torch.nn.modules which helps to automatically moved

them across CPU/GPU/TPU devices with Pytorch Lightning.

BasePointLoss

Module

Base class for point loss functions.

Parameters:

1. Scale-dependent Errors

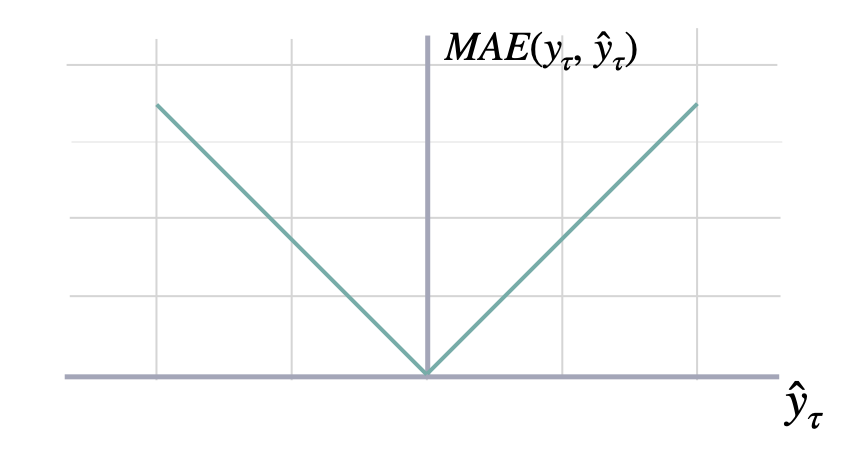

These metrics are on the same scale as the data.Mean Absolute Error (MAE)

MAE

BasePointLoss

Mean Absolute Error.

Calculates Mean Absolute Error between y and y_hat. MAE measures the relative prediction

accuracy of a forecasting method by calculating the deviation of the prediction and the true

value at a given time and averages these devations over the length of the series.

Parameters:

MAE.__call__

Returns:

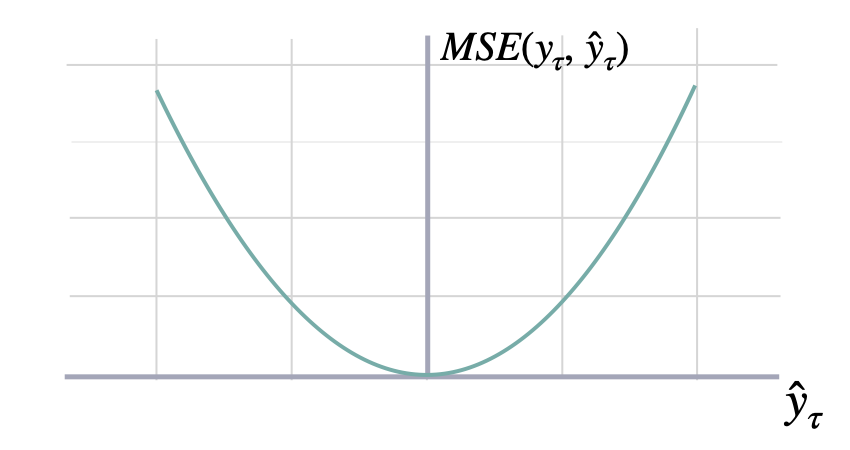

Mean Squared Error (MSE)

MSE

BasePointLoss

Mean Squared Error.

Calculates Mean Squared Error between y and y_hat. MSE measures the relative prediction

accuracy of a forecasting method by calculating the squared deviation of the prediction and the true

value at a given time, and averages these devations over the length of the series.

Parameters:

MSE.__call__

Returns:

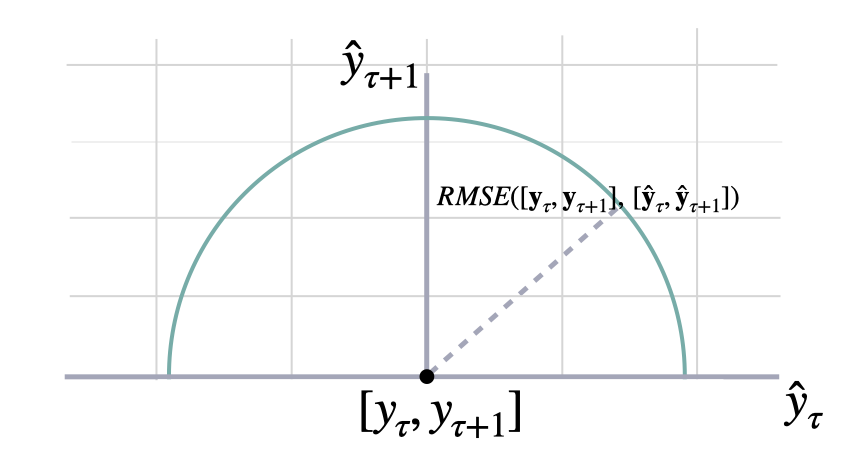

Root Mean Squared Error (RMSE)

RMSE

BasePointLoss

Root Mean Squared Error.

Calculates Root Mean Squared Error between y and y_hat. RMSE measures the relative prediction

accuracy of a forecasting method by calculating the squared deviation of the prediction and the observed value at

a given time and averages these devations over the length of the series.

Finally the RMSE will be in the same scale as the original time series so its comparison with other

series is possible only if they share a common scale. RMSE has a direct connection to the L2 norm.

Parameters:

RMSE.__call__

Returns:

2. Percentage errors

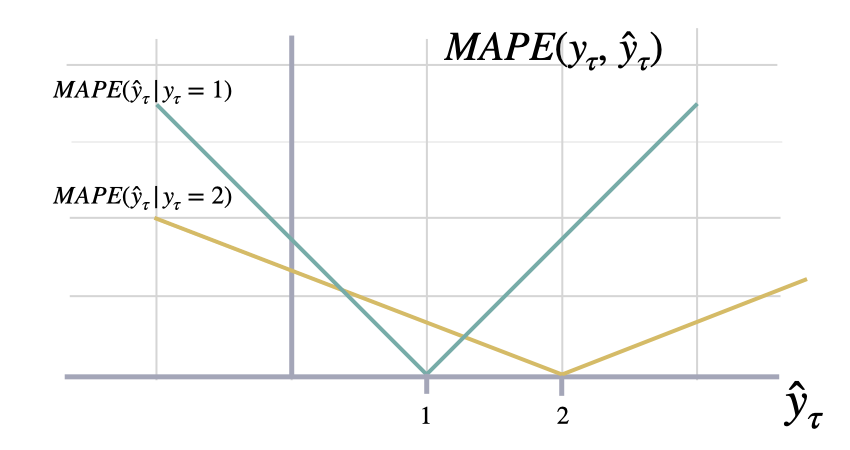

These metrics are unit-free, suitable for comparisons across series.Mean Absolute Percentage Error (MAPE)

MAPE

BasePointLoss

Mean Absolute Percentage Error

Calculates Mean Absolute Percentage Error between

y and y_hat. MAPE measures the relative prediction

accuracy of a forecasting method by calculating the percentual deviation

of the prediction and the observed value at a given time and

averages these devations over the length of the series.

The closer to zero an observed value is, the higher penalty MAPE loss

assigns to the corresponding error.

Parameters:

MAPE.__call__

Returns:

Symmetric MAPE (sMAPE)

SMAPE

BasePointLoss

Symmetric Mean Absolute Percentage Error

Calculates Symmetric Mean Absolute Percentage Error between

y and y_hat. SMAPE measures the relative prediction

accuracy of a forecasting method by calculating the relative deviation

of the prediction and the observed value scaled by the sum of the

absolute values for the prediction and observed value at a

given time, then averages these devations over the length

of the series. This allows the SMAPE to have bounds between

0% and 200% which is desireble compared to normal MAPE that

may be undetermined when the target is zero.

Parameters:

SMAPE.__call__

Returns:

3. Scale-independent Errors

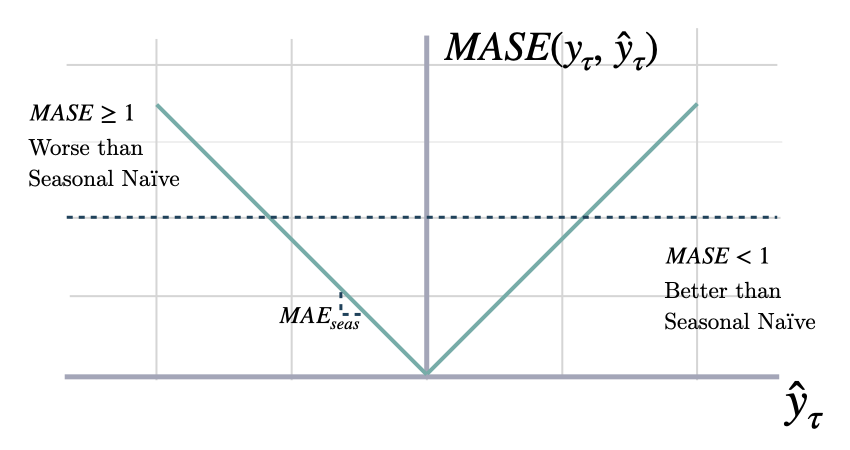

These metrics measure the relative improvements versus baselines.Mean Absolute Scaled Error (MASE)

MASE

BasePointLoss

Mean Absolute Scaled Error

Calculates the Mean Absolute Scaled Error between

y and y_hat. MASE measures the relative prediction

accuracy of a forecasting method by comparinng the mean absolute errors

of the prediction and the observed value against the mean

absolute errors of the seasonal naive model.

The MASE partially composed the Overall Weighted Average (OWA),

used in the M4 Competition.

Parameters:

MASE.__call__

Returns:

Relative Mean Squared Error (relMSE)

relMSE

BasePointLoss

Relative Mean Squared Error

Computes Relative Mean Squared Error (relMSE), as proposed by Hyndman & Koehler (2006)

as an alternative to percentage errors, to avoid measure unstability.

Parameters:

relMSE.__call__

Returns:

4. Probabilistic Errors

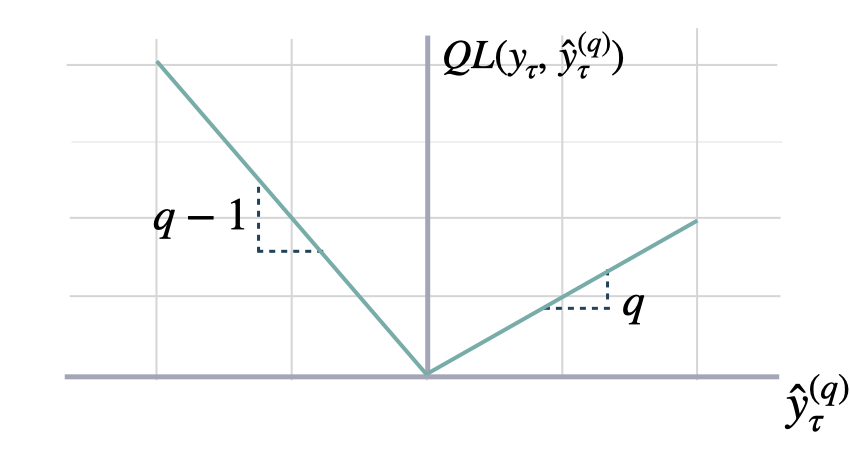

These methods use statistical approaches for estimating unknown probability distributions using observed data. Maximum likelihood estimation involves finding the parameter values that maximize the likelihood function, which measures the probability of obtaining the observed data given the parameter values. MLE has good theoretical properties and efficiency under certain satisfied assumptions. On the non-parametric approach, quantile regression measures non-symmetrically deviation, producing under/over estimation.Quantile Loss

QuantileLoss

BasePointLoss

Quantile Loss.

Computes the quantile loss between y and y_hat.

QL measures the deviation of a quantile forecast.

By weighting the absolute deviation in a non symmetric way, the

loss pays more attention to under or over estimation.

A common value for q is 0.5 for the deviation from the median (Pinball loss).

Parameters:

QuantileLoss.__call__

Returns:

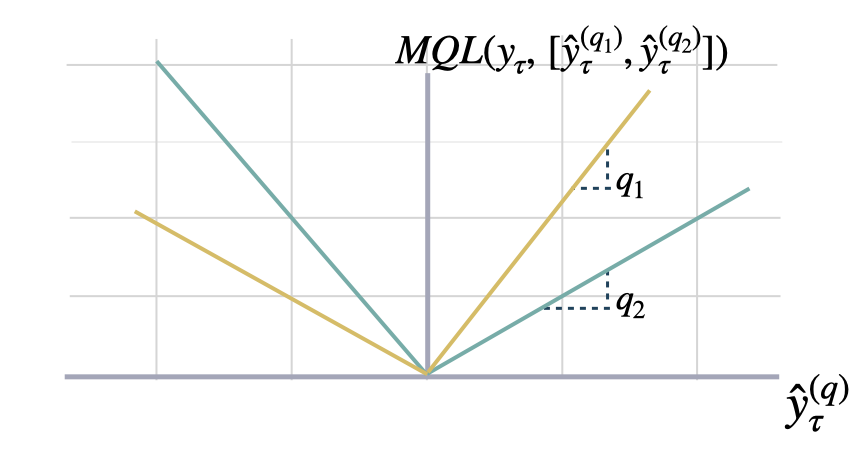

Multi Quantile Loss (MQLoss)

MQLoss

BasePointLoss

Multi-Quantile loss

Calculates the Multi-Quantile loss (MQL) between y and y_hat.

MQL calculates the average multi-quantile Loss for

a given set of quantiles, based on the absolute

difference between predicted quantiles and observed values.

The limit behavior of MQL allows to measure the accuracy

of a full predictive distribution with

the continuous ranked probability score (CRPS). This can be achieved

through a numerical integration technique, that discretizes the quantiles

and treats the CRPS integral with a left Riemann approximation, averaging over

uniformly distanced quantiles.

Parameters:

MQLoss.__call__

Returns:

Implicit Quantile Loss (IQLoss)

QuantileLayer

Module

Implicit Quantile Layer from the paper IQN for Distributional Reinforcement Learning.

Code from GluonTS: https://github.com/awslabs/gluonts/blob/61133ef6e2d88177b32ace4afc6843ab9a7bc8cd/src/gluonts/torch/distributions/implicit_quantile_network.py

IQLoss

QuantileLoss

Implicit Quantile Loss.

Computes the quantile loss between y and y_hat, with the quantile q provided as an input to the network.

IQL measures the deviation of a quantile forecast.

By weighting the absolute deviation in a non symmetric way, the

loss pays more attention to under or over estimation.

Parameters:

IQLoss.__call__

Returns:

DistributionLoss

DistributionLoss

Module

DistributionLoss

This PyTorch module wraps the torch.distribution classes allowing it to

interact with NeuralForecast models modularly. It shares the negative

log-likelihood as the optimization objective and a sample method to

generate empirically the quantiles defined by the level list.

Additionally, it implements a distribution transformation that factorizes the

scale-dependent likelihood parameters into a base scale and a multiplier

efficiently learnable within the network’s non-linearities operating ranges.

Available distributions:

- Poisson

- Normal

- StudentT

- NegativeBinomial

- Tweedie

- Bernoulli (Temporal Classifiers)

- ISQF (Incremental Spline Quantile Function)

Returns:

DistributionLoss.__call__

mask tensor.

Parameters:

Returns:

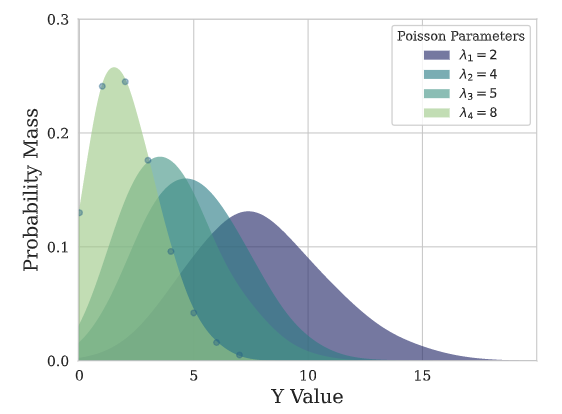

Poisson Mixture Mesh (PMM)

PMM

Module

Poisson Mixture Mesh

This Poisson Mixture statistical model assumes independence across groups of

data , and estimates relationships within the group.

Parameters:

PMM.__call__

mask tensor.

Parameters:

Returns:

Gaussian Mixture Mesh (GMM)

GMM

Module

Gaussian Mixture Mesh

This Gaussian Mixture statistical model assumes independence across groups of

data , and estimates relationships within the group.

Parameters:

GMM.__call__

mask tensor.

