> ## Documentation Index

> Fetch the complete documentation index at: https://nixtlaverse.nixtla.io/llms.txt

> Use this file to discover all available pages before exploring further.

# Simulation Paths | NeuralForecast

> Generate correlated sample paths for scenario analysis

## Simulation vs. Prediction Intervals: When to Use Which

NeuralForecast provides two complementary approaches for reasoning about

future uncertainty:

### Prediction Intervals (`predict(level=...)`)

Prediction intervals answer: **“What range of values is the target

likely to fall within at each future time step?”**

* Output: Independent confidence bands per horizon step (e.g., 90%

interval at step $h$).

* Each step is treated marginally — no information about how steps

relate to each other.

* Best for: monitoring, alerting, dashboarding, reporting confidence

bands.

### Simulation Paths (`simulate(...)`)

Simulation paths answer: **“What are realistic *joint* future

trajectories the time series could follow?”**

* Output: $N$ complete trajectories of length $H$, each representing a

plausible future.

* Temporal correlations between steps are preserved — if step $h$ is

high, step $h+1$ is likely high too.

* Best for: scenario analysis, portfolio optimization, supply chain

planning, energy dispatch, risk assessment (VaR/CVaR), stochastic

programming.

### Key Difference: Marginal vs. Joint

Consider electricity price forecasting over 24 hours. A 90% prediction

interval tells you the price at hour 12 will likely be between \$40 and

\$80. But it says nothing about whether hours 11, 12, and 13 will *all*

be high simultaneously (a sustained price spike) or whether high and low

values alternate randomly.

Simulation paths capture this joint structure. From 500 simulated paths

you can compute: - **P(total cost > budget)** — requires summing across

correlated hours - **P(at least 3 consecutive hours above \$70)** —

requires temporal ordering - **Expected shortfall (CVaR)** — requires

the joint tail distribution

These questions *cannot* be answered from marginal prediction intervals

alone.

## Available Simulation Methods

| Method | Temporal Correlation | Description |

| --------------------------- | -------------------------------- | ------------------------------------------------------------------------------------------------------------------------------------------------------------ |

| `gaussian_copula` (default) | AR(1) Gaussian copula | Draws correlated uniform samples via Cholesky decomposition, maps through marginal CDFs. Parametric correlation structure. |

| `schaake_shuffle` | Empirical (historical templates) | Draws independent marginal samples, reorders them to match rank structure of historical trajectory templates. Nonparametric — captures arbitrary dependence. |

**Compatible losses**: - **`DistributionLoss`** (Normal, StudentT,

Poisson, etc.) and **mixture losses** (`GMM`, `PMM`, `NBMM`) — produce

arbitrary quantiles natively. - **`MQLoss`** / **`HuberMQLoss`** — uses

the model’s trained quantile grid. - **`IQLoss`** / **`HuberIQLoss`** —

evaluates multiple quantiles via repeated forward passes. - **Point

losses** (`MAE`, `MSE`, etc.) — requires `prediction_intervals`

(Conformal Prediction) set during `fit()` to build a quantile grid from

calibration scores.

## 1. Setup

```python theme={null}

import logging

import warnings

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import torch

warnings.filterwarnings("ignore")

logging.getLogger("pytorch_lightning").setLevel(logging.ERROR)

torch.set_float32_matmul_precision("high")

```

## 2. Load Data

We use the AirPassengers dataset — a classic monthly time series of

airline passenger counts.

```python theme={null}

from neuralforecast.utils import AirPassengersDF

Y_df = AirPassengersDF.copy()

Y_train_df = Y_df[Y_df.ds <= "1959-12-31"] # 132 months train

Y_test_df = Y_df[Y_df.ds > "1959-12-31"] # 12 months test

print(f"Train: {len(Y_train_df)} rows, Test: {len(Y_test_df)} rows")

Y_train_df.tail()

```

```text theme={null}

2026-03-20 13:09:32,071 INFO util.py:154 -- Missing packages: ['ipywidgets']. Run `pip install -U ipywidgets`, then restart the notebook server for rich notebook output.

2026-03-20 13:09:32,151 INFO util.py:154 -- Missing packages: ['ipywidgets']. Run `pip install -U ipywidgets`, then restart the notebook server for rich notebook output.

```

```text theme={null}

Train: 132 rows, Test: 12 rows

```

| | unique\_id | ds | y |

| --- | ---------- | ---------- | ----- |

| 127 | 1.0 | 1959-08-31 | 559.0 |

| 128 | 1.0 | 1959-09-30 | 463.0 |

| 129 | 1.0 | 1959-10-31 | 407.0 |

| 130 | 1.0 | 1959-11-30 | 362.0 |

| 131 | 1.0 | 1959-12-31 | 405.0 |

## 3. Train Models

We train five models showcasing different loss types: - **NHITS + GMM**

— Gaussian Mixture Model, a mixture `DistributionLoss`. - **NHITS +

DistributionLoss(Normal)** — parametric distribution output. - **NHITS +

MQLoss** — Multi-Quantile Loss, directly optimizes quantile levels. -

**NHITS + IQLoss** — Implicit Quantile Loss, can evaluate any quantile

at inference. - **NHITS + MAE** with Conformal Prediction — point-loss

model with calibrated prediction intervals.

Since the MAE model needs conformal prediction intervals, we pass

`prediction_intervals` to `fit()`.

```python theme={null}

from neuralforecast import NeuralForecast

from neuralforecast.losses.pytorch import GMM, MAE, MQLoss, DistributionLoss, IQLoss

from neuralforecast.models import NHITS

from neuralforecast.utils import PredictionIntervals

H = 12

MAX_STEPS = 100

models = [

NHITS(h=H, input_size=36, max_steps=MAX_STEPS, loss=GMM(), alias="NHITS_GMM", scaler_type="robust"),

NHITS(h=H, input_size=36, max_steps=MAX_STEPS, loss=DistributionLoss(distribution="Normal"), alias="NHITS_Normal", scaler_type="robust"),

NHITS(h=H, input_size=36, max_steps=MAX_STEPS, loss=MQLoss(level=[80, 90]), alias="NHITS_MQ", scaler_type="robust"),

NHITS(h=H, input_size=36, max_steps=MAX_STEPS, loss=IQLoss(), alias="NHITS_IQL", scaler_type="robust"),

NHITS(h=H, input_size=36, max_steps=MAX_STEPS, loss=MAE(), alias="NHITS_MAE", scaler_type="robust"),

]

nf = NeuralForecast(models=models, freq="MS")

nf.fit(

df=Y_train_df,

prediction_intervals=PredictionIntervals(n_windows=2, method="conformal_error"),

)

