation that we can use in tandem with our ACF and PACF plots. The Ljung-Box test takes our data, optionally either lag values to test, or the largest lag value to consider, and whether to compute the Box-Pierce statistic. Ljung-Box and Box-Pierce are two similar test statisitcs, Q , that are compared against a chi-squared distribution to determine if the series is white noise. We might use the Ljung-Box test on the residuals of our model to look for autocorrelation, ideally our residuals would be white noise.- Ho : The data are independently distributed, no autocorrelation.

- Ha : The data are not independently distributed; they exhibit serial correlation.

Split the data into training and testing

Let’s divide our data into sets 1. Data to train ourGARCH model 2.

Data to test our model

For the test data we will use the last 30 day to test and evaluate the

performance of our model.

Implementation of GARCH with StatsForecast

Load libraries

Instantiating Models

Import and instantiate the models. Setting the argument is sometimes tricky. This article on Seasonal periods by the master, Rob Hyndmann, can be useful.season_length.-

freq:a string indicating the frequency of the data. (See pandas’ available frequencies.) -

n_jobs:n_jobs: int, number of jobs used in the parallel processing, use -1 for all cores. -

fallback_model:a model to be used if a model fails.

Cross-validation

We have built different GARCH models, so we need to determine which is the best model to then be able to train it and thus be able to make the predictions. To know which is the best model we go to the Cross Validation. With time series data, Cross Validation is done by defining a sliding window across the historical data and predicting the period following it. This form of cross-validation allows us to arrive at a better estimation of our model’s predictive abilities across a wider range of temporal instances while also keeping the data in the training set contiguous as is required by our models. The following graph depicts such a Cross Validation Strategy:

Perform time series cross-validation

Cross-validation of time series models is considered a best practice but most implementations are very slow. The statsforecast library implements cross-validation as a distributed operation, making the process less time-consuming to perform. If you have big datasets you can also perform Cross Validation in a distributed cluster using Ray, Dask or Spark. The cross_validation method from the StatsForecast class takes the following arguments.-

df:training data frame -

h (int):represents h steps into the future that are being forecasted. In this case, 12 months ahead. -

step_size (int):step size between each window. In other words: how often do you want to run the forecasting processes. -

n_windows(int):number of windows used for cross validation. In other words: what number of forecasting processes in the past do you want to evaluate.

unique_id:series identifierds:datestamp or temporal indexcutoff:the last datestamp or temporal index for the n_windows.y:true value"model":columns with the model’s name and fitted value.

StatsForecast, and in particular the GARCH model and the

parameters used in Cross Validation to determine the best model for this

example.

In the previous result it can be seen that the best model is the model

With this result found using Cross Validation to determine which is the

best model, we are going to continue training our model, to then make

the predictions.

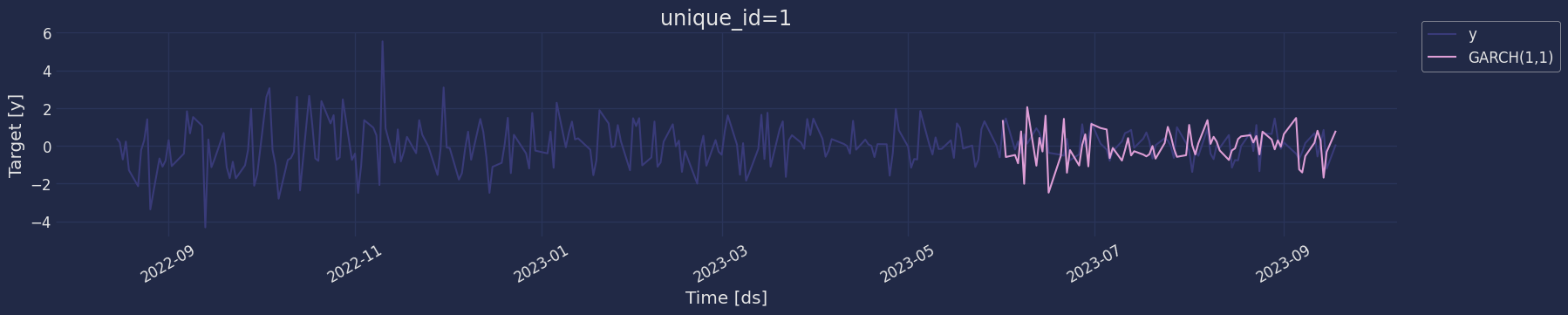

Fit the Model

.get() function to extract the element and then we are going to save

it in a pd.DataFrame().

Forecast Method

If you want to gain speed in productive settings where you have multiple series or models we recommend using theStatsForecast.forecast method

instead of .fit and .predict.

The main difference is that the .forecast doest not store the fitted

values and is highly scalable in distributed environments.

The forecast method takes two arguments: forecasts next h (horizon)

and level.

-

h (int):represents the forecast h steps into the future. In this case, 12 months ahead. -

level (list of floats):this optional parameter is used for probabilistic forecasting. Set the level (or confidence percentile) of your prediction interval. For example,level=[90]means that the model expects the real value to be inside that interval 90% of the times.

ARIMA and Theta)

Adding 95% confidence interval with the forecast method

Predict method with confidence interval

To generate forecasts use the predict method. The predict method takes two arguments: forecasts the nexth (for

horizon) and level.

-

h (int):represents the forecast h steps into the future. In this case, 30 dayly ahead. -

level (list of floats):this optional parameter is used for probabilistic forecasting. Set the level (or confidence percentile) of your prediction interval. For example,level=[95]means that the model expects the real value to be inside that interval 95% of the times.

Model Evaluation

Now we are going to evaluate our model with the results of the predictions, we will use different types of metrics MAE, MAPE, MASE, RMSE, SMAPE to evaluate the accuracy.References

- Changquan Huang • Alla Petukhina. Springer series (2022). Applied Time Series Analysis and Forecasting with Python.

- Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of econometrics, 31(3), 307-327.

- Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the econometric society, 987-1007..

- James D. Hamilton. Time Series Analysis Princeton University Press, Princeton, New Jersey, 1st Edition, 1994.

- Nixtla Garch API

- Pandas available frequencies.

- Rob J. Hyndman and George Athanasopoulos (2018). “Forecasting Principles and Practice (3rd ed)”.

- Seasonal periods- Rob J Hyndman.