mlforecast. We train a model on one domain (M4 Monthly

Macro series) and then generate calibrated prediction intervals for

a different domain (M4 Monthly Finance series) — without retraining

the model.

Why transfer?

Standard conformal prediction intervals are calibrated on the same distribution as training data. When you apply a pretrained model to new, unseen series from a potentially different domain, the source conformity scores may be miscalibrated for the target domain. Transfer conformal methods attempt to correct for this shift using different strategies:

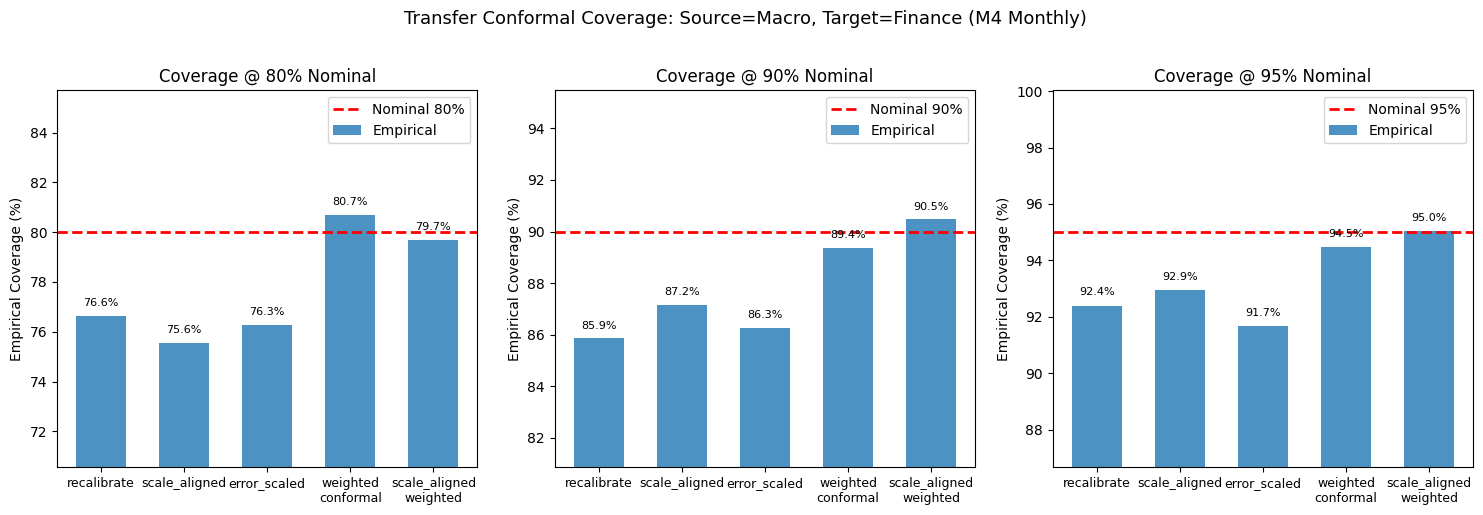

We evaluate each method’s empirical coverage — the fraction of test

observations that fall inside the predicted interval — and compare it to

the nominal level.