```

## 4. Prediction Intervals (Baseline)

First, let’s see the standard prediction intervals — these are marginal

(per-step) uncertainty bands.

```python theme={null}

from utilsforecast.plotting import plot_series

fcst_df = nf.predict(level=[80, 90])

```

```python theme={null}

plot_series(Y_train_df, fcst_df, level=[80, 90], models=["NHITS_Normal"])

```

The shaded bands show the 80% and 90% prediction intervals. These are

useful for understanding per-step uncertainty, but they do not capture

the **temporal correlation** between forecast steps. Each band is

computed independently.

## 5. Simulation Paths

Now let’s generate correlated simulation paths using the `simulate()`

method. This returns a long-format DataFrame with columns

`[unique_id, ds, sample_id, model_1, model_2, ...]`.

### Plotting helper

```python theme={null}

def extract_sims(sim_df, model_col, uid=None):

"""Extract simulation paths as a (n_paths, H) numpy array from simulate() output."""

if uid is None:

uid = sim_df["unique_id"].iloc[0]

series = sim_df[sim_df["unique_id"] == uid]

return series.pivot(index="sample_id", columns="ds", values=model_col).values

def plot_simulations(train_df, sims, model_name, title, color="steelblue", n_show=100):

"""Plot historical data with simulated future paths and derived prediction intervals."""

fig, ax = plt.subplots(1, 1, figsize=(10, 4))

# History (last 48 months)

hist = train_df.sort_values("ds").tail(48)

ax.plot(hist["ds"], hist["y"], color="black", linewidth=1.5, label="History")

# Future dates

last_date = hist["ds"].iloc[-1]

future_dates = pd.date_range(start=last_date, periods=sims.shape[1] + 1, freq="MS")[1:]

# Individual paths

for i in range(min(n_show, sims.shape[0])):

ax.plot(future_dates, sims[i], color=color, alpha=0.05, linewidth=0.5)

# Derived prediction intervals from simulations

for q_lo, q_hi, alpha in [(0.05, 0.95, 0.15), (0.10, 0.90, 0.25), (0.25, 0.75, 0.35)]:

lo = np.quantile(sims, q_lo, axis=0)

hi = np.quantile(sims, q_hi, axis=0)

ax.fill_between(future_dates, lo, hi, color=color, alpha=alpha,

label=f"{int((q_hi - q_lo) * 100)}% PI")

# Median

median = np.median(sims, axis=0)

ax.plot(future_dates, median, color=color, linewidth=2, label="Median")

# Actual (if available)

ax.plot(Y_test_df["ds"], Y_test_df["y"], color="black", linestyle="--", label="Actual")

ax.set_title(f"{title} — {model_name}")

ax.legend(loc="upper left", fontsize=8)

ax.set_xlabel("Date")

ax.set_ylabel("Passengers")

plt.tight_layout()

plt.show()

```

### Generate simulation paths

`simulate()` generates `n_paths` correlated sample paths for every model

× series combination.

```python theme={null}

N_PATHS = 500

SEED = 42

sim_df = nf.simulate(n_paths=N_PATHS, seed=SEED)

```

```python theme={null}

sim_df.head(10)

```

| | unique\_id | ds | sample\_id | NHITS\_GMM | NHITS\_Normal | NHITS\_MQ | NHITS\_IQL | NHITS\_MAE |

| - | ---------- | ---------- | ---------- | ---------- | ------------- | ---------- | ---------- | ---------- |

| 0 | 1.0 | 1960-01-01 | 0 | 424.577554 | 424.765725 | 415.206802 | 409.314326 | 438.886536 |

| 1 | 1.0 | 1960-02-01 | 0 | 404.827416 | 404.260575 | 414.203812 | 388.755778 | 416.497602 |

| 2 | 1.0 | 1960-03-01 | 0 | 469.169496 | 469.978479 | 464.367880 | 466.584470 | 482.319912 |

| 3 | 1.0 | 1960-04-01 | 0 | 450.245044 | 451.145088 | 454.416200 | 462.261074 | 459.493987 |

| 4 | 1.0 | 1960-05-01 | 0 | 472.641135 | 471.130120 | 475.350769 | 486.486899 | 493.030374 |

| 5 | 1.0 | 1960-06-01 | 0 | 528.117486 | 527.280406 | 539.266724 | 497.874372 | 530.030655 |

| 6 | 1.0 | 1960-07-01 | 0 | 594.137207 | 592.315796 | 623.242188 | 507.372412 | 586.462607 |

| 7 | 1.0 | 1960-08-01 | 0 | 604.532895 | 604.907234 | 617.977478 | 531.723887 | 583.457802 |

| 8 | 1.0 | 1960-09-01 | 0 | 530.447128 | 529.882652 | 545.858492 | 566.198389 | 524.067964 |

| 9 | 1.0 | 1960-10-01 | 0 | 458.686895 | 458.105852 | 466.378017 | 466.831645 | 468.689723 |

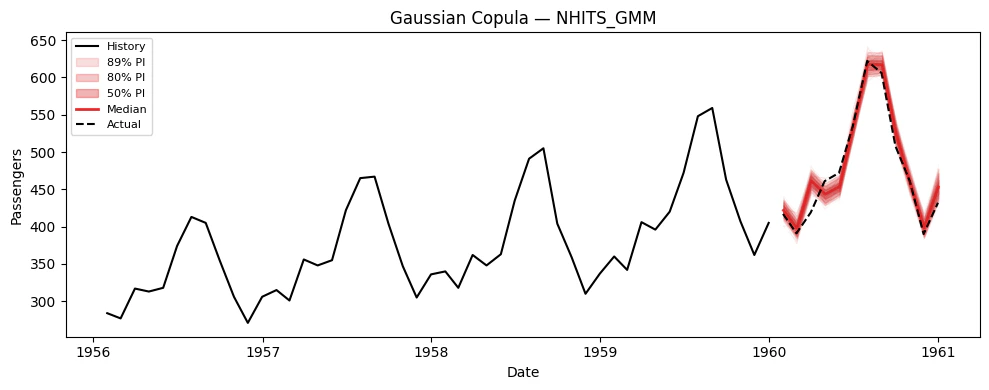

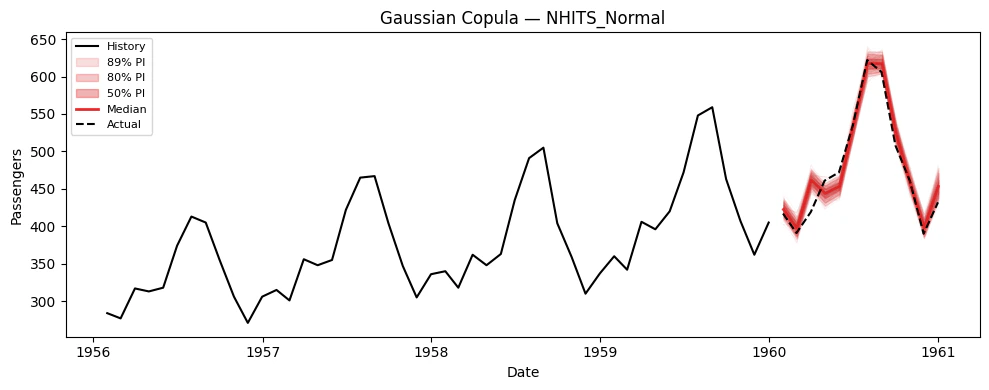

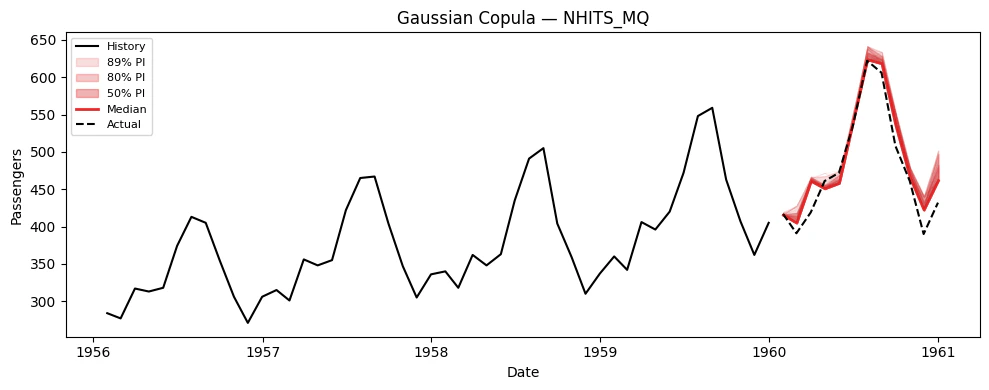

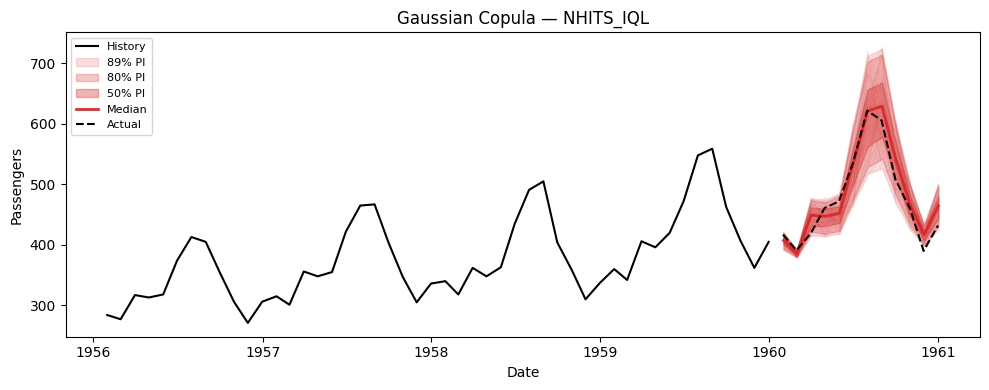

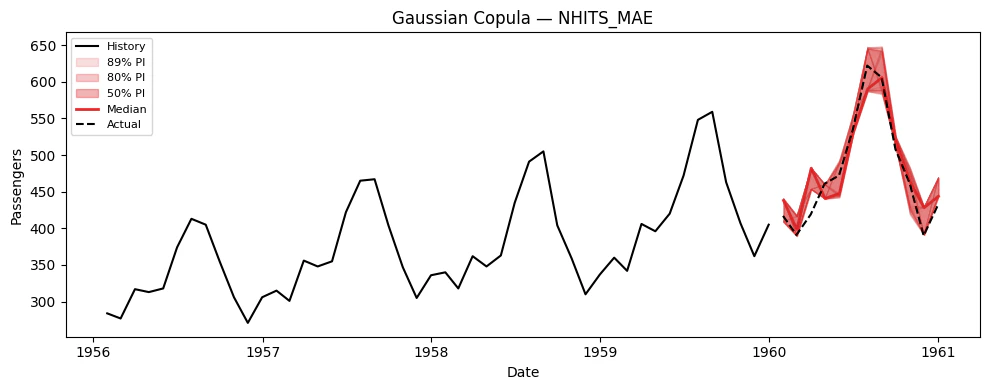

### Visualize paths for each model

```python theme={null}

# Extract (n_paths, H) arrays for plotting

model_cols = [c for c in sim_df.columns if c not in ("unique_id", "ds", "sample_id")]

for model_col in model_cols:

sims = extract_sims(sim_df, model_col)

print(f"{model_col}: simulation paths shape = {sims.shape}")

plot_simulations(Y_train_df, sims, model_col, "Gaussian Copula", color="tab:red")

```

```text theme={null}

NHITS_GMM: simulation paths shape = (500, 12)

NHITS_Normal: simulation paths shape = (500, 12)

NHITS_MQ: simulation paths shape = (500, 12)

NHITS_IQL: simulation paths shape = (500, 12)

NHITS_MAE: simulation paths shape = (500, 12)

```

The shaded bands show the 80% and 90% prediction intervals. These are

useful for understanding per-step uncertainty, but they do not capture

the **temporal correlation** between forecast steps. Each band is

computed independently.

## 5. Simulation Paths

Now let’s generate correlated simulation paths using the `simulate()`

method. This returns a long-format DataFrame with columns

`[unique_id, ds, sample_id, model_1, model_2, ...]`.

### Plotting helper

```python theme={null}

def extract_sims(sim_df, model_col, uid=None):

"""Extract simulation paths as a (n_paths, H) numpy array from simulate() output."""

if uid is None:

uid = sim_df["unique_id"].iloc[0]

series = sim_df[sim_df["unique_id"] == uid]

return series.pivot(index="sample_id", columns="ds", values=model_col).values

def plot_simulations(train_df, sims, model_name, title, color="steelblue", n_show=100):

"""Plot historical data with simulated future paths and derived prediction intervals."""

fig, ax = plt.subplots(1, 1, figsize=(10, 4))

# History (last 48 months)

hist = train_df.sort_values("ds").tail(48)

ax.plot(hist["ds"], hist["y"], color="black", linewidth=1.5, label="History")

# Future dates

last_date = hist["ds"].iloc[-1]

future_dates = pd.date_range(start=last_date, periods=sims.shape[1] + 1, freq="MS")[1:]

# Individual paths

for i in range(min(n_show, sims.shape[0])):

ax.plot(future_dates, sims[i], color=color, alpha=0.05, linewidth=0.5)

# Derived prediction intervals from simulations

for q_lo, q_hi, alpha in [(0.05, 0.95, 0.15), (0.10, 0.90, 0.25), (0.25, 0.75, 0.35)]:

lo = np.quantile(sims, q_lo, axis=0)

hi = np.quantile(sims, q_hi, axis=0)

ax.fill_between(future_dates, lo, hi, color=color, alpha=alpha,

label=f"{int((q_hi - q_lo) * 100)}% PI")

# Median

median = np.median(sims, axis=0)

ax.plot(future_dates, median, color=color, linewidth=2, label="Median")

# Actual (if available)

ax.plot(Y_test_df["ds"], Y_test_df["y"], color="black", linestyle="--", label="Actual")

ax.set_title(f"{title} — {model_name}")

ax.legend(loc="upper left", fontsize=8)

ax.set_xlabel("Date")

ax.set_ylabel("Passengers")

plt.tight_layout()

plt.show()

```

### Generate simulation paths

`simulate()` generates `n_paths` correlated sample paths for every model

× series combination.

```python theme={null}

N_PATHS = 500

SEED = 42

sim_df = nf.simulate(n_paths=N_PATHS, seed=SEED)

```

```python theme={null}

sim_df.head(10)

```

| | unique\_id | ds | sample\_id | NHITS\_GMM | NHITS\_Normal | NHITS\_MQ | NHITS\_IQL | NHITS\_MAE |

| - | ---------- | ---------- | ---------- | ---------- | ------------- | ---------- | ---------- | ---------- |

| 0 | 1.0 | 1960-01-01 | 0 | 424.577554 | 424.765725 | 415.206802 | 409.314326 | 438.886536 |

| 1 | 1.0 | 1960-02-01 | 0 | 404.827416 | 404.260575 | 414.203812 | 388.755778 | 416.497602 |

| 2 | 1.0 | 1960-03-01 | 0 | 469.169496 | 469.978479 | 464.367880 | 466.584470 | 482.319912 |

| 3 | 1.0 | 1960-04-01 | 0 | 450.245044 | 451.145088 | 454.416200 | 462.261074 | 459.493987 |

| 4 | 1.0 | 1960-05-01 | 0 | 472.641135 | 471.130120 | 475.350769 | 486.486899 | 493.030374 |

| 5 | 1.0 | 1960-06-01 | 0 | 528.117486 | 527.280406 | 539.266724 | 497.874372 | 530.030655 |

| 6 | 1.0 | 1960-07-01 | 0 | 594.137207 | 592.315796 | 623.242188 | 507.372412 | 586.462607 |

| 7 | 1.0 | 1960-08-01 | 0 | 604.532895 | 604.907234 | 617.977478 | 531.723887 | 583.457802 |

| 8 | 1.0 | 1960-09-01 | 0 | 530.447128 | 529.882652 | 545.858492 | 566.198389 | 524.067964 |

| 9 | 1.0 | 1960-10-01 | 0 | 458.686895 | 458.105852 | 466.378017 | 466.831645 | 468.689723 |

### Visualize paths for each model

```python theme={null}

# Extract (n_paths, H) arrays for plotting

model_cols = [c for c in sim_df.columns if c not in ("unique_id", "ds", "sample_id")]

for model_col in model_cols:

sims = extract_sims(sim_df, model_col)

print(f"{model_col}: simulation paths shape = {sims.shape}")

plot_simulations(Y_train_df, sims, model_col, "Gaussian Copula", color="tab:red")

```

```text theme={null}

NHITS_GMM: simulation paths shape = (500, 12)

NHITS_Normal: simulation paths shape = (500, 12)

NHITS_MQ: simulation paths shape = (500, 12)

NHITS_IQL: simulation paths shape = (500, 12)

NHITS_MAE: simulation paths shape = (500, 12)

```

## 6. Using Simulation Paths for Decision-Making

The key advantage of simulation paths over prediction intervals is

answering **joint** probabilistic questions. Here are concrete examples.

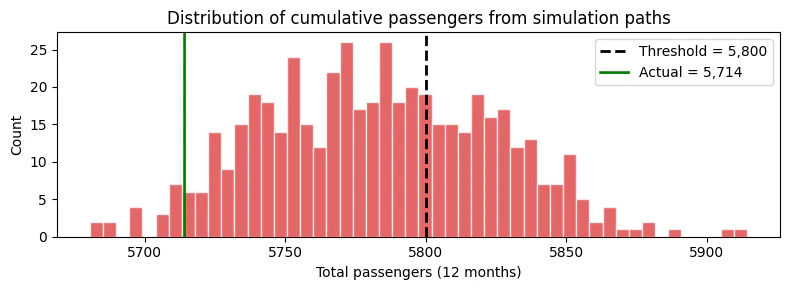

### Example: Probability of exceeding a cumulative threshold

Suppose we have a capacity of 5,800 total passengers over the next 12

months. What is the probability of exceeding this capacity?

This question requires the **joint** distribution — it cannot be

answered from marginal intervals.

```python theme={null}

THRESHOLD = 5800

# Use NHITS_GMM simulations

sims_gmm = extract_sims(sim_df, "NHITS_GMM")

cumulative_passengers = sims_gmm.sum(axis=1) # Sum across H=12 months per path

prob_exceed = (cumulative_passengers > THRESHOLD).mean()

print(f"P(total passengers > {THRESHOLD:,}) = {prob_exceed:.1%}")

print(f"Expected total passengers = {cumulative_passengers.mean():,.0f}")

print(f"5th percentile = {np.quantile(cumulative_passengers, 0.05):,.0f}")

print(f"95th percentile = {np.quantile(cumulative_passengers, 0.95):,.0f}")

fig, ax = plt.subplots(figsize=(8, 3))

ax.hist(cumulative_passengers, bins=50, color="tab:red", alpha=0.7, edgecolor="white")

ax.axvline(THRESHOLD, color="black", linestyle="--", linewidth=2, label=f"Threshold = {THRESHOLD:,}")

ax.axvline(Y_test_df["y"].sum(), color="green", linestyle="-", linewidth=2, label=f"Actual = {Y_test_df['y'].sum():,.0f}")

ax.set_xlabel("Total passengers (12 months)")

ax.set_ylabel("Count")

ax.set_title("Distribution of cumulative passengers from simulation paths")

ax.legend()

plt.tight_layout()

plt.show()

```

```text theme={null}

P(total passengers > 5,800) = 35.4%

Expected total passengers = 5,783

5th percentile = 5,720

95th percentile = 5,851

```

## 6. Using Simulation Paths for Decision-Making

The key advantage of simulation paths over prediction intervals is

answering **joint** probabilistic questions. Here are concrete examples.

### Example: Probability of exceeding a cumulative threshold

Suppose we have a capacity of 5,800 total passengers over the next 12

months. What is the probability of exceeding this capacity?

This question requires the **joint** distribution — it cannot be

answered from marginal intervals.

```python theme={null}

THRESHOLD = 5800

# Use NHITS_GMM simulations

sims_gmm = extract_sims(sim_df, "NHITS_GMM")

cumulative_passengers = sims_gmm.sum(axis=1) # Sum across H=12 months per path

prob_exceed = (cumulative_passengers > THRESHOLD).mean()

print(f"P(total passengers > {THRESHOLD:,}) = {prob_exceed:.1%}")

print(f"Expected total passengers = {cumulative_passengers.mean():,.0f}")

print(f"5th percentile = {np.quantile(cumulative_passengers, 0.05):,.0f}")

print(f"95th percentile = {np.quantile(cumulative_passengers, 0.95):,.0f}")

fig, ax = plt.subplots(figsize=(8, 3))

ax.hist(cumulative_passengers, bins=50, color="tab:red", alpha=0.7, edgecolor="white")

ax.axvline(THRESHOLD, color="black", linestyle="--", linewidth=2, label=f"Threshold = {THRESHOLD:,}")

ax.axvline(Y_test_df["y"].sum(), color="green", linestyle="-", linewidth=2, label=f"Actual = {Y_test_df['y'].sum():,.0f}")

ax.set_xlabel("Total passengers (12 months)")

ax.set_ylabel("Count")

ax.set_title("Distribution of cumulative passengers from simulation paths")

ax.legend()

plt.tight_layout()

plt.show()

```

```text theme={null}

P(total passengers > 5,800) = 35.4%

Expected total passengers = 5,783

5th percentile = 5,720

95th percentile = 5,851

```

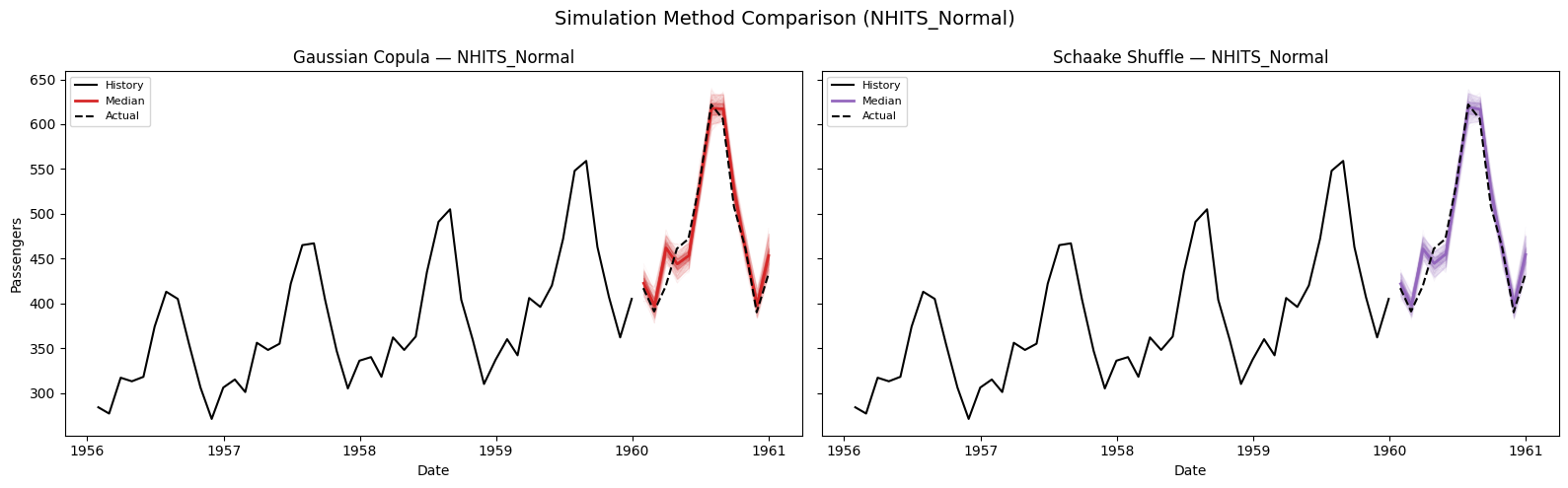

## 7. Comparing Simulation Methods: Gaussian Copula vs. Schaake Shuffle

Both methods use the same marginal quantile forecasts but differ in how

they introduce temporal correlation across horizon steps. Let’s compare

them on the **NHITS\_Normal** model.

```python theme={null}

# Generate paths with both methods

sim_copula = nf.simulate(n_paths=N_PATHS, seed=SEED, method="gaussian_copula")

sim_schaake = nf.simulate(n_paths=N_PATHS, seed=SEED, method="schaake_shuffle")

