> ## Documentation Index

> Fetch the complete documentation index at: https://nixtlaverse.nixtla.io/llms.txt

> Use this file to discover all available pages before exploring further.

# Long-Horizon Forecasting with Transformer models

> Tutorial on how to train and forecast Transformer models.

Transformer models, originally proposed for applications in natural

language processing, have seen increasing adoption in the field of time

series forecasting. The transformative power of these models lies in

their novel architecture that relies heavily on the self-attention

mechanism, which helps the model to focus on different parts of the

input sequence to make predictions, while capturing long-range

dependencies within the data. In the context of time series forecasting,

Transformer models leverage this self-attention mechanism to identify

relevant information across different periods in the time series, making

them exceptionally effective in predicting future values for complex and

noisy sequences.

Long horizon forecasting consists of predicting a large number of

timestamps. It is a challenging task because of the *volatility* of the

predictions and the *computational complexity*. To solve this problem,

recent studies proposed a variety of Transformer-based models.

The Neuralforecast library includes implementations of the following

popular recent models: `Informer` (Zhou, H. et al. 2021), `Autoformer`

(Wu et al. 2021), `FEDformer` (Zhou, T. et al. 2022), and `PatchTST`

(Nie et al. 2023).

Our implementation of all these models are univariate, meaning that only

autoregressive values of each feature are used for forecasting. **We

observed that these unvivariate models are more accurate and faster than

their multivariate couterpart**.

In this notebook we will show how to: \* Load the

[ETTm2](https://github.com/zhouhaoyi/ETDataset) benchmark dataset, used

in the academic literature. \* Train models \* Forecast the test set

**The results achieved in this notebook outperform the original

self-reported results in the respective original paper, with a fraction

of the computational cost. Additionally, all models are trained with the

default recommended parameters, results can be further improved using

our `auto` models with automatic hyperparameter selection.**

You can run these experiments using GPU with Google Colab.

## 1. Installing libraries

```python theme={null}

%%capture

!pip install neuralforecast datasetsforecast utilsforecast

```

## 2. Load ETTm2 Data

The `LongHorizon` class will automatically download the complete ETTm2

dataset and process it.

It return three Dataframes: `Y_df` contains the values for the target

variables, `X_df` contains exogenous calendar features and `S_df`

contains static features for each time-series (none for ETTm2). For this

example we will only use `Y_df`.

If you want to use your own data just replace `Y_df`. Be sure to use a

long format and have a similar structure to our data set.

```python theme={null}

import pandas as pd

from datasetsforecast.long_horizon import LongHorizon

```

```python theme={null}

# Change this to your own data to try the model

Y_df, _, _ = LongHorizon.load(directory='./', group='ETTm2')

Y_df['ds'] = pd.to_datetime(Y_df['ds'])

n_time = len(Y_df.ds.unique())

val_size = int(.2 * n_time)

test_size = int(.2 * n_time)

Y_df.groupby('unique_id').head(2)

```

| | unique\_id | ds | y |

| ------ | ---------- | ------------------- | --------- |

| 0 | HUFL | 2016-07-01 00:00:00 | -0.041413 |

| 1 | HUFL | 2016-07-01 00:15:00 | -0.185467 |

| 57600 | HULL | 2016-07-01 00:00:00 | 0.040104 |

| 57601 | HULL | 2016-07-01 00:15:00 | -0.214450 |

| 115200 | LUFL | 2016-07-01 00:00:00 | 0.695804 |

| 115201 | LUFL | 2016-07-01 00:15:00 | 0.434685 |

| 172800 | LULL | 2016-07-01 00:00:00 | 0.434430 |

| 172801 | LULL | 2016-07-01 00:15:00 | 0.428168 |

| 230400 | MUFL | 2016-07-01 00:00:00 | -0.599211 |

| 230401 | MUFL | 2016-07-01 00:15:00 | -0.658068 |

| 288000 | MULL | 2016-07-01 00:00:00 | -0.393536 |

| 288001 | MULL | 2016-07-01 00:15:00 | -0.659338 |

| 345600 | OT | 2016-07-01 00:00:00 | 1.018032 |

| 345601 | OT | 2016-07-01 00:15:00 | 0.980124 |

## 3. Train models

We will train models using the `cross_validation` method, which allows

users to automatically simulate multiple historic forecasts (in the test

set).

The `cross_validation` method will use the validation set for

hyperparameter selection and early stopping, and will then produce the

forecasts for the test set.

First, instantiate each model in the `models` list, specifying the

`horizon`, `input_size`, and training iterations.

(NOTE: The `FEDformer` model was excluded due to extremely long training

times.)

```python theme={null}

%%capture

from neuralforecast.core import NeuralForecast

from neuralforecast.models import Informer, Autoformer, FEDformer, PatchTST

```

```text theme={null}

INFO:torch.distributed.nn.jit.instantiator:Created a temporary directory at /tmp/tmpopb2vyyt

INFO:torch.distributed.nn.jit.instantiator:Writing /tmp/tmpopb2vyyt/_remote_module_non_scriptable.py

```

```python theme={null}

%%capture

horizon = 96 # 24hrs = 4 * 15 min.

models = [Informer(h=horizon, # Forecasting horizon

input_size=horizon, # Input size

max_steps=1000, # Number of training iterations

val_check_steps=100, # Compute validation loss every 100 steps

early_stop_patience_steps=3), # Stop training if validation loss does not improve

Autoformer(h=horizon,

input_size=horizon,

max_steps=1000,

val_check_steps=100,

early_stop_patience_steps=3),

PatchTST(h=horizon,

input_size=horizon,

max_steps=1000,

val_check_steps=100,

early_stop_patience_steps=3),

]

```

```text theme={null}

INFO:lightning_fabric.utilities.seed:Global seed set to 1

INFO:lightning_fabric.utilities.seed:Global seed set to 1

INFO:lightning_fabric.utilities.seed:Global seed set to 1

```

> **Tip**

>

> Check our `auto` models for automatic hyperparameter optimization.

Instantiate a `NeuralForecast` object with the following required

parameters:

* `models`: a list of models.

* `freq`: a string indicating the frequency of the data. (See [panda’s

available

frequencies](https://pandas.pydata.org/pandas-docs/stable/user_guide/timeseries.html#offset-aliases).)

Second, use the `cross_validation` method, specifying the dataset

(`Y_df`), validation size and test size.

```python theme={null}

%%capture

nf = NeuralForecast(

models=models,

freq='15min')

Y_hat_df = nf.cross_validation(df=Y_df,

val_size=val_size,

test_size=test_size,

n_windows=None)

```

The `cross_validation` method will return the forecasts for each model

on the test set.

```python theme={null}

Y_hat_df.head()

```

| | unique\_id | ds | cutoff | Informer | Autoformer | PatchTST | y |

| - | ---------- | ------------------- | ------------------- | --------- | ---------- | --------- | --------- |

| 0 | HUFL | 2017-10-24 00:00:00 | 2017-10-23 23:45:00 | -1.055062 | -0.861487 | -0.860189 | -0.977673 |

| 1 | HUFL | 2017-10-24 00:15:00 | 2017-10-23 23:45:00 | -1.021247 | -0.873399 | -0.865730 | -0.865620 |

| 2 | HUFL | 2017-10-24 00:30:00 | 2017-10-23 23:45:00 | -1.057297 | -0.900345 | -0.944296 | -0.961624 |

| 3 | HUFL | 2017-10-24 00:45:00 | 2017-10-23 23:45:00 | -0.886652 | -0.867466 | -0.974849 | -1.049700 |

| 4 | HUFL | 2017-10-24 01:00:00 | 2017-10-23 23:45:00 | -1.000431 | -0.887454 | -1.008530 | -0.953600 |

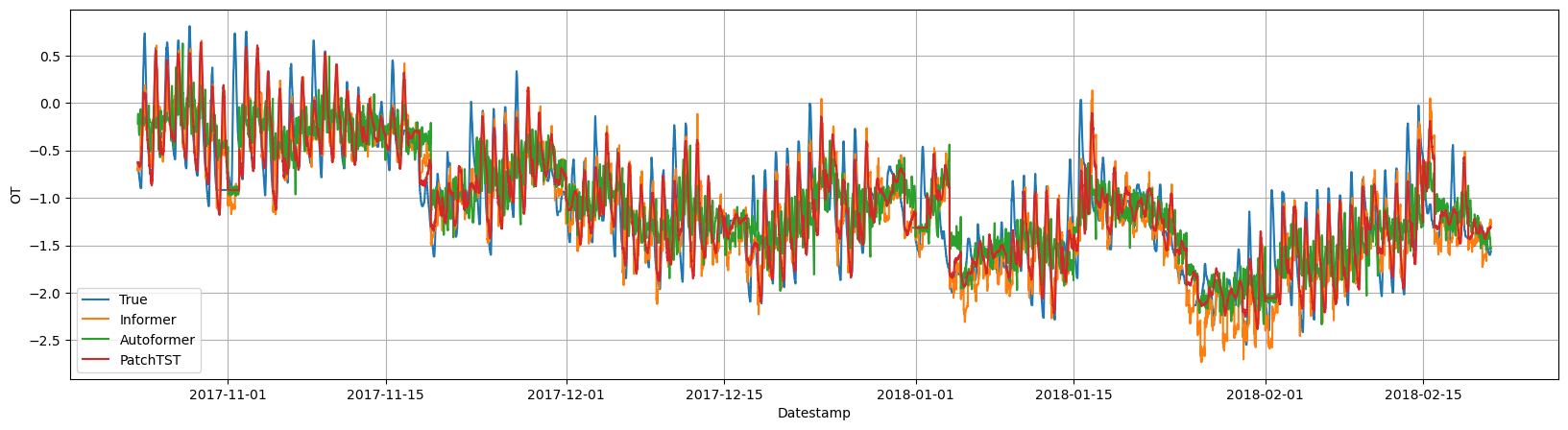

## 4. Evaluate Results

Next, we plot the forecasts on the test set for the `OT` variable for

all models.

```python theme={null}

import matplotlib.pyplot as plt

```

```python theme={null}

Y_plot = Y_hat_df[Y_hat_df['unique_id']=='OT'] # OT dataset

cutoffs = Y_hat_df['cutoff'].unique()[::horizon]

Y_plot = Y_plot[Y_hat_df['cutoff'].isin(cutoffs)]

plt.figure(figsize=(20,5))

plt.plot(Y_plot['ds'], Y_plot['y'], label='True')

plt.plot(Y_plot['ds'], Y_plot['Informer'], label='Informer')

plt.plot(Y_plot['ds'], Y_plot['Autoformer'], label='Autoformer')

plt.plot(Y_plot['ds'], Y_plot['PatchTST'], label='PatchTST')

plt.xlabel('Datestamp')

plt.ylabel('OT')

plt.grid()

plt.legend()

```

## 1. Installing libraries

```python theme={null}

%%capture

!pip install neuralforecast datasetsforecast utilsforecast

```

## 2. Load ETTm2 Data

The `LongHorizon` class will automatically download the complete ETTm2

dataset and process it.

It return three Dataframes: `Y_df` contains the values for the target

variables, `X_df` contains exogenous calendar features and `S_df`

contains static features for each time-series (none for ETTm2). For this

example we will only use `Y_df`.

If you want to use your own data just replace `Y_df`. Be sure to use a

long format and have a similar structure to our data set.

```python theme={null}

import pandas as pd

from datasetsforecast.long_horizon import LongHorizon

```

```python theme={null}

# Change this to your own data to try the model

Y_df, _, _ = LongHorizon.load(directory='./', group='ETTm2')

Y_df['ds'] = pd.to_datetime(Y_df['ds'])

n_time = len(Y_df.ds.unique())

val_size = int(.2 * n_time)

test_size = int(.2 * n_time)

Y_df.groupby('unique_id').head(2)

```

| | unique\_id | ds | y |

| ------ | ---------- | ------------------- | --------- |

| 0 | HUFL | 2016-07-01 00:00:00 | -0.041413 |

| 1 | HUFL | 2016-07-01 00:15:00 | -0.185467 |

| 57600 | HULL | 2016-07-01 00:00:00 | 0.040104 |

| 57601 | HULL | 2016-07-01 00:15:00 | -0.214450 |

| 115200 | LUFL | 2016-07-01 00:00:00 | 0.695804 |

| 115201 | LUFL | 2016-07-01 00:15:00 | 0.434685 |

| 172800 | LULL | 2016-07-01 00:00:00 | 0.434430 |

| 172801 | LULL | 2016-07-01 00:15:00 | 0.428168 |

| 230400 | MUFL | 2016-07-01 00:00:00 | -0.599211 |

| 230401 | MUFL | 2016-07-01 00:15:00 | -0.658068 |

| 288000 | MULL | 2016-07-01 00:00:00 | -0.393536 |

| 288001 | MULL | 2016-07-01 00:15:00 | -0.659338 |

| 345600 | OT | 2016-07-01 00:00:00 | 1.018032 |

| 345601 | OT | 2016-07-01 00:15:00 | 0.980124 |

## 3. Train models

We will train models using the `cross_validation` method, which allows

users to automatically simulate multiple historic forecasts (in the test

set).

The `cross_validation` method will use the validation set for

hyperparameter selection and early stopping, and will then produce the

forecasts for the test set.

First, instantiate each model in the `models` list, specifying the

`horizon`, `input_size`, and training iterations.

(NOTE: The `FEDformer` model was excluded due to extremely long training

times.)

```python theme={null}

%%capture

from neuralforecast.core import NeuralForecast

from neuralforecast.models import Informer, Autoformer, FEDformer, PatchTST

```

```text theme={null}

INFO:torch.distributed.nn.jit.instantiator:Created a temporary directory at /tmp/tmpopb2vyyt

INFO:torch.distributed.nn.jit.instantiator:Writing /tmp/tmpopb2vyyt/_remote_module_non_scriptable.py

```

```python theme={null}

%%capture

horizon = 96 # 24hrs = 4 * 15 min.

models = [Informer(h=horizon, # Forecasting horizon

input_size=horizon, # Input size

max_steps=1000, # Number of training iterations

val_check_steps=100, # Compute validation loss every 100 steps

early_stop_patience_steps=3), # Stop training if validation loss does not improve

Autoformer(h=horizon,

input_size=horizon,

max_steps=1000,

val_check_steps=100,

early_stop_patience_steps=3),

PatchTST(h=horizon,

input_size=horizon,

max_steps=1000,

val_check_steps=100,

early_stop_patience_steps=3),

]

```

```text theme={null}

INFO:lightning_fabric.utilities.seed:Global seed set to 1

INFO:lightning_fabric.utilities.seed:Global seed set to 1

INFO:lightning_fabric.utilities.seed:Global seed set to 1

```

> **Tip**

>

> Check our `auto` models for automatic hyperparameter optimization.

Instantiate a `NeuralForecast` object with the following required

parameters:

* `models`: a list of models.

* `freq`: a string indicating the frequency of the data. (See [panda’s

available

frequencies](https://pandas.pydata.org/pandas-docs/stable/user_guide/timeseries.html#offset-aliases).)

Second, use the `cross_validation` method, specifying the dataset

(`Y_df`), validation size and test size.

```python theme={null}

%%capture

nf = NeuralForecast(

models=models,

freq='15min')

Y_hat_df = nf.cross_validation(df=Y_df,

val_size=val_size,

test_size=test_size,

n_windows=None)

```

The `cross_validation` method will return the forecasts for each model

on the test set.

```python theme={null}

Y_hat_df.head()

```

| | unique\_id | ds | cutoff | Informer | Autoformer | PatchTST | y |

| - | ---------- | ------------------- | ------------------- | --------- | ---------- | --------- | --------- |

| 0 | HUFL | 2017-10-24 00:00:00 | 2017-10-23 23:45:00 | -1.055062 | -0.861487 | -0.860189 | -0.977673 |

| 1 | HUFL | 2017-10-24 00:15:00 | 2017-10-23 23:45:00 | -1.021247 | -0.873399 | -0.865730 | -0.865620 |

| 2 | HUFL | 2017-10-24 00:30:00 | 2017-10-23 23:45:00 | -1.057297 | -0.900345 | -0.944296 | -0.961624 |

| 3 | HUFL | 2017-10-24 00:45:00 | 2017-10-23 23:45:00 | -0.886652 | -0.867466 | -0.974849 | -1.049700 |

| 4 | HUFL | 2017-10-24 01:00:00 | 2017-10-23 23:45:00 | -1.000431 | -0.887454 | -1.008530 | -0.953600 |

## 4. Evaluate Results

Next, we plot the forecasts on the test set for the `OT` variable for

all models.

```python theme={null}

import matplotlib.pyplot as plt

```

```python theme={null}

Y_plot = Y_hat_df[Y_hat_df['unique_id']=='OT'] # OT dataset

cutoffs = Y_hat_df['cutoff'].unique()[::horizon]

Y_plot = Y_plot[Y_hat_df['cutoff'].isin(cutoffs)]

plt.figure(figsize=(20,5))

plt.plot(Y_plot['ds'], Y_plot['y'], label='True')

plt.plot(Y_plot['ds'], Y_plot['Informer'], label='Informer')

plt.plot(Y_plot['ds'], Y_plot['Autoformer'], label='Autoformer')

plt.plot(Y_plot['ds'], Y_plot['PatchTST'], label='PatchTST')

plt.xlabel('Datestamp')

plt.ylabel('OT')

plt.grid()

plt.legend()

```

Finally, we compute the test errors using the Mean Absolute Error (MAE):

$\qquad MAE = \frac{1}{Windows * Horizon} \sum_{\tau} |y_{\tau} - \hat{y}_{\tau}| \qquad$

```python theme={null}

from utilsforecast.evaluation import evaluate

from utilsforecast.losses import mae

```

```python theme={null}

eval_df = evaluate(

df=Y_hat_df.drop(columns=["cutoff"]),

metrics=[mae],

agg_fn="mean"

)

print('Informer: ', eval_df.iloc[0]["Informer"])

print('Autoformer: ', eval_df.iloc[0]["Autoformer"])

print('PatchTST: ', eval_df.iloc[0]["PatchTST"])

```

```text theme={null}

Informer: 0.339

Autoformer: 0.316

PatchTST: 0.251

```

For reference, we can check the performance when compared to

self-reported performance in their respective papers.

| Horizon | PatchTST | AutoFormer | Informer | ARIMA |

| ------- | --------- | ---------- | -------- | ----- |

| 96 | **0.256** | 0.339 | 0.453 | 0.301 |

| 192 | 0.296 | 0.340 | 0.563 | 0.345 |

| 336 | 0.329 | 0.372 | 0.887 | 0.386 |

| 720 | 0.385 | 0.419 | 1.388 | 0.445 |

## Next steps

We proposed an alternative model for long-horizon forecasting, the

`NHITS`, based on feed-forward networks in (Challu et al. 2023). It

achieves on par performance with `PatchTST`, with a fraction of the

computational cost. The `NHITS` tutorial is available

[here](https://nixtlaverse.nixtla.io/neuralforecast/docs/tutorials/longhorizon_with_nhits.html).

## References

[Zhou, H., Zhang, S., Peng, J., Zhang, S., Li, J., Xiong, H., & Zhang,

W. (2021, May). Informer: Beyond efficient transformer for long sequence

time-series forecasting. In Proceedings of the AAAI conference on

artificial intelligence (Vol. 35, No. 12,

pp. 11106-11115)](https://ojs.aaai.org/index.php/AAAI/article/view/17325)

[Wu, H., Xu, J., Wang, J., & Long, M. (2021). Autoformer: Decomposition

transformers with auto-correlation for long-term series forecasting.

Advances in Neural Information Processing Systems, 34,

22419-22430.](https://proceedings.neurips.cc/paper/2021/hash/bcc0d400288793e8bdcd7c19a8ac0c2b-Abstract.html)

[Zhou, T., Ma, Z., Wen, Q., Wang, X., Sun, L., & Jin, R. (2022, June).

Fedformer: Frequency enhanced decomposed transformer for long-term

series forecasting. In International Conference on Machine Learning

(pp. 27268-27286).

PMLR.](https://proceedings.mlr.press/v162/zhou22g.html)

[Nie, Y., Nguyen, N. H., Sinthong, P., & Kalagnanam, J. (2022). A Time

Series is Worth 64 Words: Long-term Forecasting with

Transformers.](https://arxiv.org/pdf/2211.14730.pdf)

[Cristian Challu, Kin G. Olivares, Boris N. Oreshkin, Federico Garza,

Max Mergenthaler-Canseco, Artur Dubrawski (2021). NHITS: Neural

Hierarchical Interpolation for Time Series Forecasting. Accepted at AAAI

2023.](https://arxiv.org/abs/2201.12886)

Finally, we compute the test errors using the Mean Absolute Error (MAE):

$\qquad MAE = \frac{1}{Windows * Horizon} \sum_{\tau} |y_{\tau} - \hat{y}_{\tau}| \qquad$

```python theme={null}

from utilsforecast.evaluation import evaluate

from utilsforecast.losses import mae

```

```python theme={null}

eval_df = evaluate(

df=Y_hat_df.drop(columns=["cutoff"]),

metrics=[mae],

agg_fn="mean"

)

print('Informer: ', eval_df.iloc[0]["Informer"])

print('Autoformer: ', eval_df.iloc[0]["Autoformer"])

print('PatchTST: ', eval_df.iloc[0]["PatchTST"])

```

```text theme={null}

Informer: 0.339

Autoformer: 0.316

PatchTST: 0.251

```

For reference, we can check the performance when compared to

self-reported performance in their respective papers.

| Horizon | PatchTST | AutoFormer | Informer | ARIMA |

| ------- | --------- | ---------- | -------- | ----- |

| 96 | **0.256** | 0.339 | 0.453 | 0.301 |

| 192 | 0.296 | 0.340 | 0.563 | 0.345 |

| 336 | 0.329 | 0.372 | 0.887 | 0.386 |

| 720 | 0.385 | 0.419 | 1.388 | 0.445 |

## Next steps

We proposed an alternative model for long-horizon forecasting, the

`NHITS`, based on feed-forward networks in (Challu et al. 2023). It

achieves on par performance with `PatchTST`, with a fraction of the

computational cost. The `NHITS` tutorial is available

[here](https://nixtlaverse.nixtla.io/neuralforecast/docs/tutorials/longhorizon_with_nhits.html).

## References

[Zhou, H., Zhang, S., Peng, J., Zhang, S., Li, J., Xiong, H., & Zhang,

W. (2021, May). Informer: Beyond efficient transformer for long sequence

time-series forecasting. In Proceedings of the AAAI conference on

artificial intelligence (Vol. 35, No. 12,

pp. 11106-11115)](https://ojs.aaai.org/index.php/AAAI/article/view/17325)

[Wu, H., Xu, J., Wang, J., & Long, M. (2021). Autoformer: Decomposition

transformers with auto-correlation for long-term series forecasting.

Advances in Neural Information Processing Systems, 34,

22419-22430.](https://proceedings.neurips.cc/paper/2021/hash/bcc0d400288793e8bdcd7c19a8ac0c2b-Abstract.html)

[Zhou, T., Ma, Z., Wen, Q., Wang, X., Sun, L., & Jin, R. (2022, June).

Fedformer: Frequency enhanced decomposed transformer for long-term

series forecasting. In International Conference on Machine Learning

(pp. 27268-27286).

PMLR.](https://proceedings.mlr.press/v162/zhou22g.html)

[Nie, Y., Nguyen, N. H., Sinthong, P., & Kalagnanam, J. (2022). A Time

Series is Worth 64 Words: Long-term Forecasting with

Transformers.](https://arxiv.org/pdf/2211.14730.pdf)

[Cristian Challu, Kin G. Olivares, Boris N. Oreshkin, Federico Garza,

Max Mergenthaler-Canseco, Artur Dubrawski (2021). NHITS: Neural

Hierarchical Interpolation for Time Series Forecasting. Accepted at AAAI

2023.](https://arxiv.org/abs/2201.12886)