Setup

Load M4 Monthly Data

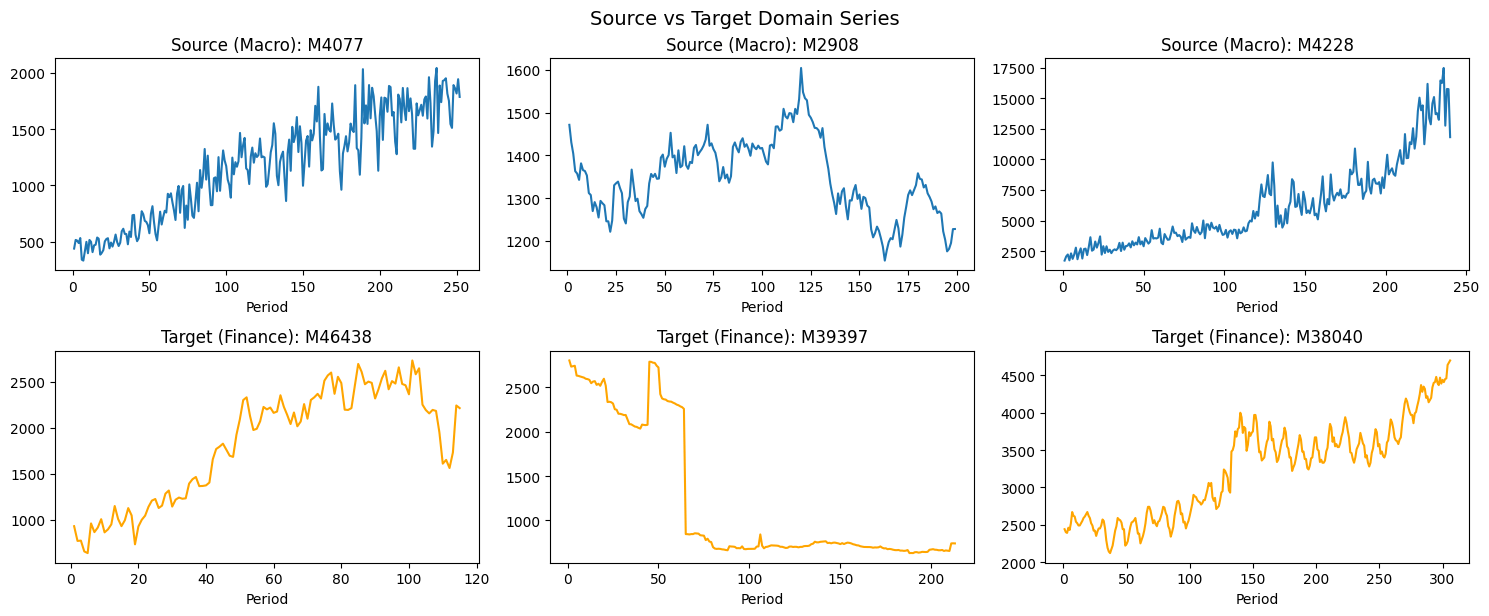

The M4 Monthly dataset contains 48,000 monthly time series across 6 categories. We use it to create a cross-domain transfer scenario:- Source domain:

Macrocategory — macroeconomic time series - Target domain:

Financecategory — financial time series

Create Source and Target Domains

Explore the Domains

Let’s visualize a few series from each domain to get a sense of the distribution shift.

Fit MLForecast on Source Domain

Feature engineering for cross-domain transfer

Because the model is trained on one domain and applied to another, the features must be scale-invariant. Tree models cannot extrapolate: if a Finance series has level changes larger than anything seen in the Macro training data, its predictions get clamped to the training range, producing large, skewed errors that no conformal correction can fully repair. We therefore model log-returns instead of raw differences:GlobalSklearnTransformer(FunctionTransformer(np.log1p, np.expm1))followed byDifferences([1])— the model sees relative changes, which live on a comparable scale in both domains. Back-transformed intervals scale multiplicatively with each series’ level.- Volatility and trend features (

RollingStd,ExponentiallyWeightedMean,SeasonalRollingMean) — these sharpen the point forecasts and, importantly, give the density-ratio estimator meaningful covariates: on the raw scale, lag features mostly encode the scale difference between domains rather than the dynamics.

Prediction interval configuration

We fit on Macro series usingPredictionIntervals with: -

method='weighted_conformal_error' — stores lag features in the

conformity score dataframe, enabling density-ratio estimation (DRE) for

the weighted_conformal and scale_aligned_weighted transfer

methods. - scale_estimator='mad' — stores per-series scale estimates

(MAD of first differences), enabling the scale_aligned and

scale_aligned_weighted transfer methods.

Using this single fit configuration unlocks all five transfer

methods.

Evaluate Transfer Methods

For each transfer method, we callmlf.predict() with: -

new_df=target_train — the target domain training history (Finance

series) - level=[80, 90, 95] — the requested coverage levels -

transfer_conformal=method — which transfer strategy to use

We then merge predictions with target_test and compute the empirical

coverage at each level.

Results: Nominal vs Empirical Coverage

A well-calibrated method should have empirical coverage close to nominal. We show the results as a summary table and a bar chart.

Coverage Gap Analysis

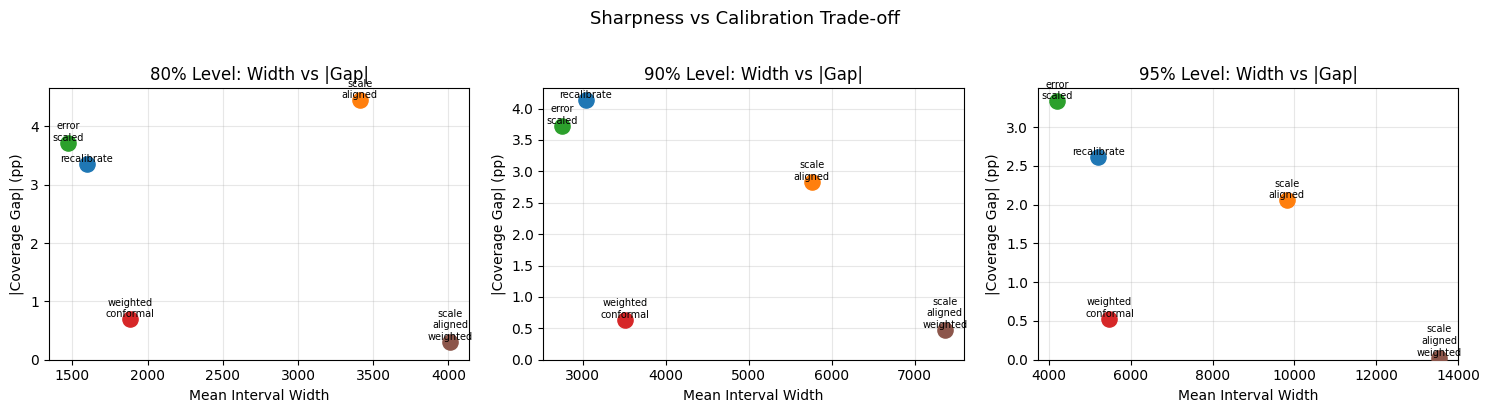

Interval Width Analysis

Beyond coverage, we also care about interval sharpness. Narrower intervals (lower width) are better, as long as coverage is maintained.