Parameters:

Returns:

Negative Binomial Mixture Mesh (NBMM)

NBMM

Module

Negative Binomial Mixture Mesh

This N. Binomial Mixture statistical model assumes independence across groups of

data , and estimates relationships within the group.

Parameters:

NBMM.__call__

mask tensor.

Parameters:

Returns:

5. Robustified Errors

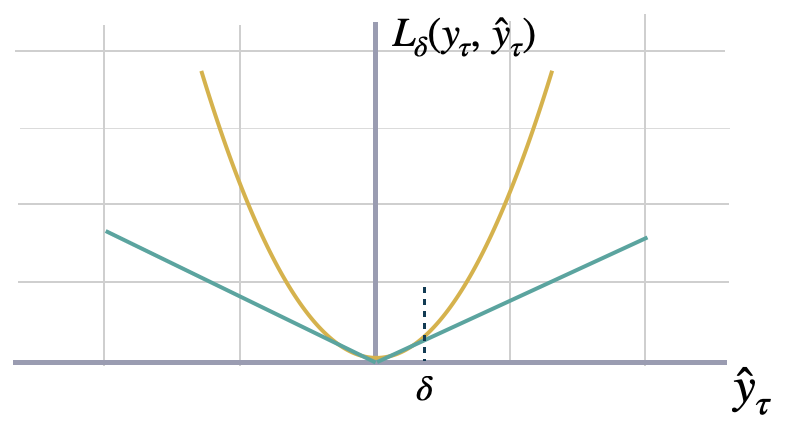

Huber Loss

HuberLoss

BasePointLoss

Huber Loss

The Huber loss, employed in robust regression, is a loss function that

exhibits reduced sensitivity to outliers in data when compared to the

squared error loss. This function is also refered as SmoothL1.

The Huber loss function is quadratic for small errors and linear for large

errors, with equal values and slopes of the different sections at the two

points where =.

where is a threshold parameter that determines the point at which the loss transitions from quadratic to linear,

and can be tuned to control the trade-off between robustness and accuracy in the predictions.

Parameters:

HuberLoss.__call__

Returns:

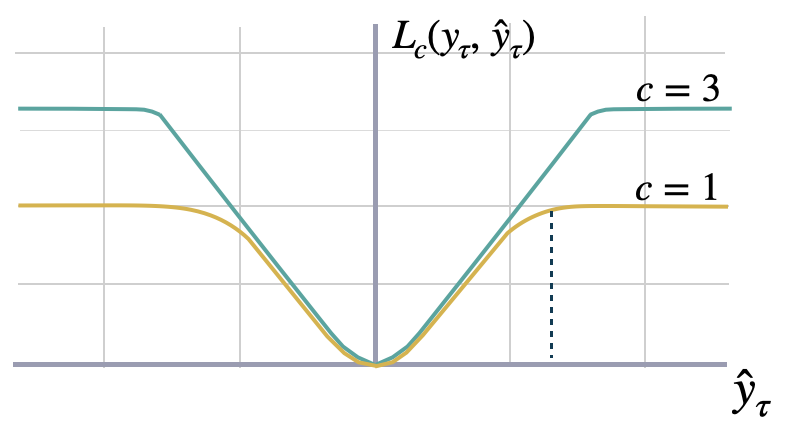

Tukey Loss

TukeyLoss

BasePointLoss

Tukey Loss

The Tukey loss function, also known as Tukey’s biweight function, is a

robust statistical loss function used in robust statistics. Tukey’s loss exhibits

quadratic behavior near the origin, like the Huber loss; however, it is even more

robust to outliers as the loss for large residuals remains constant instead of

scaling linearly.

The parameter in Tukey’s loss determines the ”saturation” point

of the function: Higher values of enhance sensitivity, while lower values

increase resistance to outliers.

Please note that the Tukey loss function assumes the data to be stationary or

normalized beforehand. If the error values are excessively large, the algorithm

may need help to converge during optimization. It is advisable to employ small learning rates.

Parameters:

TukeyLoss.__call__

Returns:

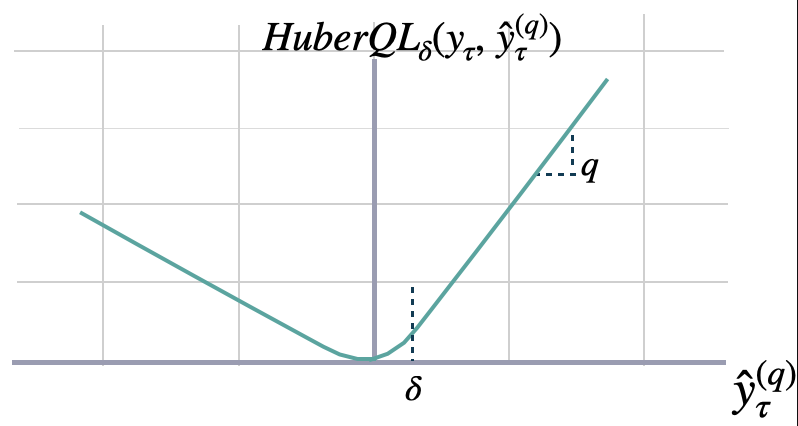

Huberized Quantile Loss

HuberQLoss

BasePointLoss

Huberized Quantile Loss

The Huberized quantile loss is a modified version of the quantile loss function that

combines the advantages of the quantile loss and the Huber loss. It is commonly used

in regression tasks, especially when dealing with data that contains outliers or heavy tails.

The Huberized quantile loss between y and y_hat measure the Huber Loss in a non-symmetric way.

The loss pays more attention to under/over-estimation depending on the quantile parameter ;

and controls the trade-off between robustness and accuracy in the predictions with the parameter .

Parameters:

HuberQLoss.__call__

Returns:

Huberized MQLoss

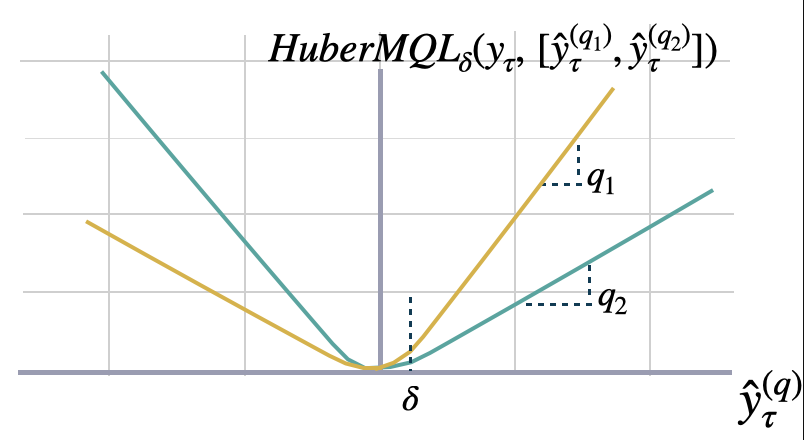

HuberMQLoss

BasePointLoss

Huberized Multi-Quantile loss

The Huberized Multi-Quantile loss (HuberMQL) is a modified version of the multi-quantile loss function

that combines the advantages of the quantile loss and the Huber loss. HuberMQL is commonly used in regression

tasks, especially when dealing with data that contains outliers or heavy tails. The loss function pays

more attention to under/over-estimation depending on the quantile list parameter.

It controls the trade-off between robustness and prediction accuracy with the parameter .

Parameters:

HuberMQLoss.__call__

Returns:

Huberized IQLoss

HuberIQLoss

HuberQLoss

Implicit Huber Quantile Loss

Computes the huberized quantile loss between y and y_hat, with the quantile q provided as an input to the network.

HuberIQLoss measures the deviation of a huberized quantile forecast.

By weighting the absolute deviation in a non symmetric way, the

loss pays more attention to under or over estimation.

Parameters:

HuberIQLoss.__call__

Returns:

6. Others

Accuracy

Accuracy

BasePointLoss

Accuracy

Computes the accuracy between categorical y and y_hat.

This evaluation metric is only meant for evalution, as it

is not differentiable.

Accuracy.__call__

Returns:

Scaled Continuous Ranked Probability Score (sCRPS)

sCRPS

BasePointLoss

Scaled Continues Ranked Probability Score

Calculates a scaled variation of the CRPS, as proposed by Rangapuram (2021),

to measure the accuracy of predicted quantiles y_hat compared to the observation y.

This metric averages percentual weighted absolute deviations as

defined by the quantile losses.

where is the estimated quantile, and

are the target variable realizations.

Parameters:

sCRPS.__call__

Returns: