1. Scale-dependent Errors

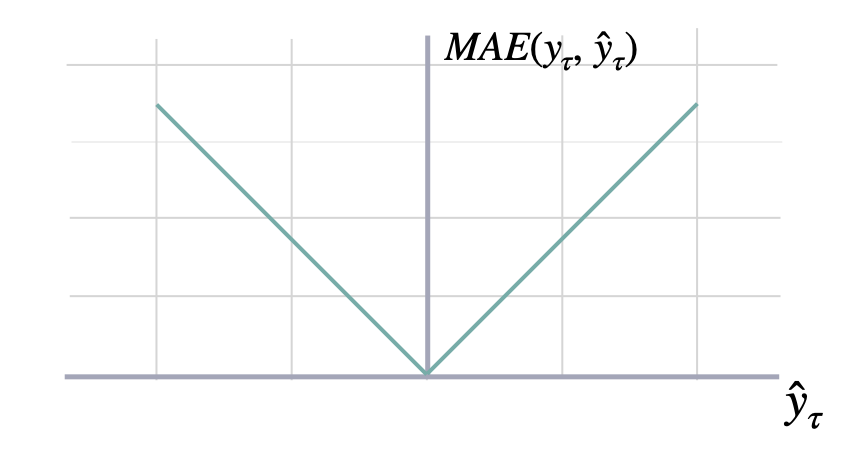

Mean Absolute Error

mae

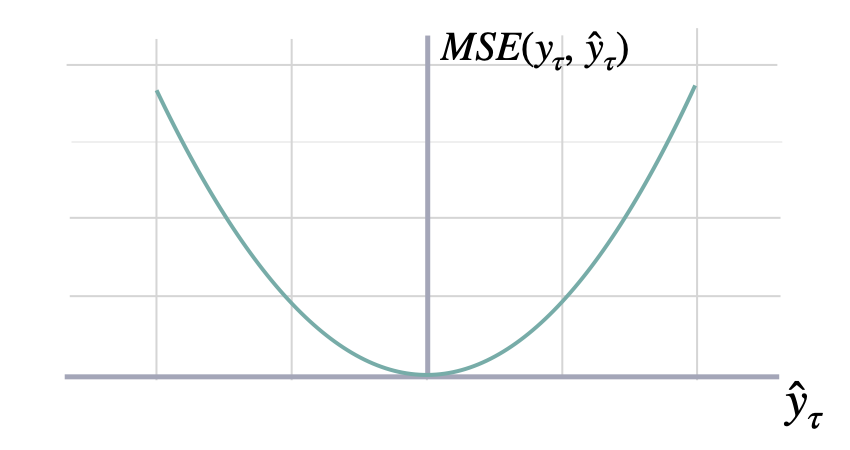

Mean Squared Error

mse

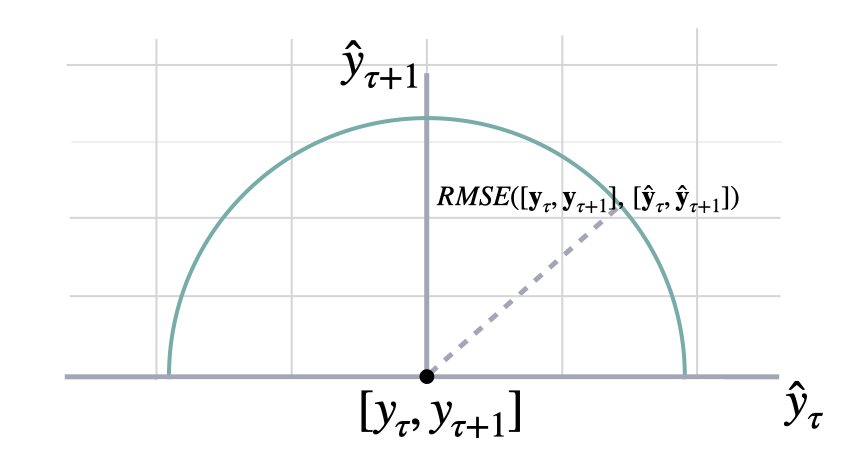

Root Mean Squared Error

rmse

Bias

bias

Cumulative Forecast Error

cfe

Absolute Periods In Stock

pis

Linex

where must be .linex

- If a > 0, under-forecasting () is penalized more.