```

```python theme={null}

sims_copula = extract_sims(sim_copula, "NHITS_Normal")

sims_schaake = extract_sims(sim_schaake, "NHITS_Normal")

# Side-by-side path comparison

fig, axes = plt.subplots(1, 2, figsize=(16, 5), sharey=True)

hist = Y_train_df.sort_values("ds").tail(48)

last_date = hist["ds"].iloc[-1]

future_dates = pd.date_range(start=last_date, periods=H + 1, freq="MS")[1:]

for ax, sims, title, color in zip(

axes,

[sims_copula, sims_schaake],

["Gaussian Copula", "Schaake Shuffle"],

["tab:red", "tab:purple"],

):

ax.plot(hist["ds"], hist["y"], color="black", linewidth=1.5, label="History")

for i in range(min(100, sims.shape[0])):

ax.plot(future_dates, sims[i], color=color, alpha=0.05, linewidth=0.5)

for q_lo, q_hi, alpha in [(0.05, 0.95, 0.15), (0.25, 0.75, 0.30)]:

lo = np.quantile(sims, q_lo, axis=0)

hi = np.quantile(sims, q_hi, axis=0)

ax.fill_between(future_dates, lo, hi, color=color, alpha=alpha)

median = np.median(sims, axis=0)

ax.plot(future_dates, median, color=color, linewidth=2, label="Median")

ax.plot(Y_test_df["ds"], Y_test_df["y"], color="black", linestyle="--", label="Actual")

ax.set_title(f"{title} — NHITS_Normal")

ax.set_xlabel("Date")

ax.legend(loc="upper left", fontsize=8)

axes[0].set_ylabel("Passengers")

plt.suptitle("Simulation Method Comparison (NHITS_Normal)", fontsize=14)

plt.tight_layout()

plt.show()

```

## 7. Comparing Simulation Methods: Gaussian Copula vs. Schaake Shuffle

Both methods use the same marginal quantile forecasts but differ in how

they introduce temporal correlation across horizon steps. Let’s compare

them on the **NHITS\_Normal** model.

```python theme={null}

# Generate paths with both methods

sim_copula = nf.simulate(n_paths=N_PATHS, seed=SEED, method="gaussian_copula")

sim_schaake = nf.simulate(n_paths=N_PATHS, seed=SEED, method="schaake_shuffle")

```

```python theme={null}

sims_copula = extract_sims(sim_copula, "NHITS_Normal")

sims_schaake = extract_sims(sim_schaake, "NHITS_Normal")

# Side-by-side path comparison

fig, axes = plt.subplots(1, 2, figsize=(16, 5), sharey=True)

hist = Y_train_df.sort_values("ds").tail(48)

last_date = hist["ds"].iloc[-1]

future_dates = pd.date_range(start=last_date, periods=H + 1, freq="MS")[1:]

for ax, sims, title, color in zip(

axes,

[sims_copula, sims_schaake],

["Gaussian Copula", "Schaake Shuffle"],

["tab:red", "tab:purple"],

):

ax.plot(hist["ds"], hist["y"], color="black", linewidth=1.5, label="History")

for i in range(min(100, sims.shape[0])):

ax.plot(future_dates, sims[i], color=color, alpha=0.05, linewidth=0.5)

for q_lo, q_hi, alpha in [(0.05, 0.95, 0.15), (0.25, 0.75, 0.30)]:

lo = np.quantile(sims, q_lo, axis=0)

hi = np.quantile(sims, q_hi, axis=0)

ax.fill_between(future_dates, lo, hi, color=color, alpha=alpha)

median = np.median(sims, axis=0)

ax.plot(future_dates, median, color=color, linewidth=2, label="Median")

ax.plot(Y_test_df["ds"], Y_test_df["y"], color="black", linestyle="--", label="Actual")

ax.set_title(f"{title} — NHITS_Normal")

ax.set_xlabel("Date")

ax.legend(loc="upper left", fontsize=8)

axes[0].set_ylabel("Passengers")

plt.suptitle("Simulation Method Comparison (NHITS_Normal)", fontsize=14)

plt.tight_layout()

plt.show()

```

## 8. Evaluating Marginal vs. Joint Distributions

We can evaluate both the **marginal** distribution (from

`predict(quantiles=...)`) and the **joint** distribution (from

`simulate()`) using the same metrics. For each model we compare:

* **Point metrics**: MAE, MSE on the median forecast.

* **Probabilistic metric**: scaled CRPS on the quantile forecasts —

either from `predict` (marginal) or derived from simulation paths

(joint).

If the simulation paths are well-calibrated, their empirical quantiles

should score comparably to the model’s native marginal quantiles.

```python theme={null}

from utilsforecast.evaluation import evaluate

from utilsforecast.losses import mae, mse, scaled_crps

# ── Quantile grid for evaluation ──

eval_quantiles = np.round(np.arange(0.1, 1.0, 0.1), 2).tolist() # [0.1, 0.2, ..., 0.9]

# We'll evaluate NHITS_Normal only for clarity

MODEL = "NHITS_Normal"

# ── 1. Marginal quantiles from predict() ──

marginal_df = nf.predict(quantiles=eval_quantiles)

# Add actuals — align by position (predict uses freq="MS" dates, test data has month-end dates)

marginal_df = marginal_df.sort_values(["unique_id", "ds"]).reset_index(drop=True)

marginal_df["y"] = Y_test_df.sort_values(["unique_id", "ds"])["y"].values

# ── 2. Joint quantiles derived from simulation paths (gaussian_copula) ──

sims_gc = extract_sims(sim_copula, MODEL) # (n_paths, H)

joint_gc_df = marginal_df[["unique_id", "ds", "y"]].copy()

for q in eval_quantiles:

joint_gc_df[f"{MODEL}_ql{q}"] = np.quantile(sims_gc, q, axis=0)

joint_gc_df[MODEL] = np.median(sims_gc, axis=0)

# ── 3. Joint quantiles derived from simulation paths (schaake_shuffle) ──

sims_ss = extract_sims(sim_schaake, MODEL) # (n_paths, H)

joint_ss_df = marginal_df[["unique_id", "ds", "y"]].copy()

for q in eval_quantiles:

joint_ss_df[f"{MODEL}_ql{q}"] = np.quantile(sims_ss, q, axis=0)

joint_ss_df[MODEL] = np.median(sims_ss, axis=0)

```

```python theme={null}

# ── Evaluate point metrics (via evaluate) ──

point_marginal = evaluate(marginal_df, metrics=[mae, mse], models=[MODEL], agg_fn="mean")

point_gc = evaluate(joint_gc_df, metrics=[mae, mse], models=[MODEL], agg_fn="mean")

point_ss = evaluate(joint_ss_df, metrics=[mae, mse], models=[MODEL], agg_fn="mean")

# ── Evaluate scaled CRPS (called directly — evaluate expects level-style columns) ──

quantile_cols = {MODEL: [f"{MODEL}_ql{q}" for q in eval_quantiles]}

quantiles_arr = np.array(eval_quantiles)

crps_marginal = scaled_crps(marginal_df, models=quantile_cols, quantiles=quantiles_arr)

crps_gc = scaled_crps(joint_gc_df, models=quantile_cols, quantiles=quantiles_arr)

crps_ss = scaled_crps(joint_ss_df, models=quantile_cols, quantiles=quantiles_arr)

# ── Combine results ──

results = pd.DataFrame({

"Metric": ["MAE", "MSE", "Scaled CRPS"],

"Marginal (predict)": [

point_marginal[MODEL].values[0],

point_marginal[MODEL].values[1],

crps_marginal[MODEL].mean(),

],

"Joint — Gaussian Copula": [

point_gc[MODEL].values[0],

point_gc[MODEL].values[1],

crps_gc[MODEL].mean(),

],

"Joint — Schaake Shuffle": [

point_ss[MODEL].values[0],

point_ss[MODEL].values[1],

crps_ss[MODEL].mean(),

],

}).set_index("Metric")

print(f"Model: {MODEL}")

results

```

```text theme={null}

Model: NHITS_Normal

```

| | Marginal (predict) | Joint — Gaussian Copula | Joint — Schaake Shuffle |

| ----------- | ------------------ | ----------------------- | ----------------------- |

| Metric | | | |

| MAE | 12.669571 | 12.942172 | 12.516764 |

| MSE | 276.954919 | 288.357154 | 275.652889 |

| Scaled CRPS | 0.021440 | 0.022133 | 0.021545 |

**Interpreting the results:**

* **MAE / MSE** (point metrics): Both simulation methods use the

median of the sample paths as their point forecast. Since the

marginal quantiles and simulation-derived quantiles share the same

underlying model, the median forecasts are similar but not identical

— simulation introduces sampling variability.

* **Scaled CRPS** (probabilistic metric): Measures the quality of the

full quantile distribution. The marginal quantiles come directly

from the model’s predictive distribution, while the

simulation-derived quantiles are empirical (computed from `n_paths`

samples). With enough paths, the simulation CRPS should converge to

the marginal CRPS.

## 9. Summary

| Question | Use |

| ----------------------------------------------- | ------------------------------------------- |

| “What range is step $h$ likely in?” | `predict(level=...)` — prediction intervals |

| “What are realistic joint future trajectories?” | `simulate(n_paths=...)` — sample paths |

| “What is P(total > threshold)?” | `simulate()` then sum paths |

| “What is P(3 consecutive spikes)?” | `simulate()` then check path patterns |

| “What is the CVaR of my portfolio?” | `simulate()` then compute tail statistics |

### Simulation Methods

| Method | Use when… |

| --------------------------- | ---------------------------------------------------------------------------------------------------------------- |

| `gaussian_copula` (default) | You want smooth, parametric temporal correlation (AR(1) structure). Fast and robust. |

| `schaake_shuffle` | You want nonparametric dependence from historical data. Captures asymmetric / non-Gaussian correlation patterns. |

### Compatible Losses

| Loss type | How quantiles are obtained |

| ---------------------------------------- | ------------------------------------------------------------------------------- |

| `DistributionLoss`, `GMM`, `PMM`, `NBMM` | Arbitrary quantiles from parametric distribution |

| `MQLoss` / `HuberMQLoss` | Uses the model’s trained quantile grid |

| `IQLoss` / `HuberIQLoss` | Multiple forward passes, one per quantile |

| Point losses (`MAE`, `MSE`, etc.) | Conformal Prediction intervals (requires `prediction_intervals` during `fit()`) |

### References

* Baron, E. et al. (2025). [Efficiently generating correlated sample

paths from multi-step time series foundation

models](https://arxiv.org/abs/2510.02224). NeurIPS 2025 Workshop.

* Clark, M. et al. (2004). The Schaake shuffle: A method for

reconstructing space-time variability. *Journal of

Hydrometeorology*, 5(1).

## 8. Evaluating Marginal vs. Joint Distributions

We can evaluate both the **marginal** distribution (from

`predict(quantiles=...)`) and the **joint** distribution (from

`simulate()`) using the same metrics. For each model we compare:

* **Point metrics**: MAE, MSE on the median forecast.

* **Probabilistic metric**: scaled CRPS on the quantile forecasts —

either from `predict` (marginal) or derived from simulation paths

(joint).

If the simulation paths are well-calibrated, their empirical quantiles

should score comparably to the model’s native marginal quantiles.

```python theme={null}

from utilsforecast.evaluation import evaluate

from utilsforecast.losses import mae, mse, scaled_crps

# ── Quantile grid for evaluation ──

eval_quantiles = np.round(np.arange(0.1, 1.0, 0.1), 2).tolist() # [0.1, 0.2, ..., 0.9]

# We'll evaluate NHITS_Normal only for clarity

MODEL = "NHITS_Normal"

# ── 1. Marginal quantiles from predict() ──

marginal_df = nf.predict(quantiles=eval_quantiles)

# Add actuals — align by position (predict uses freq="MS" dates, test data has month-end dates)

marginal_df = marginal_df.sort_values(["unique_id", "ds"]).reset_index(drop=True)

marginal_df["y"] = Y_test_df.sort_values(["unique_id", "ds"])["y"].values

# ── 2. Joint quantiles derived from simulation paths (gaussian_copula) ──

sims_gc = extract_sims(sim_copula, MODEL) # (n_paths, H)

joint_gc_df = marginal_df[["unique_id", "ds", "y"]].copy()

for q in eval_quantiles:

joint_gc_df[f"{MODEL}_ql{q}"] = np.quantile(sims_gc, q, axis=0)

joint_gc_df[MODEL] = np.median(sims_gc, axis=0)

# ── 3. Joint quantiles derived from simulation paths (schaake_shuffle) ──

sims_ss = extract_sims(sim_schaake, MODEL) # (n_paths, H)

joint_ss_df = marginal_df[["unique_id", "ds", "y"]].copy()

for q in eval_quantiles:

joint_ss_df[f"{MODEL}_ql{q}"] = np.quantile(sims_ss, q, axis=0)

joint_ss_df[MODEL] = np.median(sims_ss, axis=0)

```

```python theme={null}

# ── Evaluate point metrics (via evaluate) ──

point_marginal = evaluate(marginal_df, metrics=[mae, mse], models=[MODEL], agg_fn="mean")

point_gc = evaluate(joint_gc_df, metrics=[mae, mse], models=[MODEL], agg_fn="mean")

point_ss = evaluate(joint_ss_df, metrics=[mae, mse], models=[MODEL], agg_fn="mean")

# ── Evaluate scaled CRPS (called directly — evaluate expects level-style columns) ──

quantile_cols = {MODEL: [f"{MODEL}_ql{q}" for q in eval_quantiles]}

quantiles_arr = np.array(eval_quantiles)

crps_marginal = scaled_crps(marginal_df, models=quantile_cols, quantiles=quantiles_arr)

crps_gc = scaled_crps(joint_gc_df, models=quantile_cols, quantiles=quantiles_arr)

crps_ss = scaled_crps(joint_ss_df, models=quantile_cols, quantiles=quantiles_arr)

# ── Combine results ──

results = pd.DataFrame({

"Metric": ["MAE", "MSE", "Scaled CRPS"],

"Marginal (predict)": [

point_marginal[MODEL].values[0],

point_marginal[MODEL].values[1],

crps_marginal[MODEL].mean(),

],

"Joint — Gaussian Copula": [

point_gc[MODEL].values[0],

point_gc[MODEL].values[1],

crps_gc[MODEL].mean(),

],

"Joint — Schaake Shuffle": [

point_ss[MODEL].values[0],

point_ss[MODEL].values[1],

crps_ss[MODEL].mean(),

],

}).set_index("Metric")

print(f"Model: {MODEL}")

results

```

```text theme={null}

Model: NHITS_Normal

```

| | Marginal (predict) | Joint — Gaussian Copula | Joint — Schaake Shuffle |

| ----------- | ------------------ | ----------------------- | ----------------------- |

| Metric | | | |

| MAE | 12.669571 | 12.942172 | 12.516764 |

| MSE | 276.954919 | 288.357154 | 275.652889 |

| Scaled CRPS | 0.021440 | 0.022133 | 0.021545 |

**Interpreting the results:**

* **MAE / MSE** (point metrics): Both simulation methods use the

median of the sample paths as their point forecast. Since the

marginal quantiles and simulation-derived quantiles share the same

underlying model, the median forecasts are similar but not identical

— simulation introduces sampling variability.

* **Scaled CRPS** (probabilistic metric): Measures the quality of the

full quantile distribution. The marginal quantiles come directly

from the model’s predictive distribution, while the

simulation-derived quantiles are empirical (computed from `n_paths`

samples). With enough paths, the simulation CRPS should converge to

the marginal CRPS.

## 9. Summary

| Question | Use |

| ----------------------------------------------- | ------------------------------------------- |

| “What range is step $h$ likely in?” | `predict(level=...)` — prediction intervals |

| “What are realistic joint future trajectories?” | `simulate(n_paths=...)` — sample paths |

| “What is P(total > threshold)?” | `simulate()` then sum paths |

| “What is P(3 consecutive spikes)?” | `simulate()` then check path patterns |

| “What is the CVaR of my portfolio?” | `simulate()` then compute tail statistics |

### Simulation Methods

| Method | Use when… |

| --------------------------- | ---------------------------------------------------------------------------------------------------------------- |

| `gaussian_copula` (default) | You want smooth, parametric temporal correlation (AR(1) structure). Fast and robust. |

| `schaake_shuffle` | You want nonparametric dependence from historical data. Captures asymmetric / non-Gaussian correlation patterns. |

### Compatible Losses

| Loss type | How quantiles are obtained |

| ---------------------------------------- | ------------------------------------------------------------------------------- |

| `DistributionLoss`, `GMM`, `PMM`, `NBMM` | Arbitrary quantiles from parametric distribution |

| `MQLoss` / `HuberMQLoss` | Uses the model’s trained quantile grid |

| `IQLoss` / `HuberIQLoss` | Multiple forward passes, one per quantile |

| Point losses (`MAE`, `MSE`, etc.) | Conformal Prediction intervals (requires `prediction_intervals` during `fit()`) |

### References

* Baron, E. et al. (2025). [Efficiently generating correlated sample

paths from multi-step time series foundation

models](https://arxiv.org/abs/2510.02224). NeurIPS 2025 Workshop.

* Clark, M. et al. (2004). The Schaake shuffle: A method for

reconstructing space-time variability. *Journal of

Hydrometeorology*, 5(1).