Step-by-step guide on using theThe objective of the following article is to obtain a step-by-step guide on building the Arima model usingAutoARIMA ModelwithStatsforecast.

AutoARIMA with Statsforecast.

During this walkthrough, we will become familiar with the main

StatsForecast class and some relevant methods such as

StatsForecast.plot, StatsForecast.forecast and

StatsForecast.cross_validation.

The text in this article is largely taken from Rob J. Hyndman and

George Athanasopoulos (2018). “Forecasting Principles and Practice (3rd

ed)”.

Table of Contents

- What is AutoArima with StatsForecast?

- Definition of the Arima model

- Advantages of using AutoArima

- Loading libraries and data

- Explore data with the plot method

- Split the data into training and testing

- Implementation of AutoARIMA with StatsForecast

- Cross-validation

- Model evaluation

- References

What is AutoArima with StatsForecast?

An autoARIMA is a time series model that uses an automatic process to select the optimal ARIMA (Autoregressive Integrated Moving Average) model parameters for a given time series. ARIMA is a widely used statistical model for modeling and predicting time series. The process of automatic parameter selection in an autoARIMA model is performed using statistical and optimization techniques, such as the Akaike Information Criterion (AIC) and cross-validation, to identify optimal values for autoregression, integration, and moving average parameters. of the ARIMA model. Automatic parameter selection is useful because it can be difficult to determine the optimal parameters of an ARIMA model for a given time series without a thorough understanding of the underlying stochastic process that generates the time series. The autoARIMA model automates the parameter selection process and can provide a fast and effective solution for time series modeling and forecasting. Thestatsforecast.models library brings the AutoARIMA function from

Python provides an implementation of autoARIMA that allows to

automatically select the optimal parameters for an ARIMA model given a

time series.

Definition of the Arima model

An Arima model (autoregressive integrated moving average) process is the combination of an autoregressive process AR(p), integration I(d), and the moving average process MA(q). Just like the ARMA process, the ARIMA process states that the present value is dependent on past values, coming from the AR(p) portion, and past errors, coming from the MA(q) portion. However, instead of using the original series, denoted as yt, the ARIMA process uses the differenced series, denoted as . Note that can represent a series that has been differenced more than once. Therefore, the mathematical expression of the ARIMA(p,d,q) process states that the present value of the differenced series is equal to the sum of a constant , past values of the differenced series , the mean of the differenced series , past error terms , and a current error term , as shown in equation where is the differenced series (it may have been differenced more than once). The “predictors” on the right hand side include both lagged values of and lagged errors. We call this an ARIMA( p,d,q) model, where

The same stationarity and invertibility conditions that are used for

autoregressive and moving average models also apply to an ARIMA model.

Many of the models we have already discussed are special cases of the

ARIMA model, as shown in Table

Once we start combining components in this way to form more complicated

models, it is much easier to work with the backshift notation. For

example, Equation (1) can be written in backshift notation as:

Selecting appropriate values for p, d and q can be difficult. However,

the

AutoARIMA() function from statsforecast will do it for you

automatically.

For more information

here

Loading libraries and data

Using anAutoARIMA() model to model and predict time series has

several advantages, including:

-

Automation of the parameter selection process: The

AutoARIMA()function automates the ARIMA model parameter selection process, which can save the user time and effort by eliminating the need to manually try different combinations of parameters. - Reduction of prediction error: By automatically selecting optimal parameters, the ARIMA model can improve the accuracy of predictions compared to manually selected ARIMA models.

-

Identification of complex patterns: The

AutoARIMA()function can identify complex patterns in the data that may be difficult to detect visually or with other time series modeling techniques. - Flexibility in the choice of the parameter selection methodology: The ARIMA Model can use different methodologies to select the optimal parameters, such as the Akaike Information Criterion (AIC), cross-validation and others, which allows the user to choose the methodology that best suits their needs.

AutoARIMA() function can help improve the

efficiency and accuracy of time series modeling and forecasting,

especially for users who are inexperienced with manual parameter

selection for ARIMA models.

Main results

We compared accuracy and speed against pmdarima, Rob Hyndman’s forecast package and Facebook’s Prophet. We used theDaily, Hourly and Weekly data from the M4

competition.

The following table summarizes the results. As can be seen, our

auto_arima is the best model in accuracy (measured by the MASE loss)

and time, even compared with the original implementation in R.

[1] The model

auto_arima from pmdarima had a problem with Hourly

data. An issue was opened.

The following table summarizes the data details.

Loading libraries and data

Tip Statsforecast will be needed. To install, see instructions.Next, we import plotting libraries and configure the plotting style.

Loading Data

The input to StatsForecast is always a data frame in long format with

three columns: unique_id, ds and y:

-

The

unique_id(string, int or category) represents an identifier for the series. -

The

ds(datestamp) column should be of a format expected by Pandas, ideally YYYY-MM-DD for a date or YYYY-MM-DD HH:MM:SS for a timestamp. -

The

y(numeric) represents the measurement we wish to forecast.

ds from the object type to datetime.

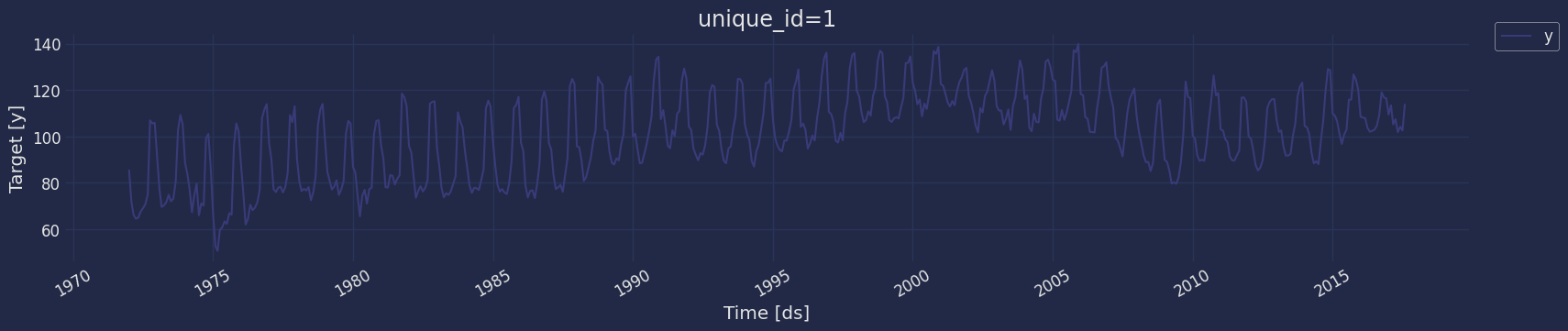

Explore data with the plot method

Plot a series using the plot method from the StatsForecast class. This method prints a random series from the dataset and is useful for basic EDA.