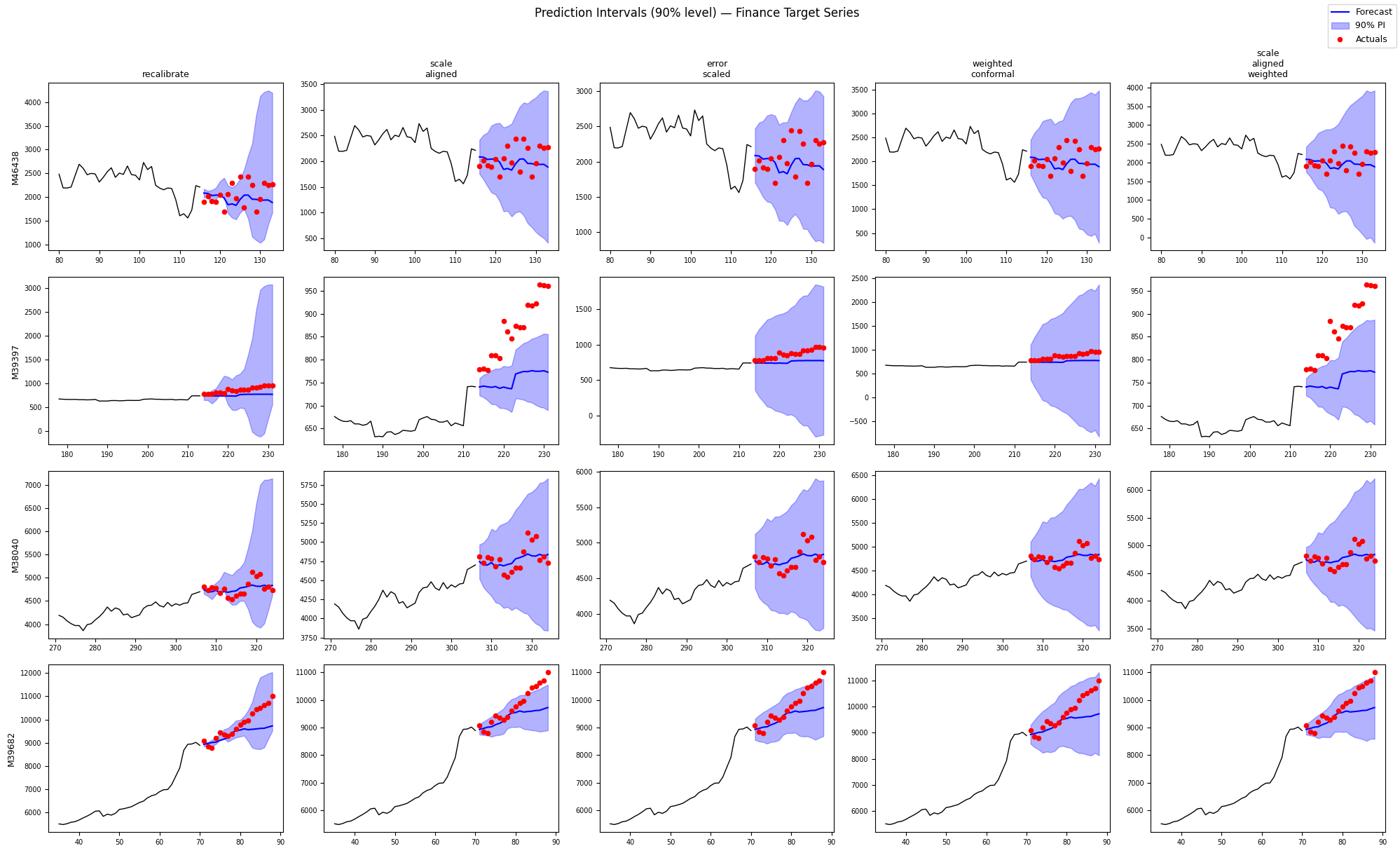

Visual Inspection: Interval Examples

Let’s visually inspect the intervals produced by each method for a few target-domain series.

Summary

The table and charts above show how each transfer method calibrates prediction intervals when moving from a Macro source domain to a Finance target domain in M4 Monthly data. Key takeaways:- Feature engineering matters as much as the transfer method.

Modeling log-returns (

log1p+Differences([1])) instead of raw differences makes the features scale-invariant across domains, removes the systematic point-forecast bias, and is what allows the weighted methods to reach near-nominal coverage. With raw differences, every method under-covers by several percentage points. recalibrateruns cross-validation on the target data — it tends to be the most directly calibrated but requires running CV (computationally equivalent to retraining).scale_aligneduses the scale of the y signal (MAD of differences) to align source residuals — zero-shot, no CV needed.error_scaledruns CV on the target data to estimate prediction error magnitude — a middle ground between full recalibration and scale alignment.weighted_conformaluses density-ratio estimation to reweight source conformity scores — handles covariate shift without needing target labels during calibration.scale_aligned_weightedcombines scale alignment with DRE weighting — the most sophisticated zero-shot method.- The residual under-coverage of the non-weighted methods comes from pooling conformity scores across heterogeneous series: pooled intervals are too wide for calm series and too narrow for volatile ones. This is precisely the failure mode the weighted/scale-aligned variants are designed to mitigate.

recalibrate or error_scaled - If you need zero-shot

transfer: scale_aligned or scale_aligned_weighted - If covariate

shift is the main concern: weighted_conformal or

scale_aligned_weighted