> ## Documentation Index

> Fetch the complete documentation index at: https://nixtlaverse.nixtla.io/llms.txt

> Use this file to discover all available pages before exploring further.

# Losses

> Loss functions for model evaluation.

The most important train signal is the forecast error, which is the

difference between the observed value $y_{\tau}$ and the prediction

$\hat{y}_{\tau}$, at time $y_{\tau}$:

```math theme={null}

e_{\tau} = y_{\tau}-\hat{y}_{\tau} \qquad \qquad \tau \in \{t+1,\dots,t+H \}

```

The train loss summarizes the forecast errors in different evaluation

metrics.

## 1. Scale-dependent Errors

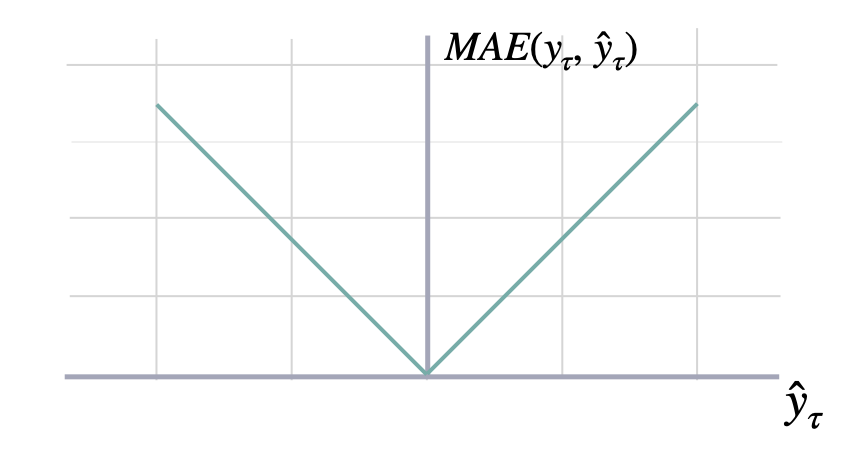

### Mean Absolute Error

```math theme={null}

\mathrm{MAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} |y_{\tau} - \hat{y}_{\tau}|

```

#### `mae`

```python theme={null}

mae(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Mean Absolute Error (MAE)

MAE measures the relative prediction

accuracy of a forecasting method by calculating the

deviation of the prediction and the true

value at a given time and averages these devations

over the length of the series.

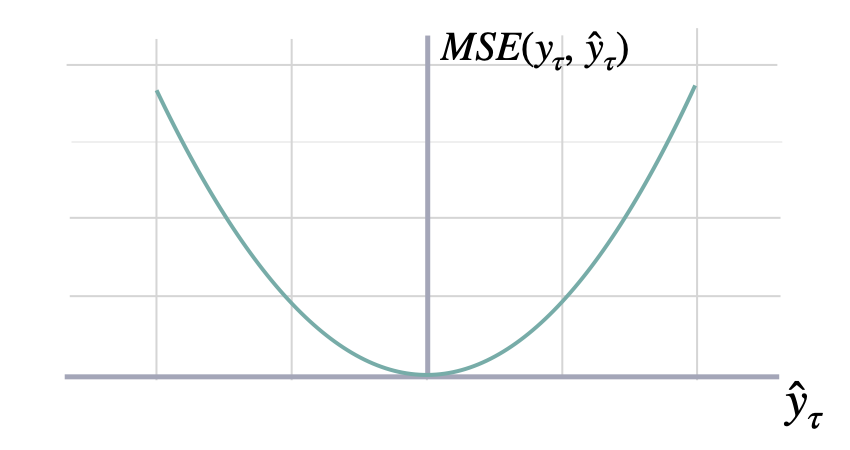

### Mean Squared Error

```math theme={null}

\mathrm{MSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} (y_{\tau} - \hat{y}_{\tau})^{2}

```

#### `mae`

```python theme={null}

mae(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Mean Absolute Error (MAE)

MAE measures the relative prediction

accuracy of a forecasting method by calculating the

deviation of the prediction and the true

value at a given time and averages these devations

over the length of the series.

### Mean Squared Error

```math theme={null}

\mathrm{MSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} (y_{\tau} - \hat{y}_{\tau})^{2}

```

#### `mse`

```python theme={null}

mse(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Mean Squared Error (MSE)

MSE measures the relative prediction

accuracy of a forecasting method by calculating the

squared deviation of the prediction and the true

value at a given time, and averages these devations

over the length of the series.

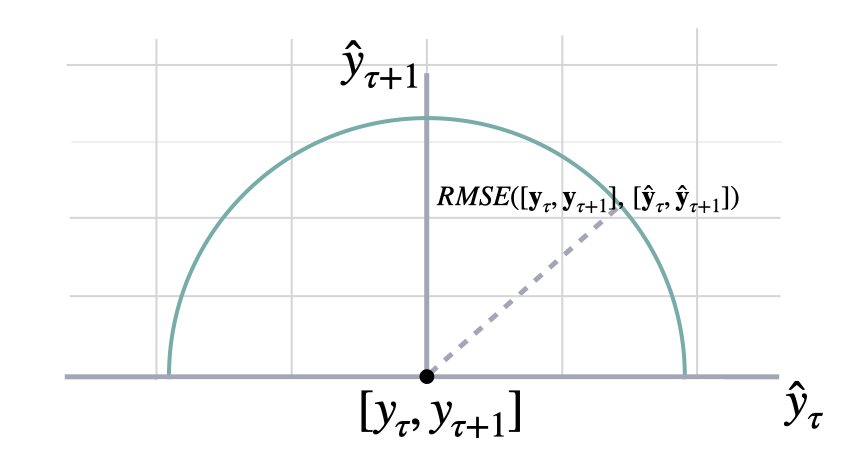

### Root Mean Squared Error

```math theme={null}

\mathrm{RMSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sqrt{\frac{1}{H} \sum^{t+H}_{\tau=t+1} (y_{\tau} - \hat{y}_{\tau})^{2}}

```

#### `mse`

```python theme={null}

mse(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Mean Squared Error (MSE)

MSE measures the relative prediction

accuracy of a forecasting method by calculating the

squared deviation of the prediction and the true

value at a given time, and averages these devations

over the length of the series.

### Root Mean Squared Error

```math theme={null}

\mathrm{RMSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sqrt{\frac{1}{H} \sum^{t+H}_{\tau=t+1} (y_{\tau} - \hat{y}_{\tau})^{2}}

```

#### `rmse`

```python theme={null}

rmse(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Root Mean Squared Error (RMSE)

RMSE measures the relative prediction

accuracy of a forecasting method by calculating the squared deviation

of the prediction and the observed value at a given time and

averages these devations over the length of the series.

Finally the RMSE will be in the same scale

as the original time series so its comparison with other

series is possible only if they share a common scale.

RMSE has a direct connection to the L2 norm.

### Bias

```math theme={null}

\mathrm{Bias}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} (\hat{y}_{\tau} - \mathbf{y}_{\tau})

```

#### `bias`

```python theme={null}

bias(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Forecast estimator bias.

Defined as prediction - actual

### Cumulative Forecast Error

```math theme={null}

\mathrm{CFE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sum^{t+H}_{\tau=t+1} (\hat{y}_{\tau} - \mathbf{y}_{\tau})

```

#### `cfe`

```python theme={null}

cfe(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Cumulative Forecast Error (CFE)

Total signed forecast error per series. Positive values mean under forecast; negative mean over forecast.

### Absolute Periods In Stock

```math theme={null}

\mathrm{PIS}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sum^{t+H}_{\tau=t+1} |y_{\tau} - \hat{y}_{\tau}|

```

#### `pis`

```python theme={null}

pis(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Compute the raw Absolute Periods In Stock (PIS) for one or multiple models.

The PIS metric sums the absolute forecast errors per series without any scaling,

yielding a scale-dependent measure of bias.

### Linex

```math theme={null}

\mathrm{Linex}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} (e^{a(y_{\tau} - \hat{y}_{\tau})} - a(y_{\tau} - \hat{y}_{\tau}) - 1)

```

where must be $a\neq0$.

#### `linex`

```python theme={null}

linex(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff', a=1.0)

```

Linex Loss (Linear Exponential)

The Linex loss penalizes over- and under-forecasting

asymmetrically depending on the parameter a.

* If a > 0, under-forecasting ($y > \hat{y}$) is penalized more.

* If a \< 0, over-forecasting ($\hat{y} > y$) is penalized more.

* a must not be 0.

**Parameters:**

| Name | Type | Description | Default |

| ---- | ---------------------------- | ------------------------------------------------------- | ---------------- |

| `a` |

#### `rmse`

```python theme={null}

rmse(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Root Mean Squared Error (RMSE)

RMSE measures the relative prediction

accuracy of a forecasting method by calculating the squared deviation

of the prediction and the observed value at a given time and

averages these devations over the length of the series.

Finally the RMSE will be in the same scale

as the original time series so its comparison with other

series is possible only if they share a common scale.

RMSE has a direct connection to the L2 norm.

### Bias

```math theme={null}

\mathrm{Bias}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} (\hat{y}_{\tau} - \mathbf{y}_{\tau})

```

#### `bias`

```python theme={null}

bias(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Forecast estimator bias.

Defined as prediction - actual

### Cumulative Forecast Error

```math theme={null}

\mathrm{CFE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sum^{t+H}_{\tau=t+1} (\hat{y}_{\tau} - \mathbf{y}_{\tau})

```

#### `cfe`

```python theme={null}

cfe(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Cumulative Forecast Error (CFE)

Total signed forecast error per series. Positive values mean under forecast; negative mean over forecast.

### Absolute Periods In Stock

```math theme={null}

\mathrm{PIS}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sum^{t+H}_{\tau=t+1} |y_{\tau} - \hat{y}_{\tau}|

```

#### `pis`

```python theme={null}

pis(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Compute the raw Absolute Periods In Stock (PIS) for one or multiple models.

The PIS metric sums the absolute forecast errors per series without any scaling,

yielding a scale-dependent measure of bias.

### Linex

```math theme={null}

\mathrm{Linex}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} (e^{a(y_{\tau} - \hat{y}_{\tau})} - a(y_{\tau} - \hat{y}_{\tau}) - 1)

```

where must be $a\neq0$.

#### `linex`

```python theme={null}

linex(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff', a=1.0)

```

Linex Loss (Linear Exponential)

The Linex loss penalizes over- and under-forecasting

asymmetrically depending on the parameter a.

* If a > 0, under-forecasting ($y > \hat{y}$) is penalized more.

* If a \< 0, over-forecasting ($\hat{y} > y$) is penalized more.

* a must not be 0.

**Parameters:**

| Name | Type | Description | Default |

| ---- | ---------------------------- | ------------------------------------------------------- | ---------------- |

| `a` | [float](#float) | Asymmetry parameter. Must be non-zero. Defaults to 1.0. | 1.0 |

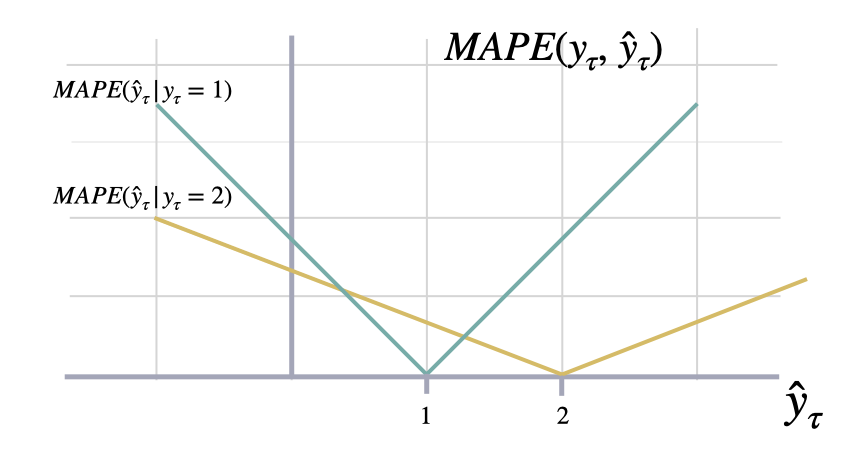

## 2. Percentage Errors

### Mean Absolute Percentage Error

```math theme={null}

\mathrm{MAPE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau}-\hat{y}_{\tau}|}{|y_{\tau}|}

```

#### `mape`

```python theme={null}

mape(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Mean Absolute Percentage Error (MAPE)

MAPE measures the relative prediction

accuracy of a forecasting method by calculating the percentual deviation

of the prediction and the observed value at a given time and

averages these devations over the length of the series.

The closer to zero an observed value is, the higher penalty MAPE loss

assigns to the corresponding error.

### Symmetric Mean Absolute Percentage Error

```math theme={null}

\mathrm{SMAPE}_{2}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau}-\hat{y}_{\tau}|}{|y_{\tau}|+|\hat{y}_{\tau}|}

```

#### `smape`

```python theme={null}

smape(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Symmetric Mean Absolute Percentage Error (SMAPE)

SMAPE measures the relative prediction

accuracy of a forecasting method by calculating the relative deviation

of the prediction and the observed value scaled by the sum of the

absolute values for the prediction and observed value at a

given time, then averages these devations over the length

of the series. This allows the SMAPE to have bounds between

0% and 100% which is desirable compared to normal MAPE that

may be undetermined when the target is zero.

## 3. Scale-independent Errors

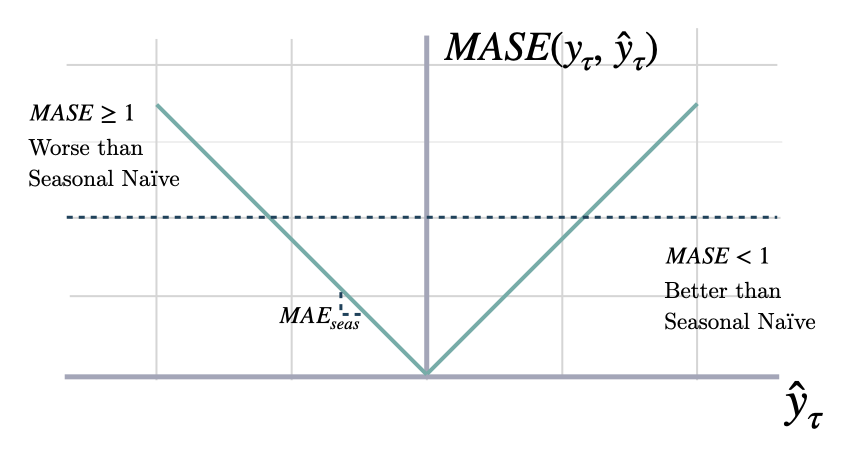

### Mean Absolute Scaled Error

```math theme={null}

\mathrm{MASE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau}) =

\frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau}-\hat{y}_{\tau}|}{\mathrm{MAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau})}

```

#### `mape`

```python theme={null}

mape(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Mean Absolute Percentage Error (MAPE)

MAPE measures the relative prediction

accuracy of a forecasting method by calculating the percentual deviation

of the prediction and the observed value at a given time and

averages these devations over the length of the series.

The closer to zero an observed value is, the higher penalty MAPE loss

assigns to the corresponding error.

### Symmetric Mean Absolute Percentage Error

```math theme={null}

\mathrm{SMAPE}_{2}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau}-\hat{y}_{\tau}|}{|y_{\tau}|+|\hat{y}_{\tau}|}

```

#### `smape`

```python theme={null}

smape(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Symmetric Mean Absolute Percentage Error (SMAPE)

SMAPE measures the relative prediction

accuracy of a forecasting method by calculating the relative deviation

of the prediction and the observed value scaled by the sum of the

absolute values for the prediction and observed value at a

given time, then averages these devations over the length

of the series. This allows the SMAPE to have bounds between

0% and 100% which is desirable compared to normal MAPE that

may be undetermined when the target is zero.

## 3. Scale-independent Errors

### Mean Absolute Scaled Error

```math theme={null}

\mathrm{MASE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau}) =

\frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau}-\hat{y}_{\tau}|}{\mathrm{MAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau})}

```

#### `mase`

```python theme={null}

mase(df, models, seasonality, train_df, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Mean Absolute Scaled Error (MASE)

MASE measures the relative prediction

accuracy of a forecasting method by comparinng the mean absolute errors

of the prediction and the observed value against the mean

absolute errors of the seasonal naive model.

The MASE partially composed the Overall Weighted Average (OWA),

used in the M4 Competition.

**Parameters:**

| Name | Type | Description | Default |

| ------------- | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` |

#### `mase`

```python theme={null}

mase(df, models, seasonality, train_df, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Mean Absolute Scaled Error (MASE)

MASE measures the relative prediction

accuracy of a forecasting method by comparinng the mean absolute errors

of the prediction and the observed value against the mean

absolute errors of the seasonal naive model.

The MASE partially composed the Overall Weighted Average (OWA),

used in the M4 Competition.

**Parameters:**

| Name | Type | Description | Default |

| ------------- | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `seasonality` | [int](#int) | Main frequency of the time series; Hourly 24, Daily 7, Weekly 52, Monthly 12, Quarterly 4, Yearly 1. | *required* |

| `train_df` | pandas or polars DataFrame | Training dataframe with id and actual values. Must be sorted by time. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://robjhyndman.com/papers/mase.pdf](https://robjhyndman.com/papers/mase.pdf)

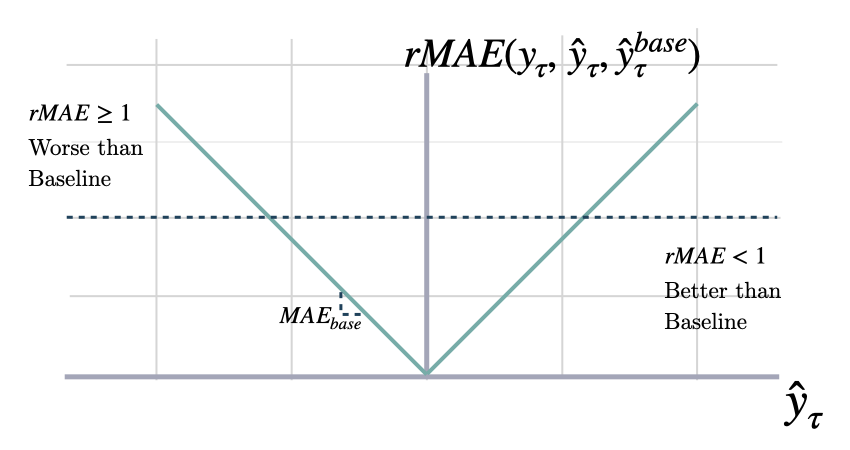

### Relative Mean Absolute Error

```math theme={null}

\mathrm{RMAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}, \mathbf{\hat{y}}^{base}_{\tau}) = \frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau}-\hat{y}_{\tau}|}{\mathrm{MAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{base}_{\tau})}

```

#### `rmae`

```python theme={null}

rmae(df, models, baseline, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Relative Mean Absolute Error (RMAE)

Calculates the RAME between two sets of forecasts (from two different forecasting methods).

A number smaller than one implies that the forecast in the

numerator is better than the forecast in the denominator.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` |

#### `rmae`

```python theme={null}

rmae(df, models, baseline, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Relative Mean Absolute Error (RMAE)

Calculates the RAME between two sets of forecasts (from two different forecasting methods).

A number smaller than one implies that the forecast in the

numerator is better than the forecast in the denominator.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `baseline` | [str](#str) | Column that identifies the baseline model predictions. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

### Normalized Deviation

```math theme={null}

\mathrm{ND}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \frac{\sum^{t+H}_{\tau=t+1} |y_{\tau} - \hat{y}_{\tau}|}{\sum^{t+H}_{\tau=t+1} | y_{\tau} |}

```

#### `nd`

```python theme={null}

nd(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Normalized Deviation (ND)

ND measures the relative prediction

accuracy of a forecasting method by calculating the

sum of the absolute deviation of the prediction and the true

value at a given time and dividing it by the sum of the absolute

value of the ground truth.

### Mean Squared Scaled Error

```math theme={null}

\mathrm{MSSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau}) =

\frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{(y_{\tau}-\hat{y}_{\tau})^2}{\mathrm{MSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau})}

```

### `msse`

```python theme={null}

msse(df, models, seasonality, train_df, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Mean Squared Scaled Error (MSSE)

MSSE measures the relative prediction

accuracy of a forecasting method by comparinng the mean squared errors

of the prediction and the observed value against the mean

squared errors of the seasonal naive model.

**Parameters:**

| Name | Type | Description | Default |

| ------------- | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `seasonality` | [int](#int) | Main frequency of the time series; Hourly 24, Daily 7, Weekly 52, Monthly 12, Quarterly 4, Yearly 1. | *required* |

| `train_df` | pandas or polars DataFrame | Training dataframe with id and actual values. Must be sorted by time. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://otexts.com/fpp3/accuracy.html](https://otexts.com/fpp3/accuracy.html)

### Root Mean Squared Scaled Error

```math theme={null}

\mathrm{RMSSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau}) =

\sqrt{\frac{1}{H} \sum^{t+H}_{\tau=t+1} \frac{(y_{\tau}-\hat{y}_{\tau})^2}{\mathrm{MSE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau})}}

```

### `rmsse`

```python theme={null}

rmsse(df, models, seasonality, train_df, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Root Mean Squared Scaled Error (RMSSE)

MSSE measures the relative prediction

accuracy of a forecasting method by comparinng the mean squared errors

of the prediction and the observed value against the mean

squared errors of the seasonal naive model.

**Parameters:**

| Name | Type | Description | Default |

| ------------- | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ---------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `seasonality` | int | Main frequency of the time series; Hourly 24, Daily 7, Weekly 52, Monthly 12, Quarterly 4, Yearly 1. | *required* |

| `train_df` | pandas or polars DataFrame | Training dataframe with id and actual values. Must be sorted by time. | *required* |

| `id_col` | str | Column that identifies each serie. Defaults to 'unique\_id'. | *required* |

| `target_col` | str | Column that contains the target. Defaults to 'y'. | *required* |

| `cutoff_col` | str | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | *required* |

**Returns:**

| Type | Description |

| ----------------------------------------------------------------------------------- | ----------- |

| pandas or polars DataFrame: dataframe with one row per id and one column per model. | |

References

\[1] [https://otexts.com/fpp3/accuracy.html](https://otexts.com/fpp3/accuracy.html)

### Scaled Absolute Periods In Stock

```math theme={null}

\mathrm{PIS}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}_{\tau}) = \sum^{t+H}_{\tau=t+1} \frac{|y_{\tau} - \hat{y}_{\tau}|}{\bar{y}}

```

where $\bar{y}=\frac{1}{H}\sum^{t+H}_{\tau=t+1} y_{\tau}$.

#### `spis`

```python theme={null}

spis(df, models, train_df, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Compute the scaled Absolute Periods In Stock (sAPIS) for one or multiple models.

The sPIS metric scales the sum of absolute forecast errors by the mean in-sample demand,

yielding a scale-independent bias measure that can be aggregated across series.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `train_df` | pandas or polars DataFrame | Training dataframe with id and actual values. Must be sorted by time. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

## 4. Probabilistic Errors

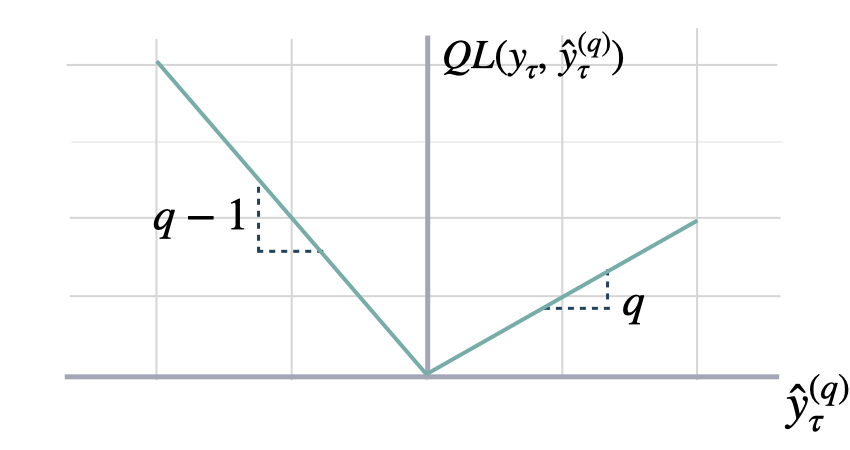

### Quantile Loss

```math theme={null}

\mathrm{QL}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{(q)}_{\tau}) =

\frac{1}{H} \sum^{t+H}_{\tau=t+1}

\Big( (1-q)\,( \hat{y}^{(q)}_{\tau} - y_{\tau} )_{+}

+ q\,( y_{\tau} - \hat{y}^{(q)}_{\tau} )_{+} \Big)

```

#### `quantile_loss`

```python theme={null}

quantile_loss(df, models, q=0.5, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Quantile Loss (QL)

QL measures the deviation of a quantile forecast.

By weighting the absolute deviation in a non symmetric way, the

loss pays more attention to under or over estimation.

A common value for q is 0.5 for the deviation from the median.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` |

#### `quantile_loss`

```python theme={null}

quantile_loss(df, models, q=0.5, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Quantile Loss (QL)

QL measures the deviation of a quantile forecast.

By weighting the absolute deviation in a non symmetric way, the

loss pays more attention to under or over estimation.

A common value for q is 0.5 for the deviation from the median.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | dict from str to str | Mapping from model name to the model predictions for the specified quantile. | *required* |

| `q` | [float](#float) | Quantile for the predictions' comparison. Defaults to 0.5. | 0.5 |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

### Scaled Quantile Loss

```math theme={null}

\mathrm{SQL}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{(q)}_{\tau}) =

\frac{1}{H} \sum^{t+H}_{\tau=t+1}

\frac{(1-q)\,( \hat{y}^{(q)}_{\tau} - y_{\tau} )_{+}

+ q\,( y_{\tau} - \hat{y}^{(q)}_{\tau} )_{+}}{\mathrm{MAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau})}

```

#### `scaled_quantile_loss`

```python theme={null}

scaled_quantile_loss(df, models, seasonality, train_df, q=0.5, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Scaled Quantile Loss (SQL)

SQL measures the deviation of a quantile forecast scaled by

the mean absolute errors of the seasonal naive model.

By weighting the absolute deviation in a non symmetric way, the

loss pays more attention to under or over estimation.

A common value for q is 0.5 for the deviation from the median.

This was the official measure used in the M5 Uncertainty competition

with seasonality = 1.

**Parameters:**

| Name | Type | Description | Default |

| ------------- | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | dict from str to str | Mapping from model name to the model predictions for the specified quantile. | *required* |

| `seasonality` | [int](#int) | Main frequency of the time series; Hourly 24, Daily 7, Weekly 52, Monthly 12, Quarterly 4, Yearly 1. | *required* |

| `train_df` | pandas or polars DataFrame | Training dataframe with id and actual values. Must be sorted by time. | *required* |

| `q` | [float](#float) | Quantile for the predictions' comparison. Defaults to 0.5. | 0.5 |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://www.sciencedirect.com/science/article/pii/S0169207021001722](https://www.sciencedirect.com/science/article/pii/S0169207021001722)

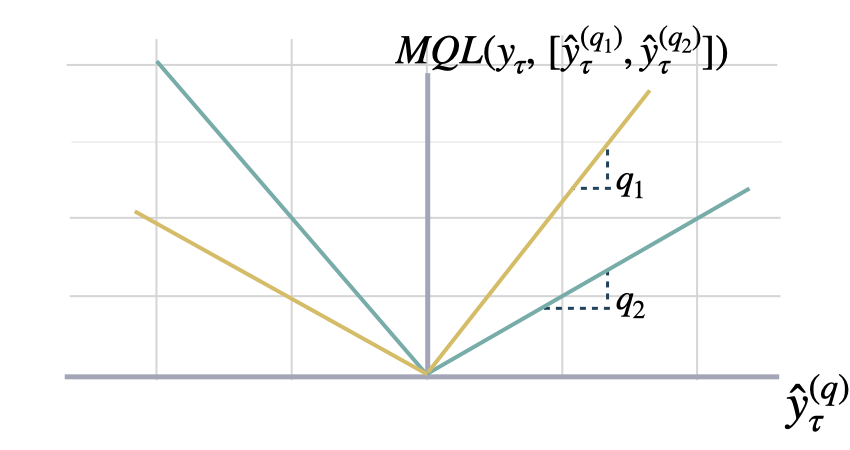

### Multi-Quantile Loss

```math theme={null}

\mathrm{MQL}(\mathbf{y}_{\tau},

[\mathbf{\hat{y}}^{(q_{1})}_{\tau}, ... ,\hat{y}^{(q_{n})}_{\tau}]) =

\frac{1}{n} \sum_{q_{i}} \mathrm{QL}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{(q_{i})}_{\tau})

```

#### `mqloss`

```python theme={null}

mqloss(df, models, quantiles, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Multi-Quantile loss (MQL)

MQL calculates the average multi-quantile Loss for

a given set of quantiles, based on the absolute

difference between predicted quantiles and observed values.

The limit behavior of MQL allows to measure the accuracy

of a full predictive distribution with

the continuous ranked probability score (CRPS). This can be achieved

through a numerical integration technique, that discretizes the quantiles

and treats the CRPS integral with a left Riemann approximation, averaging over

uniformly distanced quantiles.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | ----------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` |

#### `mqloss`

```python theme={null}

mqloss(df, models, quantiles, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Multi-Quantile loss (MQL)

MQL calculates the average multi-quantile Loss for

a given set of quantiles, based on the absolute

difference between predicted quantiles and observed values.

The limit behavior of MQL allows to measure the accuracy

of a full predictive distribution with

the continuous ranked probability score (CRPS). This can be achieved

through a numerical integration technique, that discretizes the quantiles

and treats the CRPS integral with a left Riemann approximation, averaging over

uniformly distanced quantiles.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | ----------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | dict from str to list of str | Mapping from model name to the model predictions for each quantile. | *required* |

| `quantiles` | numpy array | Quantiles to compare against. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://www.jstor.org/stable/2629907](https://www.jstor.org/stable/2629907)

### Scaled Multi-Quantile Loss

```math theme={null}

\mathrm{MQL}(\mathbf{y}_{\tau},

[\mathbf{\hat{y}}^{(q_{1})}_{\tau}, ... ,\hat{y}^{(q_{n})}_{\tau}]) =

\frac{1}{n} \sum_{q_{i}} \frac{\mathrm{QL}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{(q_{i})}_{\tau})}{\mathrm{MAE}(\mathbf{y}_{\tau}, \mathbf{\hat{y}}^{season}_{\tau})}

```

#### `scaled_mqloss`

```python theme={null}

scaled_mqloss(df, models, quantiles, seasonality, train_df, id_col='unique_id', target_col='y', cutoff_col='cutoff', time_col='ds')

```

Scaled Multi-Quantile loss (SMQL)

SMQL calculates the average multi-quantile Loss for

a given set of quantiles, based on the absolute

difference between predicted quantiles and observed values

scaled by the mean absolute errors of the seasonal naive model.

The limit behavior of MQL allows to measure the accuracy

of a full predictive distribution with

the continuous ranked probability score (CRPS). This can be achieved

through a numerical integration technique, that discretizes the quantiles

and treats the CRPS integral with a left Riemann approximation, averaging over

uniformly distanced quantiles.

This was the official measure used in the M5 Uncertainty competition

with seasonality = 1.

**Parameters:**

| Name | Type | Description | Default |

| ------------- | ----------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | dict from str to list of str | Mapping from model name to the model predictions for each quantile. | *required* |

| `quantiles` | numpy array | Quantiles to compare against. | *required* |

| `seasonality` | [int](#int) | Main frequency of the time series; Hourly 24, Daily 7, Weekly 52, Monthly 12, Quarterly 4, Yearly 1. | *required* |

| `train_df` | pandas or polars DataFrame | Training dataframe with id and actual values. Must be sorted by time. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://www.sciencedirect.com/science/article/pii/S0169207021001722](https://www.sciencedirect.com/science/article/pii/S0169207021001722)

### Coverage

#### `coverage`

```python theme={null}

coverage(df, models, level, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Coverage of y with y\_hat\_lo and y\_hat\_hi.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `level` | [int](#int) | Confidence level used for intervals. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://www.jstor.org/stable/2629907](https://www.jstor.org/stable/2629907)

### Calibration

#### `calibration`

```python theme={null}

calibration(df, models, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Fraction of y that is lower than the model's predictions.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | dict from str to str | Mapping from model name to the model predictions. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://www.jstor.org/stable/2629907](https://www.jstor.org/stable/2629907)

### CRPS

```math theme={null}

\mathrm{sCRPS}(\hat{F}_{\tau}, \mathbf{y}_{\tau}) = \frac{2}{N} \sum_{i}

\int^{1}_{0} \frac{\mathrm{QL}(\hat{F}_{i,\tau}, y_{i,\tau})_{q}}{\sum_{i} | y_{i,\tau} |} dq

```

Where $\hat{F}_{\tau}$ is the an estimated multivariate distribution,

and $y_{i,\tau}$ are its realizations.

#### `scaled_crps`

```python theme={null}

scaled_crps(df, models, quantiles, id_col='unique_id', target_col='y', cutoff_col='cutoff')

```

Scaled Continues Ranked Probability Score

Calculates a scaled variation of the CRPS, as proposed by Rangapuram (2021),

to measure the accuracy of predicted quantiles `y_hat` compared to the observation `y`.

This metric averages percentual weighted absolute deviations as

defined by the quantile losses.

**Parameters:**

| Name | Type | Description | Default |

| ------------ | ----------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, times, actuals and predictions. | *required* |

| `models` | dict from str to list of str | Mapping from model name to the model predictions for each quantile. | *required* |

| `quantiles` | numpy array | Quantiles to compare against. | *required* |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ----------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: dataframe with one row per id and one column per model. |

References

\[1] [https://proceedings.mlr.press/v139/rangapuram21a.html](https://proceedings.mlr.press/v139/rangapuram21a.html)

### Tweedie Deviance

For a set of forecasts $\{\mu_i\}_{i=1}^N$ and observations

$\{y_i\}_{i=1}^N$, the mean Tweedie deviance with power $p$ is

```math theme={null}

\mathrm{TD}_{p}(\boldsymbol{\mu}, \mathbf{y})

= \frac{1}{N} \sum_{i=1}^{N} d_{p}(y_i, \mu_i)

```

where the unit-scaled deviance for each pair $(y,\mu)$ is

```math theme={null}

d_{p}(y,\mu)

=

2

\begin{cases}

\displaystyle

\frac{y^{2-p}}{(1-p)(2-p)}

\;-\;

\frac{y\,\mu^{1-p}}{1-p}

\;+\;

\frac{\mu^{2-p}}{2-p},

& p \notin\{1,2\},\\[1em]

\displaystyle

y\,\ln\!\frac{y}{\mu}\;-\;(y-\mu),

& p = 1\quad(\text{Poisson deviance}),\\[0.5em]

\displaystyle

-2\Bigl[\ln\!\frac{y}{\mu}\;-\;\frac{y-\mu}{\mu}\Bigr],

& p = 2\quad(\text{Gamma deviance}).

\end{cases}

```

* $y_i$ are the true values, $\mu_i$ the predicted means.

* $p$ controls the variance relationship

$\mathrm{Var}(Y)\propto\mu^{p}$.

* When $1 2: Inverse Gaussian

**Parameters:**

| Name | Type | Description | Default |

| ------------ | --------------------------------------- | ------------------------------------------------------------------------------------------------------ | ------------------------- |

| `df` | pandas or polars DataFrame | Input dataframe with id, actuals and predictions. | *required* |

| `models` | list of str | Columns that identify the models predictions. | *required* |

| `power` | [float](#float) | Tweedie power parameter. Determines the compound distribution. Defaults to 1.5. | 1.5 |

| `id_col` | [str](#str) | Column that identifies each serie. Defaults to 'unique\_id'. | 'unique\_id' |

| `target_col` | [str](#str) | Column that contains the target. Defaults to 'y'. | 'y' |

| `cutoff_col` | [str](#str) | Column that identifies the cutoff point for each forecast cross-validation fold. Defaults to 'cutoff'. | 'cutoff' |

**Returns:**

| Type | Description |

| ------------------------------------------------------------------------ | ------------------------------------------------------------------------------------------------------------------------- |

| [IntoDataFrameT](#narwhals.stable.v2.typing.IntoDataFrameT) | pandas or polars DataFrame: DataFrame with one row per id and one column per model, containing the mean Tweedie deviance. |

References

\[1] [https://en.wikipedia.org/wiki/Tweedie\_distribution](https://en.wikipedia.org/wiki/Tweedie_distribution)