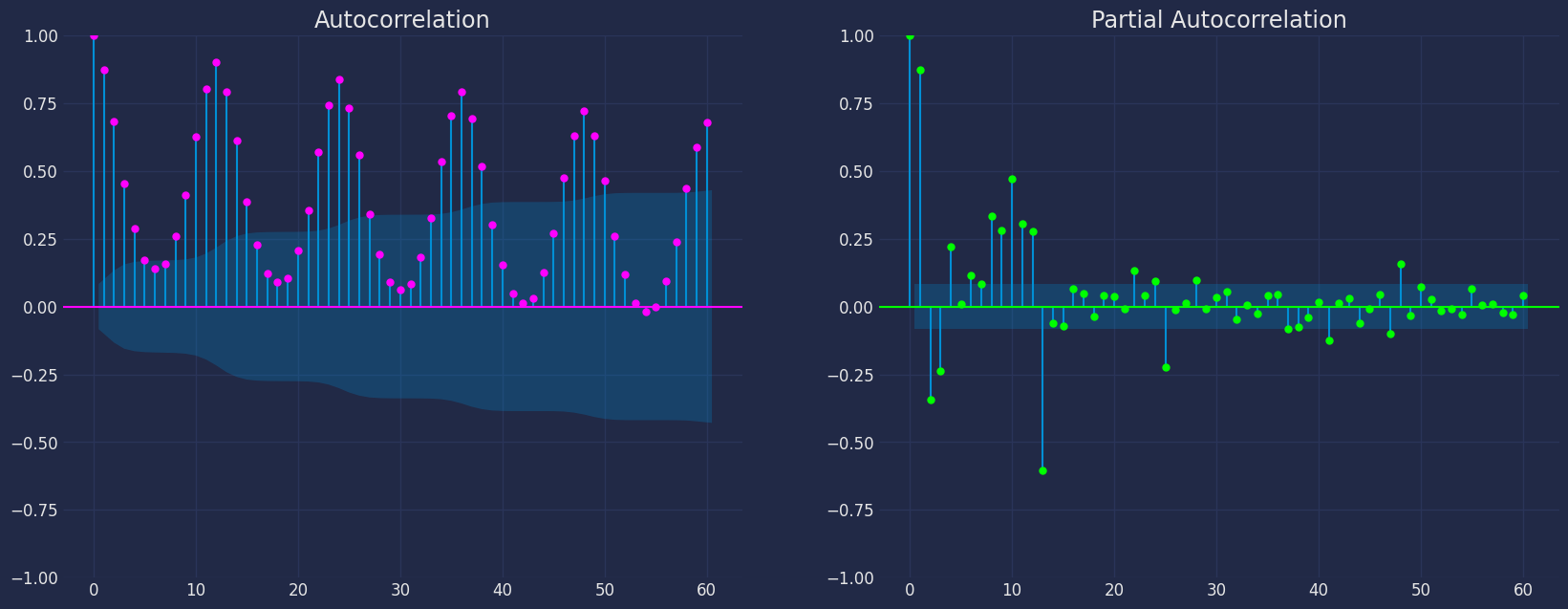

Autocorrelation plots

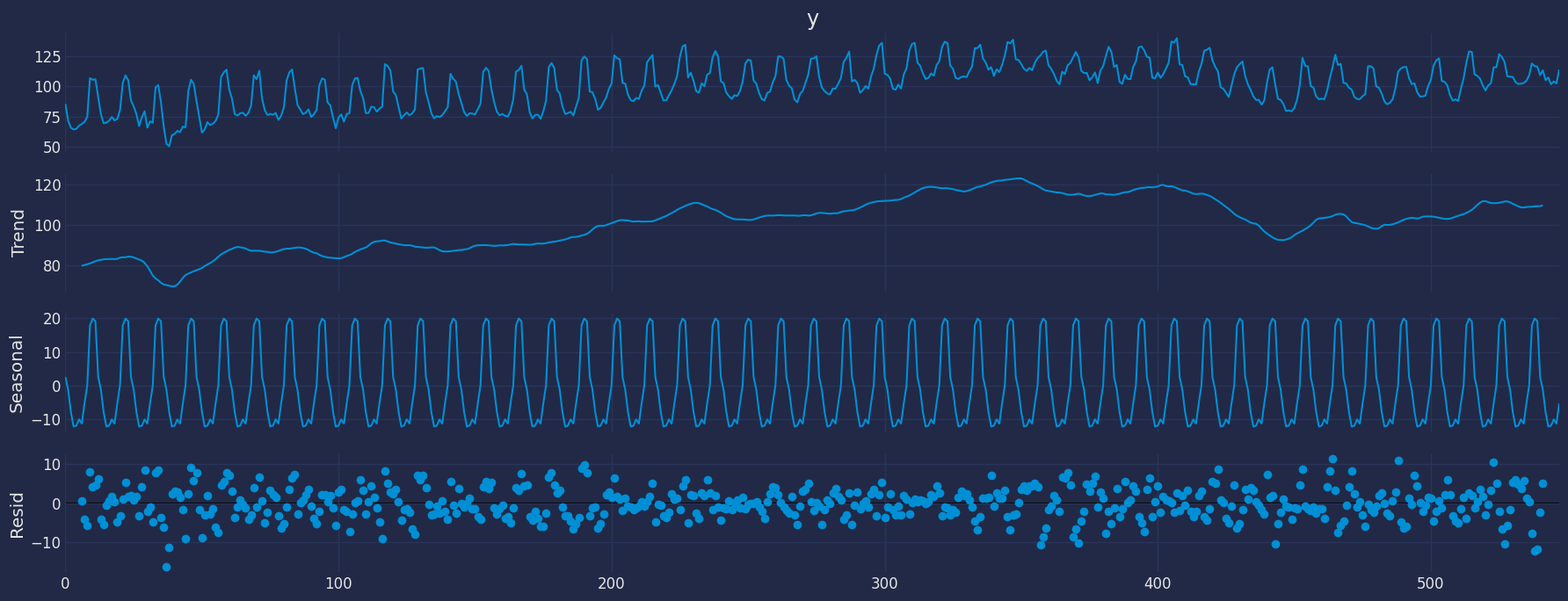

Decomposition of the time series

How to decompose a time series and why? In time series analysis to forecast new values, it is very important to know past data. More formally, we can say that it is very important to know the patterns that values follow over time. There can be many reasons that cause our forecast values to fall in the wrong direction. Basically, a time series consists of four components. The variation of those components causes the change in the pattern of the time series. These components are:- Level: This is the primary value that averages over time.

- Trend: The trend is the value that causes increasing or decreasing patterns in a time series.

- Seasonality: This is a cyclical event that occurs in a time series for a short time and causes short-term increasing or decreasing patterns in a time series.

- Residual/Noise: These are the random variations in the time series.

Multiplicative time series

If the components of the time series are multiplicative together, then the time series is called a multiplicative time series. For visualization, if the time series is having exponential growth or decline with time, then the time series can be considered as the multiplicative time series. The mathematical function of the multiplicative time series can be represented as.

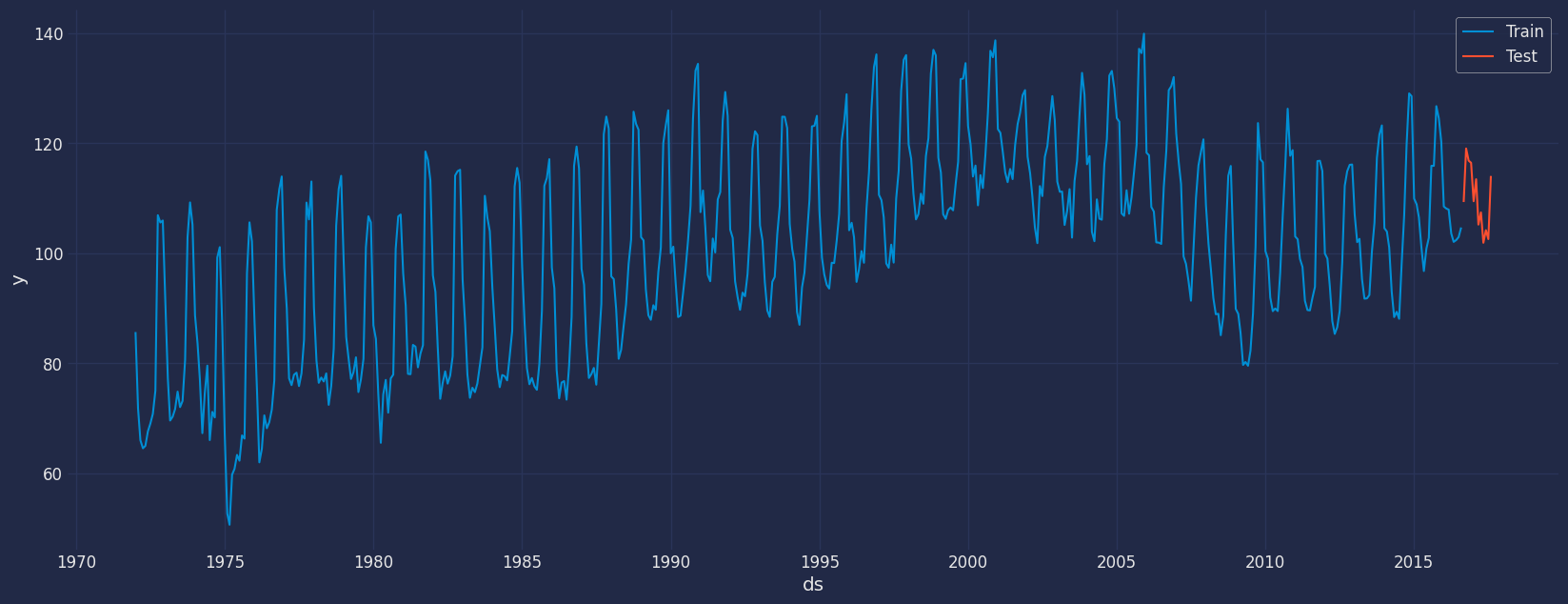

Split the data into training and testing

Let’s divide our data into sets 1. Data to train ourAutoArima model

2. Data to test our model

For the test data we will use the last 12 months to test and evaluate

the performance of our model.

Implementation of AutoArima with StatsForecast

Load libraries

Instantiating Model

Import and instantiate the models. Setting the argument is sometimes tricky. This article on Seasonal periods) by the master, Rob Hyndmann, can be useful.season_length-

freq:a string indicating the frequency of the data. (See panda’s available frequencies.) -

n_jobs:n_jobs: int, number of jobs used in the parallel processing, use -1 for all cores. -

fallback_model:a model to be used if a model fails.

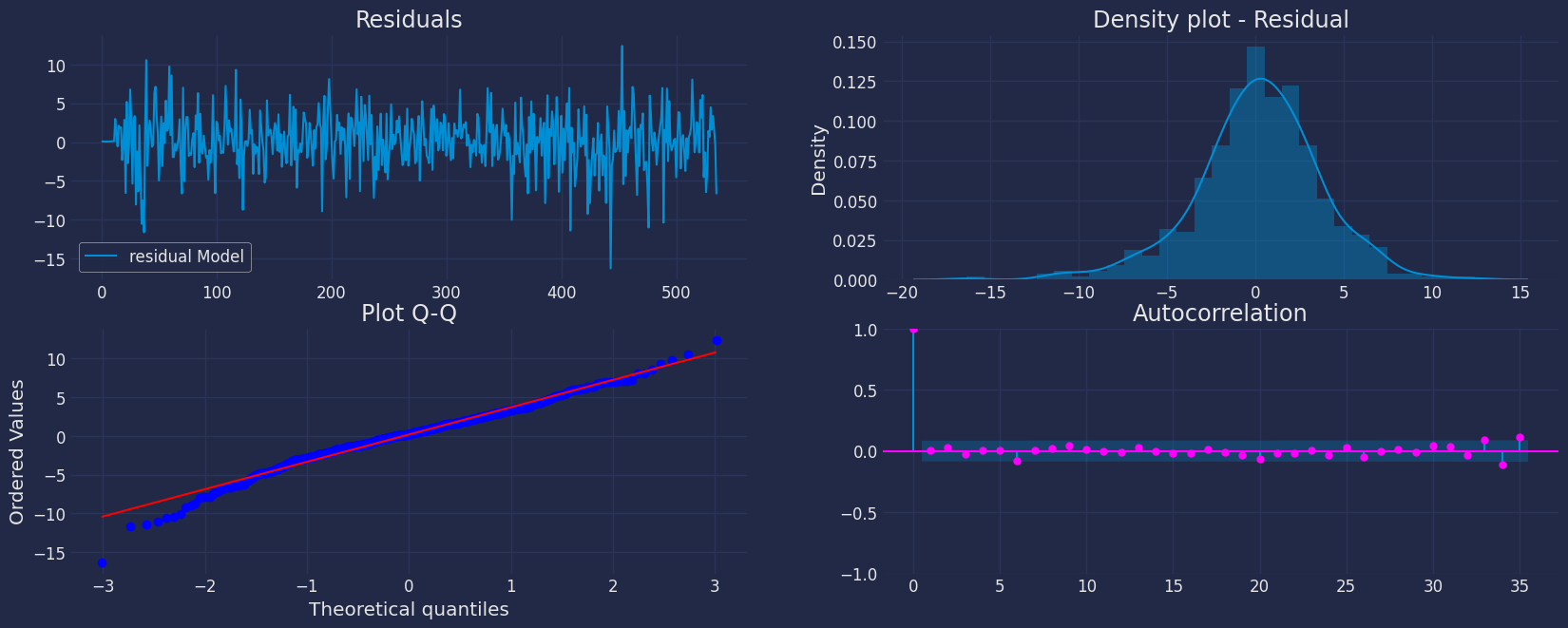

Fit the Model

arima_string function

to see the parameters that the model has found.

ARIMA(4,0,3)(0,1,1)[12], this means that our model contains

, that is, it has a non-seasonal autogressive element, on the

other hand, our model contains a seasonal part, which has an order of

, that is, it has a seasonal differential, and that contains

3 moving average element.

To know the values of the terms of our model, we can use the following

statement to know all the result of the model made.

.get() function to extract the element and then we are going to save

it in a pd.DataFrame().

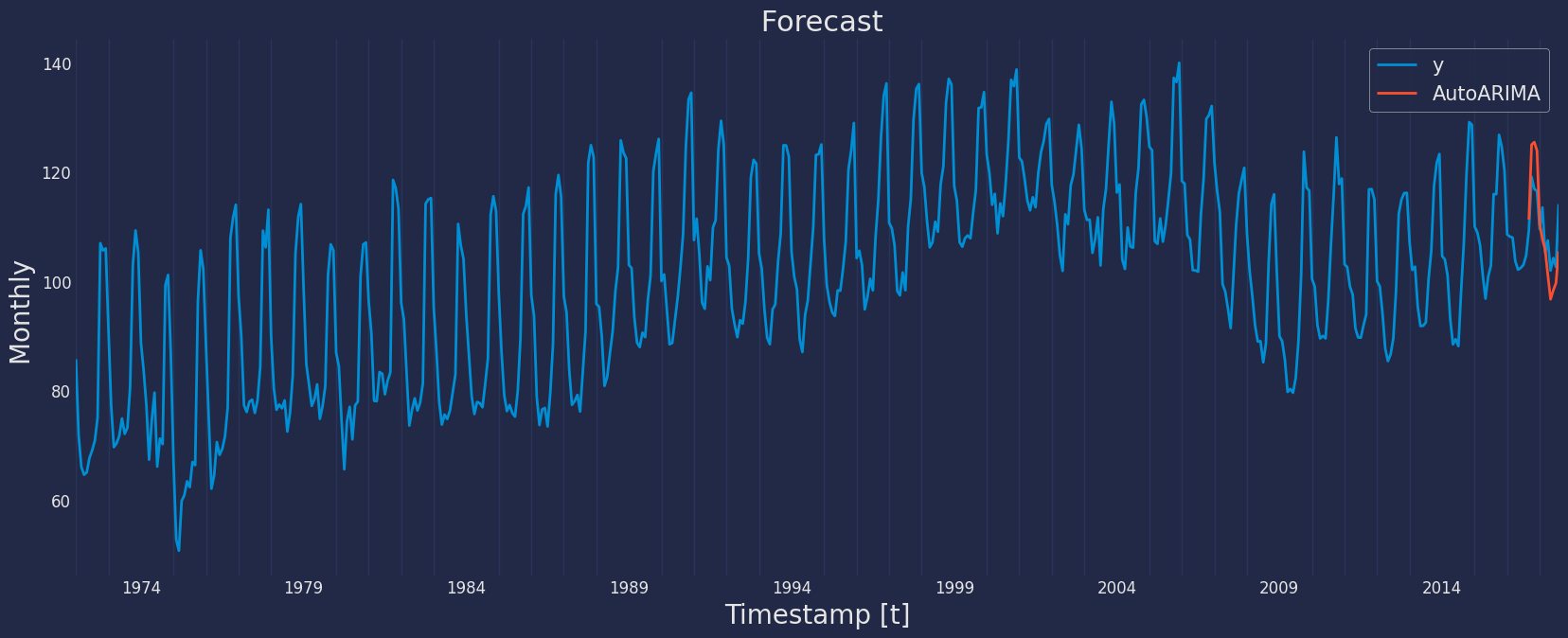

Forecast Method

If you want to gain speed in productive settings where you have multiple series or models we recommend using theStatsForecast.forecast method

instead of .fit and .predict.

The main difference is that the .forecast doest not store the fitted

values and is highly scalable in distributed environments.

The forecast method takes two arguments: forecasts next h (horizon)

and level.

-

h (int):represents the forecast h steps into the future. In this case, 12 months ahead. -

level (list of floats):this optional parameter is used for probabilistic forecasting. Set the level (or confidence percentile) of your prediction interval. For example,level=[90]means that the model expects the real value to be inside that interval 90% of the times.

ARIMA and Theta)

Adding 95% confidence interval with the forecast method

Predict method with confidence interval

To generate forecasts use the predict method. The predict method takes two arguments: forecasts the nexth (for

horizon) and level.

-

h (int):represents the forecast h steps into the future. In this case, 12 months ahead. -

level (list of floats):this optional parameter is used for probabilistic forecasting. Set the level (or confidence percentile) of your prediction interval. For example,level=[95]means that the model expects the real value to be inside that interval 95% of the times.

We can join the forecast result with the historical data using the

pandas function

pd.concat(), and then be able to use this result for

graphing.

Now let’s visualize the result of our forecast and the historical data

of our time series, also let’s draw the confidence interval that we have

obtained when making the prediction with 95% confidence.

Cross-validation

In previous steps, we’ve taken our historical data to predict the future. However, to asses its accuracy we would also like to know how the model would have performed in the past. To assess the accuracy and robustness of your models on your data perform Cross-Validation. With time series data, Cross Validation is done by defining a sliding window across the historical data and predicting the period following it. This form of cross-validation allows us to arrive at a better estimation of our model’s predictive abilities across a wider range of temporal instances while also keeping the data in the training set contiguous as is required by our models. The following graph depicts such a Cross Validation Strategy:

Perform time series cross-validation

Cross-validation of time series models is considered a best practice but most implementations are very slow. The statsforecast library implements cross-validation as a distributed operation, making the process less time-consuming to perform. If you have big datasets you can also perform Cross Validation in a distributed cluster using Ray, Dask or Spark. In this case, we want to evaluate the performance of each model for the last 5 months(n_windows=5), forecasting every second months

(step_size=12). Depending on your computer, this step should take

around 1 min.

The cross_validation method from the StatsForecast class takes the

following arguments.

-

df:training data frame -

h (int):represents h steps into the future that are being forecasted. In this case, 12 months ahead. -

step_size (int):step size between each window. In other words: how often do you want to run the forecasting processes. -

n_windows(int):number of windows used for cross validation. In other words: what number of forecasting processes in the past do you want to evaluate.

unique_id:series identifierds:datestamp or temporal indexcutoff:the last datestamp or temporal index for the n_windows.y:true value"model":columns with the model’s name and fitted value.