- If a < 0, over-forecasting () is penalized more.

- a must not be 0.

2. Percentage Errors

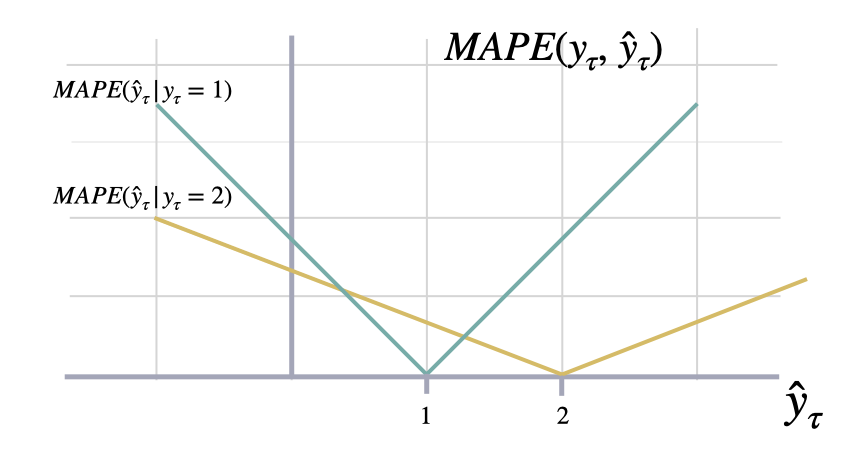

Mean Absolute Percentage Error

mape

Symmetric Mean Absolute Percentage Error

smape

3. Scale-independent Errors

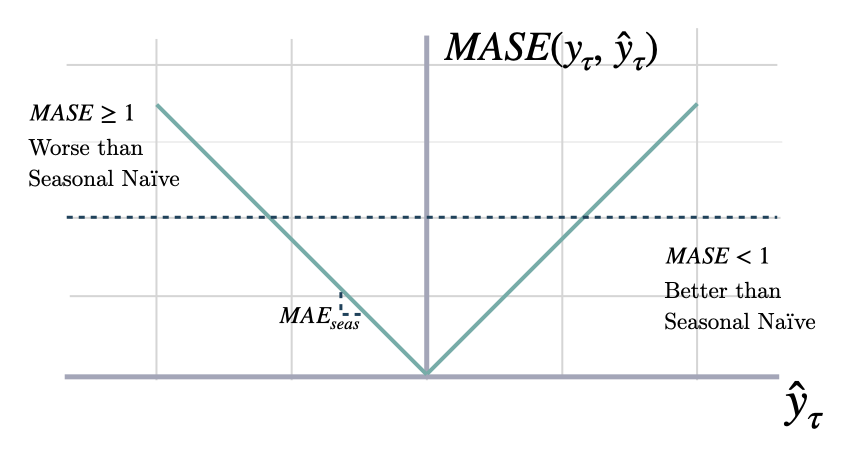

Mean Absolute Scaled Error

mase

Returns:

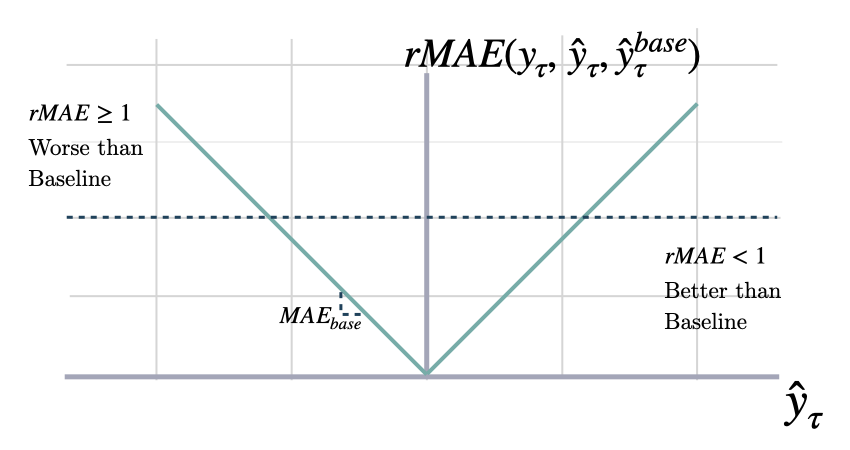

Relative Mean Absolute Error

rmae

Returns:

Normalized Deviation

nd

Mean Squared Scaled Error

msse

Returns:

Root Mean Squared Scaled Error

rmsse

Returns:

Scaled Absolute Periods In Stock

where .spis

Returns:

4. Probabilistic Errors

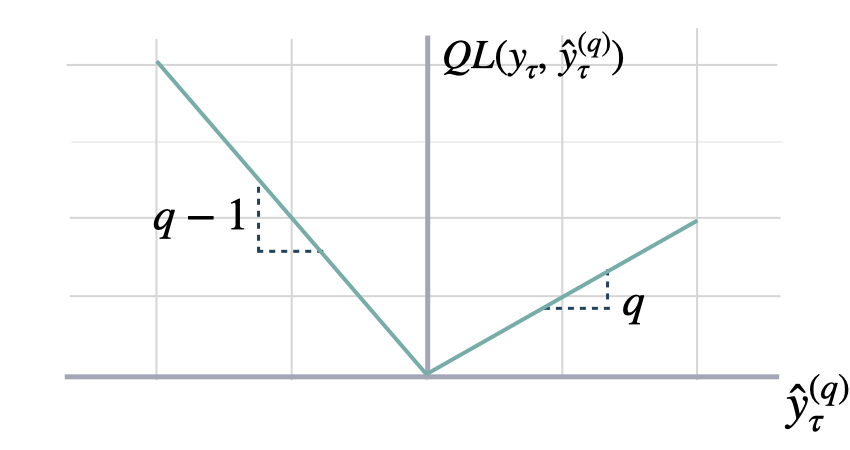

Quantile Loss

quantile_loss

Returns:

Scaled Quantile Loss

scaled_quantile_loss

Returns:

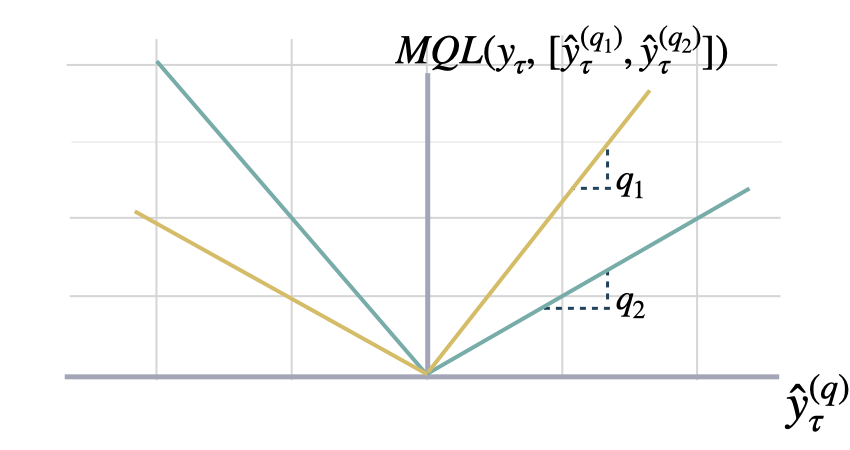

Multi-Quantile Loss

mqloss

Returns:

Scaled Multi-Quantile Loss

scaled_mqloss

Returns:

Coverage

coverage

Returns:

Calibration

calibration

Returns:

CRPS

Where is the an estimated multivariate distribution, and are its realizations.scaled_crps

y_hat compared to the observation y.

This metric averages percentual weighted absolute deviations as

defined by the quantile losses.

Parameters:

Returns:

Tweedie Deviance

For a set of forecasts and observations , the mean Tweedie deviance with power is where the unit-scaled deviance for each pair is- are the true values, the predicted means.

- controls the variance relationship .

- When , this smoothly interpolates between Poisson () and Gamma () deviance.

tweedie_deviance

power parameter defines the specific compound distribution:

- 1: Poisson

- (1, 2): Compound Poisson-Gamma

- 2: Gamma

-

2: Inverse Gaussian

Returns: